|

시장보고서

상품코드

1885812

탄소 포집 활용 화학제품(CCU) 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)Carbon Capture Utilization Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

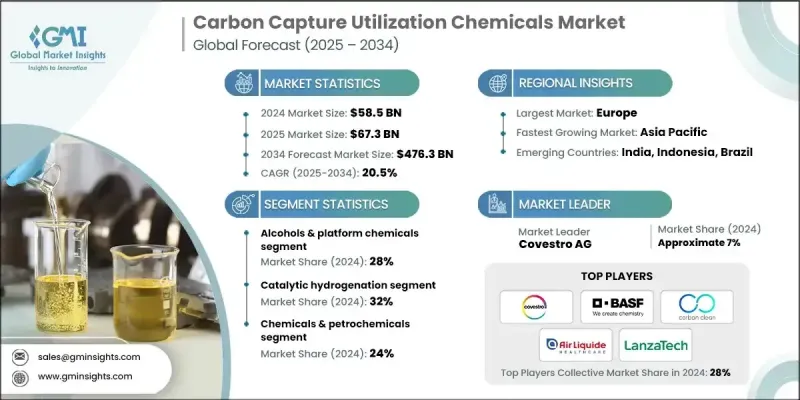

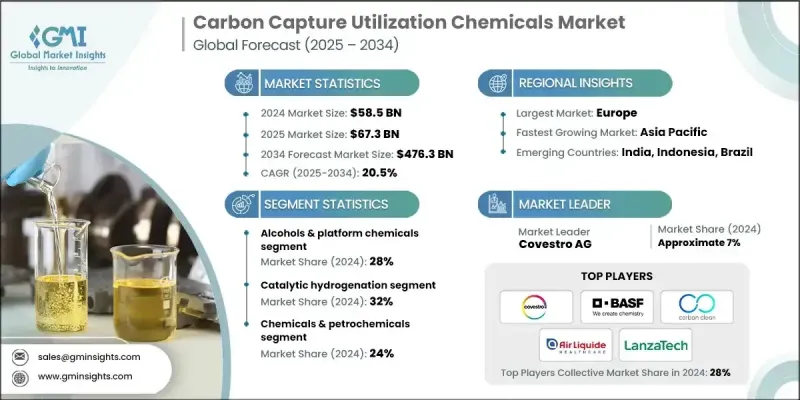

세계의 탄소 포집 활용 화학제품 시장은 2024년에 585억 달러로 평가되었고 2034년까지 연평균 복합 성장률(CAGR) 20.5%로 성장하고, 4,763억 달러에 이를 것으로 예측되고 있습니다.

세계 기업들이 장기적인 넷 제로 전략의 일환으로 저탄소 및 카본 음성 소재를 우선적으로 채택하고 있어 이에 의해 회수된 이산화탄소로부터 제조되는 솔루션에 대한 수요가 높아지고 있습니다. 제조업체는 저배출 소재의 조달 목표를 확대하고 있으며 여러 산업이 공급망 배출량을 줄이기 위해 CO2 기반 제품을 채택하고 있습니다. 촉매 기술, 전해 기술, 시스템 통합의 급속한 진보로 비용 절감과 성능 향상을 실현하고 있습니다. 이것은 CO2 변환에서 더 높은 효율과 안정성을 제공하는 신흥 촉매 기술에 의해 지원됩니다. 고성능 전해 시스템은 전류 밀도 향상을 달성하고 컴팩트한 시스템 설계를 통해 설비 투자를 삭감하고 있습니다. 시장은 또한 소규모 실증에서 본격적인 상업운전으로 이행하고 있으며, 재생가능수소, 고농도 CO2원, 바이오에너지시스템을 조합한 통합생산모델이 강력한 도입경로를 창출하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 585억 달러 |

| 예측 금액 | 4,763억 달러 |

| CAGR | 20.5% |

알코올 및 플랫폼 화학 부문은 2024년에 28%의 점유율을 차지했고, 2034년까지 23%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예상됩니다. 이 전망은 회수된 CO2 및 재생가능한 수소 유래 메탄올 및 에탄올의 생산 확대와 관련이 있습니다. 여러 지역의 상업시설은 이미 화학 및 연료 시장의 주요 원료가되는 재생 가능 메탄올을 생산하고 있습니다.

촉매 수소화 부문은 2024년에 32%의 점유율을 차지했고 2034년까지 22.5%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예측되고 있습니다. 그것의 상업적 가능성은 성숙한 촉매 시스템, 명확하게 정의된 공정 설계, 입증된 산업 도입에 의해 지원됩니다. 구리(Cu), 산화아연(ZnO), 산화알루미늄(Al2O3)을 주성분으로 하는 차세대 메탄올 합성 촉매는 기존 공정과 동등한 수율을 달성하면서 99% 이상의 선택성 수준에 도달하고 있습니다. 코발트와 철을 기반으로 하는 촉매 시스템은 CO2 유래의 합성 가스를 합성 탄화수소로 변환 가능하며, 운전 조건의 조정에 의해 출력을 최적화할 수 있습니다.

건설 분야는 2024년에 20%의 점유율을 차지했고, CAGR 25%로 성장할 전망입니다. 수요 증가는 CO2 강화 콘크리트 재료와 저탄소 시멘트의 채택 확대에 견인되고 있습니다. 주요 지역의 인프라 투자가 증가함에 따라 저 배출형 건축자재에 대한 엄격한 사양이 도입되어 시장의 기세를 강화하고 있습니다.

유럽의 탄소 포집 활용 화학제품 시장은 대규모 탄소 관리를 촉진하는 주요 기후 정책에 힘입어 2024년 32%의 점유율을 차지했습니다. 지역 이니셔티브에서는 2030년까지 CO2 저장 용량을 연간 5,000만 톤으로 확대하는 것을 목표로 함과 동시에, 2040년까지 연간 회수량 2억 8,000만 톤을 목표로 하는 국경 간 CO2 상품 시장의 개발을 장기 계획으로 내걸고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 유형별

- 장래 시장 동향

- 기술과 혁신 동향

- 현재의 기술 동향

- 신규기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추정 및 예측 : 제품 유형별, 2021-2034

- 주요 동향

- 알코올 및 플랫폼 화학제품

- 폴리머 및 플라스틱

- 올레핀 및 탄화수소

- 합성가스 및 중간체

- 건축자재· 골재

- 특수화학제품 및 기타 화학제품

제6장 시장추정 및 예측 : 기술별, 2021-2034

- 주요 동향

- 전기화학적 변환

- 촉매 수소화

- 가스 발효 및 생물학적 변환

- 열화학 변환

- 광물화 및 탄산화

- 직접 화학 합성

제7장 시장 추정 및 예측 : 최종 이용 산업별, 2021-2034

- 주요 동향

- 자동차

- 내부 부품

- 외장 부품

- 엔진 룸내 용도

- 건설 및 건축

- 주택건설

- 상업 빌딩

- 인프라·토목 공사

- 포장

- 식품 및 음료 포장

- 산업용 포장

- 소비재 포장

- 화학제품 및 석유화학제품

- 기초화학제품 제조

- 특수화학제품

- 농약

- 항공

- 상용항공

- 화물·수송

- 군 및 방위

- 헬스케어

- 의료기기

- 의약품 포장

- 병원·임상 용품

- 농업

- 작물 생산

- 비료·토양 개량제

- 농업용 기기

- 전자기기 및 소비재

- 가전제품

- 가전제품

- 스포츠 용품

제8장 시장추정 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Air Liquide SA

- Aker Carbon Capture ASA

- Avantium NV

- BASF SE

- Blue Planet Systems Corporation

- Carbon Clean Solutions Ltd.

- Carbon Recycling International(CRI)

- Carbon Upcycling Technologies Inc.

- CarbonCure Technologies Inc.

- Climeworks AG

- Covestro AG

- Econic Technologies Ltd.

- LanzaTech Global, Inc.

- Liquid Wind AB

- Mitsubishi Chemical Group Corporation

- Novomer Inc.

- SABIC

- SK Innovation Co., Ltd.

- Solidia Technologies, Inc.

- TotalEnergies SE

- Others

The Global Carbon Capture Utilization Chemicals Market was valued at USD 58.5 billion in 2024 and is estimated to grow at a CAGR of 20.5% to reach USD 476.3 billion by 2034.

Companies across the world are prioritizing low-carbon and carbon-negative materials as part of their long-term net-zero strategies, leading to rising demand for solutions produced from captured carbon dioxide. Manufacturers are broadening procurement goals for lower-emission materials, and multiple industries are adopting CO2-based products to cut supply-chain emissions. Accelerated advancements in catalysis, electrolysis, and system integration are lowering costs and improving performance, supported by emerging catalyst technologies that deliver stronger efficiency and stability in CO2 conversion. High-performance electrolysis systems are achieving increased current densities, which reduces capital investment through compact system design. The market is also shifting from small-scale demonstrations to full commercial operations, with integrated production models combining renewable hydrogen, concentrated CO2 sources, and bioenergy systems to create powerful pathways for deployment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $58.5 Billion |

| Forecast Value | $476.3 Billion |

| CAGR | 20.5% |

The alcohols and platform chemicals segment held 28% share in 2024 and is projected to grow at a 23% CAGR by 2034. This outlook is linked to expanding production of methanol and ethanol derived from captured CO2 and renewable hydrogen. Commercial facilities in multiple regions are already producing renewable methanol that serves as a key feedstock for chemical and fuel markets.

The catalytic hydrogenation segment accounted for 32% share in 2024 and is anticipated to grow at a CAGR of 22.5% through 2034. Its commercial potential is supported by mature catalyst systems, well-defined process designs, and proven industrial implementation. Next-generation methanol synthesis catalysts featuring Cu, ZnO, and Al2O3 compositions are reaching selectivity levels above 99% while achieving yields like conventional processes. Catalyst systems based on cobalt and iron enable the conversion of CO2-derived syngas into synthetic hydrocarbons, with output tailored by adjusting operating conditions.

The construction segment held 20% share in 2024 and is projected to grow at a CAGR of 25%. Demand growth is driven by expanding adoption of CO2-enhanced concrete materials and low-carbon cement. Increasing investments in infrastructure across major regions are incorporating stricter specifications for lower-emission building inputs, which is strengthening market momentum.

Europe Carbon Capture Utilization Chemicals Market held 32% share in 2024, supported by major climate policies designed to promote large-scale carbon management. Regional initiatives aim to expand CO2 storage capacity to 50 million tons per year by 2030, alongside long-term plans to develop a cross-border CO2 commodity market by 2040 targeting 280 million tons in annual capture.

Prominent companies operating in the Global Carbon Capture Utilization Chemicals Market include Climeworks AG, Aker Carbon Capture ASA, Carbon Upcycling Technologies Inc., Covestro AG, Air Liquide S.A., Liquid Wind AB, Econic Technologies Ltd., Blue Planet Systems Corporation, Carbon Recycling International (CRI), SK Innovation Co., Ltd., TotalEnergies SE, CarbonCure Technologies Inc., BASF SE, LanzaTech Global, Inc., Solidia Technologies, Inc., Avantium N.V., Carbon Clean Solutions Ltd., Mitsubishi Chemical Group Corporation, Novomer Inc., and SABIC. Leading players in the Carbon Capture Utilization Chemicals Market are strengthening their competitive position by scaling commercial production capacity, forming long-term partnerships across industrial value chains, and investing heavily in next-generation catalyst and electrolysis technologies. Many companies are also optimizing integrated systems that combine captured CO2 with renewable hydrogen to reduce production costs and improve system efficiency. Strategic collaborations with energy, chemical, and construction firms help streamline offtake agreements and secure stable demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Technology

- 2.2.4 End Use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Alcohols & platform chemicals

- 5.3 Polymers & plastics

- 5.4 Olefins & hydrocarbons

- 5.5 Syngas & intermediates

- 5.6 Building materials & aggregates

- 5.7 Specialty & other chemicals

Chapter 6 Market Estimates and Forecast, By Technology, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Electrochemical conversion

- 6.3 Catalytic hydrogenation

- 6.4 Gas fermentation & biological conversion

- 6.5 Thermochemical conversion

- 6.6 Mineralization & carbonation

- 6.7 Direct chemical synthesis

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.2.1 Interior components

- 7.2.2 Exterior components

- 7.2.3 Under-the-hood applications

- 7.3 Construction & building

- 7.3.1 Residential construction

- 7.3.2 Commercial buildings

- 7.3.3 Infrastructure & civil engineering

- 7.4 Packaging

- 7.4.1 Food & beverage packaging

- 7.4.2 Industrial packaging

- 7.4.3 Consumer goods packaging

- 7.5 Chemicals & petrochemicals

- 7.5.1 Base chemicals production

- 7.5.2 Specialty chemicals

- 7.5.3 Agrochemicals

- 7.6 Aviation

- 7.6.1 Commercial aviation

- 7.6.2 Cargo & freight

- 7.6.3 Military & defense

- 7.7 Healthcare

- 7.7.1 Medical devices

- 7.7.2 Pharmaceutical packaging

- 7.7.3 Hospital & clinical supplies

- 7.8 Agriculture

- 7.8.1 Crop production

- 7.8.2 Fertilizers & soil amendments

- 7.8.3 Agricultural equipment

- 7.9 Electronics & consumer goods

- 7.9.1 Consumer electronics

- 7.9.2 Home appliances

- 7.9.3 Sporting goods

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Air Liquide S.A.

- 9.2 Aker Carbon Capture ASA

- 9.3 Avantium N.V.

- 9.4 BASF SE

- 9.5 Blue Planet Systems Corporation

- 9.6 Carbon Clean Solutions Ltd.

- 9.7 Carbon Recycling International (CRI)

- 9.8 Carbon Upcycling Technologies Inc.

- 9.9 CarbonCure Technologies Inc.

- 9.10 Climeworks AG

- 9.11 Covestro AG

- 9.12 Econic Technologies Ltd.

- 9.13 LanzaTech Global, Inc.

- 9.14 Liquid Wind AB

- 9.15 Mitsubishi Chemical Group Corporation

- 9.16 Novomer Inc.

- 9.17 SABIC

- 9.18 SK Innovation Co., Ltd.

- 9.19 Solidia Technologies, Inc.

- 9.20 TotalEnergies SE

- 9.21 Others