|

시장보고서

상품코드

1885811

그린 수소 생산용 화학제품 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Green Hydrogen Production Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

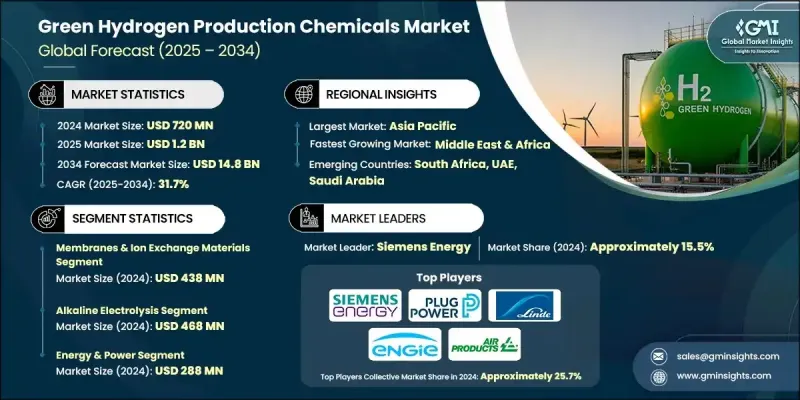

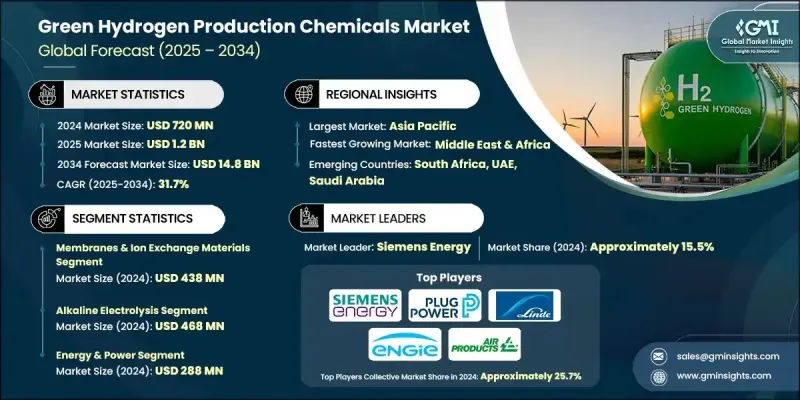

그린 수소 생산용 화학제품 시장은 2024년 7억 2,000만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 31.7%로 성장할 전망이며, 148억 달러에 이를 것으로 예측됩니다.

정부에 의한 탈탄소화 의무 강화 및 그린 수소 생산용 화학제품을 직접 지원하는 보조금 제도의 도입으로 업계의 기세는 계속 가속화되고 있습니다. 이러한 조치는 프로젝트 자금 조달을 개선하고 투자자의 확신을 높이며 산업이 저탄소 화학 공정으로의 전환을 촉진하는 동기입니다. 풍력 및 태양광 발전 비용의 급격한 저하도 시장 전망을 강화하여 주요 비용 요인인 신재생 전력의 보다 저렴한 가격으로의 이용을 가능하게 하고 있습니다. 신재생 에너지 가격 하락이 계속되는 가운데 대규모 그린 수소 및 파생 화학제품의 생산은 점점 더 실현가능해지고 시장의 상업적 매력을 확대하고 있습니다. 한편, 전해조 기술의 자본 비용 절감 및 효율 향상에 의해 생산 비용 전체가 저하하고 있습니다. 이 변화에 따라 제조업체는 규모 확대, 신규 및 첨단 프로세스 화학제품의 개발, 고성능 촉매 및 막의 채용을 추진해, 공급망 전체에서의 가치 창조를 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 시 가치 | 7억 2,000만 달러 |

| 예측 금액 | 148억 달러 |

| CAGR | 31.7% |

멤브레인 및 이온 교환 재료 부문은 2024년에 4억 3,800만 달러로 평가되었으며, 2025-2034년 연평균 복합 성장률(CAGR) 41.2%로 성장할 것으로 예측됩니다. 생산자가 운영 성능 향상을 목표로 하는 동안 이러한 재료는 전해 장치 시스템에 널리 통합되고 있습니다. 보다 고품질의 촉매 및 순도가 높은 전해질이 도입되어 변환 효율의 극대화와 에너지 손실의 저감을 도모하고 있습니다. 한편, 내구성이 뛰어난 막은 PEM(양성자 교환막) 및 AEM(알칼리 전해막) 유닛의 신뢰성을 지원하기 위해 필수적이 되고 있습니다. 이러한 재료가 지속적인 가동과 안정적인 시스템 성능을 실현하는 역할은 이 부문에서 장기적인 수요를 이끌고 있습니다.

알칼리 전해 부문은 2024년에 4억 6,800만 달러에 이르렀고, 2025-2034년 연평균 복합 성장률(CAGR) 28.4%로 성장할 것으로 예측됩니다. 알칼리 전해 및 PEM 전해 기술이 상업적 환경에서 보급됨에 따라 수요가 증가하고 있습니다. 알칼리 시스템은 안정적인 출력을 유지하기 위해 견고한 촉매 및 안정적인 전해질을 필요로 하는 반면, PEM 기술은 고효율 막, 이온 교환 재료 및 고급 촉매에 의존합니다. 산업 거점과 수소 구동 시설의 도입 확대에 따라 성능과 장수명을 지원하는 신뢰성이 높은 고품질의 화학 원료에 대한 수요가 높아지고 있습니다.

북미의 그린 수소 생산용 화학제품 시장은 2024년 5,040만 달러로 평가되었습니다. 신재생 에너지 도입 확대 및 연방정부의 인센티브 프로그램이 지역 전체의 수소 제조 활동과 화학제품 소비를 촉진하고 있습니다. 전해조 개발, 청정 에너지 인프라, 수소 수송 네트워크에 대한 투자 증가로 신규 프로젝트에서 촉매, 막, 정제 화학제품, 수처리제의 사용이 더욱 확대되고 있습니다. 이 분야에서 활동하는 주요 기업으로는 ENGIE, Siemens Energy AG, Linde plc, Plug Power Inc., Air Products and Chemicals, Inc. 등이 참가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위 및 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별 및 국가별

- 기본 추정치 및 계산

- 기준 연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건 및 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(주 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 화학 유형별(2021-2034년)

- 주요 동향

- 촉매

- 전해 촉매(PEM, 알칼리, 고체 산화물)

- 광촉매

- 전해질

- 산성 전해질

- 알칼리 전해질

- 막 및 이온 교환 재료

- 양성자 교환막

- 음이온 교환막

- 수처리 약품

- 탈이온제

- 스케일 방지제

- 부식 방지제

- 가스 정화용 약제

- 탈산소제

- 흡습제

제6장 시장 추계 및 예측 : 제조 기술별(2021-2034년)

- 주요 동향

- 알칼리 전해

- 양성자 교환막(PEM) 전해

- 고체 산화물 전해

- 광전기화학적 수소 제조

- 열화학 공정

제7장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 에너지 및 전력

- 교통기관

- 공업 프로세스

- 화학제조

- 일렉트로닉스

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Air Liquide SA

- Air Products and Chemicals, Inc.

- Linde plc

- Siemens Energy AG

- ENGIE

- Plug Power Inc.

- Bloom Energy Corporation

- Nel Hydrogen

- Cummins Inc.

- McPhy Energy SA

- thyssenkrupp AG

- Ballard Power Systems Inc.

- Reliance Industries Ltd.

- Adani Green Energy Ltd.

- Sinopec

The Green Hydrogen Production Chemicals Market was valued at USD 720 million in 2024 and is estimated to grow at a CAGR of 31.7% to reach USD 14.8 billion by 2034.

Industry momentum continues to accelerate as governments intensify decarbonization mandates and roll out subsidy frameworks that directly support chemical inputs used in green hydrogen production. These measures have improved project financing, increased investor assurance, and motivated industries to transition toward low-carbon chemical processes. Rapid declines in the cost of wind and solar power have also strengthened the market outlook, enabling producers to operate electrolysers with more affordable renewable electricity, which remains the primary cost driver. As renewable pricing continues to fall, large-scale green hydrogen and derivative chemical production has become increasingly viable, expanding the market's commercial attractiveness. Meanwhile, lower capital costs and improved efficiencies in electrolyser technology have reduced overall production expenses. This shift is pushing manufacturers to scale up, develop new and advanced process chemicals, and adopt high-performance catalysts and membranes, strengthening value creation across the supply chain.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $720 Million |

| Forecast Value | $14.8 Billion |

| CAGR | 31.7% |

The membranes and ion-exchange materials segment was valued at USD 438 million in 2024 and is forecast to grow at a CAGR of 41.2% from 2025 to 2034. These materials are being integrated more widely into electrolyser systems as producers aim to enhance operational performance. Higher-grade catalysts and purer electrolytes are being deployed to maximize conversion efficiency and reduce energy losses, while durable membranes are becoming essential to support the reliability of PEM and AEM units. Their role in enabling continuous operation and stable system performance is driving long-term demand in this segment.

The alkaline electrolysis segment reached USD 468 million in 2024 and is expected to grow at a CAGR of 28.4% from 2025 to 2034. Demand is rising as alkaline and PEM electrolysis technologies gain traction in commercial settings. Alkaline systems require robust catalysts and stable electrolytes to maintain steady output, while PEM technologies depend on high-efficiency membranes, ion-exchange materials, and advanced catalysts. Their growing deployment across industrial hubs and hydrogen-driven facilities is increasing the need for reliable, high-quality chemical inputs that support performance and long operating lifespans.

North America Green Hydrogen Production Chemicals Market was valued at USD 50.4 million in 2024. Expanding renewable energy adoption and federal incentive programs are boosting hydrogen manufacturing activities and chemical consumption across the region. Rising investments in electrolyser development, clean-energy infrastructures, and hydrogen transport networks are further increasing the use of catalysts, membranes, purification chemicals, and water-treatment agents across new projects. Key companies active in this space include ENGIE, Siemens Energy AG, Linde plc, Plug Power Inc., Air Products and Chemicals, Inc., and other participants.

Leading companies in the Global Green Hydrogen Production Chemicals Market are strengthening their competitive position through several focused strategies. Many are investing heavily in R&D to design higher-efficiency catalysts, membranes, and electrolytes that enhance electrolyser performance and reduce overall production costs. Strategic partnerships with renewable energy developers, electrolyser manufacturers, and industrial end users are increasingly common, ensuring long-term supply agreements and integrated project development. Companies are also expanding manufacturing capacity to meet rising demand and are localizing production to reduce logistics costs and qualify for regional incentives. Sustainability commitments and portfolio diversification into advanced materials, specialized chemical inputs, and next-generation hydrogen technologies are further reinforcing their market foothold.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Chemical Type

- 2.2.3 Production Technology

- 2.2.4 End Use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Chemical Type, 2021- 2034 (USD Million, Kilo Tons)

- 5.1 Key trends

- 5.2 Catalysts

- 5.2.1 Electrolysis catalysts (PEM, alkaline, solid oxide)

- 5.2.2 Photocatalysts

- 5.3 Electrolytes

- 5.3.1 Acidic electrolytes

- 5.3.2 Alkaline electrolytes

- 5.4 Membranes & ion exchange materials

- 5.4.1 Proton exchange membranes

- 5.4.2 Anion exchange membranes

- 5.5 Water treatment chemicals

- 5.5.1 Deionization agents

- 5.5.2 Anti-scaling agents

- 5.5.3 Corrosion inhibitors

- 5.6 Gas purification chemicals

- 5.6.1 Oxygen removal agents

- 5.6.2 Moisture absorbers

Chapter 6 Market Estimates and Forecast, By Production Technology, 2021 - 2034 (USD Million, Kilo Tons)

- 6.1 Key trends

- 6.2 Alkaline electrolysis

- 6.3 Proton exchange membrane (PEM) electrolysis

- 6.4 Solid oxide electrolysis

- 6.5 Photoelectrochemical water splitting

- 6.6 Thermochemical processes

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Million, Kilo Tons)

- 7.1 Key trends

- 7.2 Energy & power

- 7.3 Transportation

- 7.4 Industrial processing

- 7.5 Chemical manufacturing

- 7.6 Electronics

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Air Liquide S.A.

- 9.2 Air Products and Chemicals, Inc.

- 9.3 Linde plc

- 9.4 Siemens Energy AG

- 9.5 ENGIE

- 9.6 Plug Power Inc.

- 9.7 Bloom Energy Corporation

- 9.8 Nel Hydrogen

- 9.9 Cummins Inc.

- 9.10 McPhy Energy S.A.

- 9.11 thyssenkrupp AG

- 9.12 Ballard Power Systems Inc.

- 9.13 Reliance Industries Ltd.

- 9.14 Adani Green Energy Ltd.

- 9.15 Sinopec