|

시장보고서

상품코드

1885818

윌슨병 치료 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Wilsons Disease Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

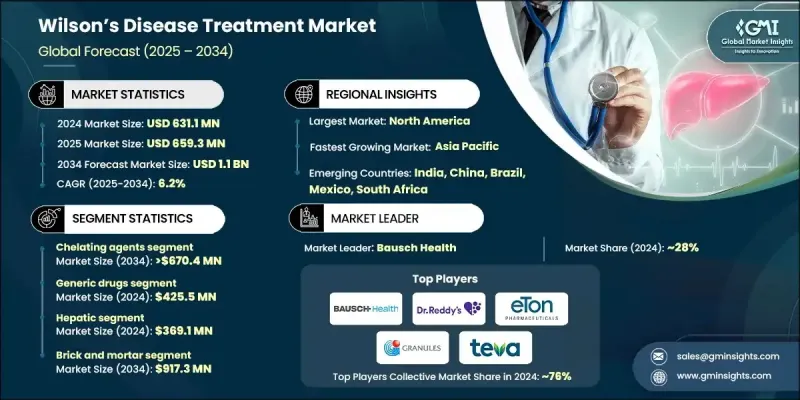

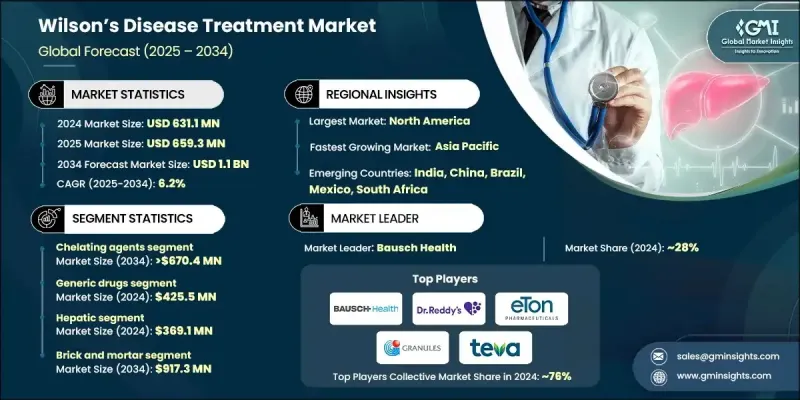

세계의 윌슨병 치료 시장은 2024년에 6억 3,110만 달러로 평가되었고, 2034년까지 6.2%의 연평균 복합 성장률(CAGR)로 성장할 전망이며, 11억 달러에 이를 것으로 예측되고 있습니다.

시장 확대는 질병 유병률 증가, 임상 인식 향상, 킬레이트 요법 및 아연 기반 치료법의 보급, 그리고 의약품 개발의 꾸준한 진보에 의해 지속적으로 형성되고 있습니다. 전문의료 및 다분야에 걸친 치료 센터에 대한 액세스가 확대되고 있는 것도, 장기 치료의 도입을 뒷받침하고 있습니다. 윌슨병 치료는 구리의 조절 기능에 유전적 결함이 있기 때문에 과도하게 축적된 구리의 관리에 중점을 두고 있으며, 주로 배설을 촉진하거나 흡수를 감소시키는 킬레이트제 및 아연 제제에 의존하고 있습니다. 이러한 치료법은 환자의 삶을 통해 건강한 구리 수준을 유지하면서 장기, 특히 간과 중추 신경계를 보호하는 것을 목표로 합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 시 가치 | 6억 3,110만 달러 |

| 예측 금액 | 11억 달러 |

| CAGR | 6.2% |

킬레이트제는 가이드라인에서 오랜 역할과 과도한 구리를 신속하게 제거하는 능력으로 인해 2024년에 60%의 점유율을 차지했습니다. 신경학적 합병증 및 간 합병증 모두를 다루는 그것의 효과는 세계 의사의 지속적인 선호를 지원합니다. 트리엔틴과 페니실라민과 같은 약물에 대한 지속적인 의존은 강력하고 일관된 세계 수요를 뒷받침합니다.

제네릭 의약품 카테고리는 2024년에 4억 2,550만 달러를 획득했으며, 2034년까지 연평균 복합 성장률(CAGR) 6.3%로 성장할 것으로 예측됩니다. 널리 사용되는 킬레이트제 및 아연 요법의 저비용 버전은 합리적인 가격이라는 큰 이점을 가지고 있으며, 치료는 평생 지속되어야 하므로 환자의 지속적인 복약 준수를 지원합니다. 몇몇 치료법의 특허가 만료됨에 따라, 보다 폭넓은 제조업체가 시장에 진입할 수 있게 되어, 비용 중시의 헬스케어 시스템에 있어서의 이용 가능성이 높아지고 있습니다.

미국 윌슨병 치료 시장은 2024년에 2억 2,860만 달러를 창출했습니다. 북미는 유전자 분석, 생화학적 검사, 영상 진단 도구 등의 진단 인프라가 정비되어 있어 시기 적절한 질병의 발견이 가능해지고 있습니다. 조기 진단률이 향상됨에 따라 치료 개시가 확대되고 시장의 지속적인 성장을 지원합니다. 또한 규제 당국의 승인과 강력한 공급망에 의해 지원되며, 이 지역 전체에서 브랜드 의약품 및 제네릭 의약품을 광범위하게 입수할 수 있어 신뢰할 수 있는 치료가 확보되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 킬레이트제 및 아연 기반 요법의 보급 확대

- 희귀질환용 의약품의 지정 확대 및 규제 지원

- 치료 준수율 향상 및 모니터링 툴의 진보

- 임상 지침 개선 및 치료 표준화

- 업계의 잠재적 위험 및 과제

- 브랜드 의약품 및 희귀의약품의 높은 비용

- 환자수가 한정되어 있어 낮츤 상업적 매력

- 시장 기회

- 차세대 킬레이트제 및 안전성 향상 제제의 도입

- 유전자 치료 및 근치의 조사에 대한 주목의 고조

- 성장 촉진요인

- 성장 가능성 분석

- 상환 시나리오

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술 동향

- 현재의 기술 동향

- 신흥 기술

- 소비자 인사이트

- 파이프라인 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 장래 시장 동향

- 임상시험 시나리오

- 갭 분석

제4장 경쟁 구도

- 서문

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신규 치료법의 도입

- 확대 계획

제5장 시장 추계 및 예측 : 치료법별(2021-2034년)

- 주요 동향

- 킬레이트제

- D-페니실라민

- 염산트리엔틴

- 트리엔틴 염산염 사염산염

- 디메르카프롤

- 아연염류

- 아세트산아연

- 황산아연

- 병용 요법

제6장 시장 추계 및 예측 : 의약품 유형별(2021-2034년)

- 주요 동향

- 제네릭 의약품

- 브랜드 의약품

제7장 시장 추계 및 예측 : 적응증별(2021-2034년)

- 주요 동향

- 간 질환

- 신경 및 정신질환

- 기타 적응증

제8장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 점포

- 전자상거래

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Bausch Health

- Biophore

- Breckenridge Pharmaceutical

- Dr. Reddy’s Laboratories

- Eton Pharmaceuticals

- GRANULES

- Invagen Pharmaceuticals

- Nobelpharma

- Optimus Pharma

- Orphalan

- TAJ PHARMA

- Teva Pharmaceutical

- TSUMURA

- Zydus Group

The Global Wilsons Disease Treatment Market was valued at USD 631.1 million in 2024 and is estimated to grow at a CAGR of 6.2% to reach USD 1.1 billion by 2034.

Market expansion continues to be shaped by rising disease prevalence, improved clinical awareness, broader use of chelation and zinc-based therapies, and steady advancements in drug development. Increasing access to specialty care and multidisciplinary treatment centers also supports stronger adoption of long-term therapy. Wilson's disease treatment focuses on managing excessive copper buildup caused by inherited defects in copper regulation, relying mainly on chelators and zinc formulations that enhance excretion or reduce absorption. These therapies aim to protect organs-most critically the liver and central nervous system-while sustaining healthy copper levels throughout a patient's lifetime.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $631.1 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 6.2% |

The chelating agents held a 60% share in 2024 owing to their longstanding role in guidelines and their ability to rapidly clear excess copper. Their effectiveness in addressing both neurological and hepatic complications supports ongoing physician preference worldwide. The continued reliance on agents such as trientine and penicillamine reinforces strong, consistent global demand.

The generic drugs category captured USD 425.5 million in 2024 and is expected to grow at a CAGR of 6.3% through 2034. Lower-cost versions of widely used chelators and zinc therapies provide significant affordability advantages, supporting sustained patient adherence since treatment must be maintained lifelong. Patent expirations across several therapies have enabled a broader range of manufacturers to enter the market, increasing availability within cost-sensitive healthcare systems.

U.S. Wilsons Disease Treatment Market generated USD 228.6 million in 2024. North America benefits from a strong diagnostic infrastructure, including widespread use of genetic analysis, biochemical testing, and imaging tools, enabling more timely detection of the condition. As early diagnosis rates rise, therapy initiation expands, supporting sustained market growth. Broad access to branded and generic medications across the region also ensures reliable treatment availability, supported by regulatory approvals and strong supply chains.

Prominent companies active in the Global Wilsons Disease Treatment Market include Breckenridge Pharmaceutical, Nobelpharma, TAJ PHARMA, Dr. Reddy's Laboratories, TSUMURA, Teva Pharmaceutical, Zydus Group, Bausch Health, Eton Pharmaceuticals, Optimus Pharma, Biophore, Granules, Invagen Pharmaceuticals, and Orphalan. Companies competing in the Global Wilsons Disease Treatment Market are strengthening their market foothold through multiple strategies. Many firms are expanding their portfolios of chelators and zinc-based formulations to meet increasing therapeutic demand and widen patient access. Investments in improved drug delivery systems aim to enhance tolerability and long-term adherence, especially for chronic management. Manufacturers are also emphasizing cost-efficient production to support competitive pricing in both branded and generic segments. Collaborations with clinical research groups help advance next-generation treatments and support evidence-based positioning.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Treatment type trends

- 2.2.3 Drug type trends

- 2.2.4 Indication trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising availability of chelating agents and zinc-based therapies

- 3.2.1.2 Expansion of orphan drug designations and regulatory support

- 3.2.1.3 Advancements in treatment adherence and monitoring tools

- 3.2.1.4 Improved clinical guidelines and treatment standardization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of branded and orphan-designated drugs

- 3.2.2.2 Limited patient population and low commercial attractiveness

- 3.2.3 Market opportunities

- 3.2.3.1 Introduction of next-generation chelators and safer formulations

- 3.2.3.2 Growing focus on gene therapy and curative research

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Reimbursement scenario

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.6 Technology landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Consumer insights

- 3.8 Pipeline analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

- 3.12 Clinical trial scenario

- 3.13 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New treatment type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Chelating agents

- 5.2.1 D-penicillamine

- 5.2.2 Trientine hydrochloride

- 5.2.3 Trientine tetrahydrochloride

- 5.2.4 Dimercaprol

- 5.3 Zinc salts

- 5.3.1 Zinc acetate

- 5.3.2 Zinc sulfate

- 5.4 Combination therapy

Chapter 6 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Generic drugs

- 6.3 Branded drugs

Chapter 7 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hepatic

- 7.3 Neurological and psychiatric

- 7.4 Other indications

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Brick and mortar

- 8.3 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bausch Health

- 10.2 Biophore

- 10.3 Breckenridge Pharmaceutical

- 10.4 Dr. Reddy’s Laboratories

- 10.5 Eton Pharmaceuticals

- 10.6 GRANULES

- 10.7 Invagen Pharmaceuticals

- 10.8 Nobelpharma

- 10.9 Optimus Pharma

- 10.10 Orphalan

- 10.11 TAJ PHARMA

- 10.12 Teva Pharmaceutical

- 10.13 TSUMURA

- 10.14 Zydus Group