|

시장보고서

상품코드

1885832

중기 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Heavy Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

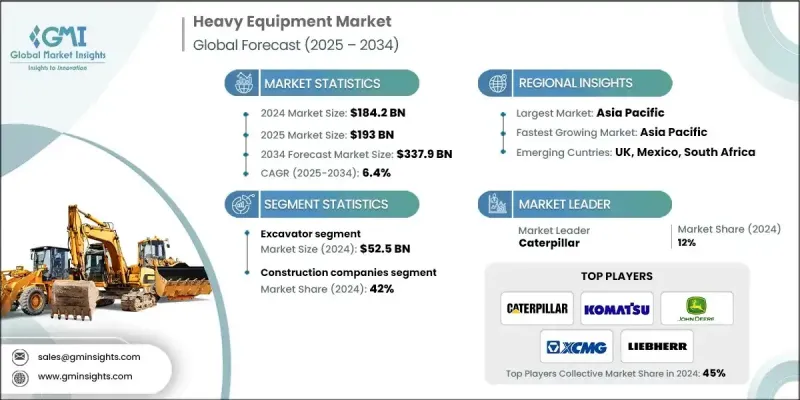

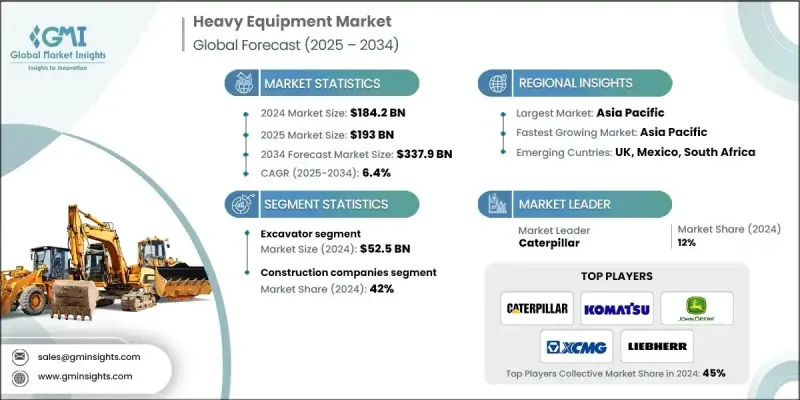

세계의 중기 시장은 2024년에 1,842억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 6.4%로 성장할 전망이며, 3,379억 달러에 달할 것으로 예측되고 있습니다.

이 시장은 도시화, 자원 이동, 경제 확대의 기반으로 세계 인프라 및 산업 발전을 지원하는 중요한 역할을 담당하고 있습니다. 주요 용도는 건설, 광업, 농업, 자재 운반 및 이들은 세계 성장에 매우 중요한 분야입니다. 수요는 도로, 에너지 프로젝트, 주택에 상당한 투자를 하는 신흥 경제국에 의해 견인되고 있습니다. 한편, 성숙시장에서는 연료 효율이 뛰어나고 디지털 접속되어 기술적으로 선진적인 기계에 의한 플릿의 현대화가 진행되고 있습니다. 자동화, 텔레매틱스 및 전기화는 업무를 변화시키고 기업이 지속가능성 목표를 달성하는 동시에 운영 비용을 절감할 수 있도록 지원합니다. 효율성 및 생산성에 대한 주목의 향상과 기술 통합이 결합되어 중기의 상황이 재구축되어 업계 전체에서 보다 스마트하고 친환경적인 업무가 가능하게 되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 시 가치 | 1,842억 달러 |

| 예측 금액 | 3,379억 달러 |

| CAGR | 6.4% |

렌탈 분야는 기업이 유연하고 비용 효율적인 솔루션을 찾고, 다액의 선행 투자를 회피하는 경향이 있기 때문에 견조한 성장을 보이고 있습니다. 그러나 업계는 원재료 가격 변동, 노동력 부족, 배출 규제 강화 등의 과제에 직면하고 있으며, 제조업체는 컴플라이언스와 경쟁력을 유지하면서 혁신의 가속을 강요하고 있습니다. 이러한 문제가 있음에도 불구하고 시장 전망은 계속 견조합니다.

건설 회사 부문은 2024년에 42%의 점유율을 차지했습니다. 굴삭기, 로더, 불도저, 크레인 등의 기계는 토공 작업, 자재 운반, 현장 준비, 구조물 조립에 널리 사용됩니다. 도시화의 진전 및 정부 인프라 프로젝트는 이러한 기계에 대한 수요를 꾸준히 밀어 올리고 있습니다.

디젤 구동기기 부문은 높은 토크, 신뢰성, 건설 및 광업, 농업 분야에서의 실적을 배경으로 2024년에 큰 점유율을 획득했습니다. 디젤 엔진은 정비된 연료 공급 인프라, 장거리 가동 능력, 조작자의 숙련도 등의 장점을 가지고 있으며, 충전 네트워크가 제한되는 원격지나 접근하기 어려운 지역에서 필수적입니다. 지속적인 무거운 작업에는 여전히 디젤이 중요시되고 있습니다.

2024년 미국 중장비 시장은 392억 달러로 82%의 점유율을 차지했습니다. 이 지역에서는 선진기계, 자동화, 텔레매틱스가 중시되어 대규모 인프라 및 광업 프로젝트가 수요를 견인하고 있습니다. 지속적인 연구개발 투자는 북미 세계 시장에서의 지위를 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 인프라 정비 및 도시화

- 기술적 진보 및 자동화

- 지속가능성 및 배출 규제

- 업계의 잠재적 위험 및 과제

- 높은 초기 투자 및 유지 관리 비용

- 공급망의 혼란 및 원재료 가격의 변동성

- 기회

- 전동화 및 환경에 배려한 설비 솔루션

- 디지털화 및 예지보전

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 기종별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 기종별(2021-2034년)

- 주요 동향

- 굴삭기

- 크레인

- 백호 로더

- 불도저 및 도저

- 휠 로더

- 모터 그레이더

- 덤프 트럭

- 컴팩터 및 롤러

- 기타

제6장 시장 추계 및 예측 : 이동성별(2021-2034년)

- 주요 동향

- 이동식 설비

- 거치형 설비

- 반이동식 설비

제7장 시장 추계 및 예측 : 전원별(2021-2034년)

- 주요 동향

- 디젤식

- 전기식

- 하이브리드식

제8장 시장 추계 및 예측 : 용도별 2021-2034

- 주요 동향

- 건설

- 광업

- 인프라 개발

- 공업제조

- 자재 운반

- 해체

- 기타(농업, 임업, 유틸리티 등)

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 건설회사

- 렌탈 서비스 제공업체

- 광업 회사

- 인프라 개발 사업자

- 제조 공장

- 기타(유틸리티, 정부기관 등)

제10장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매

- 간접 판매

제11장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 프로파일

- Caterpillar Inc.

- Doosan Infracore(now Develon)

- Hitachi Construction Machinery

- Hyundai Construction Equipment(now HD Hyundai Construction Equipment)

- JCB

- John Deere

- Komatsu Ltd.

- Liebherr Group

- Manitowoc Company

- Sany Heavy Industry

- Tadano Ltd.

- Terex Corporation

- Volvo Construction Equipment

- XCMG Group

- Zoomlion Heavy Industry

The Global Heavy Equipment Market was valued at USD 184.2 billion in 2024 and is estimated to grow at a CAGR of 6.4% to reach USD 337.9 billion by 2034.

The market plays a critical role in supporting global infrastructure and industrial development, acting as a backbone for urbanization, resource movement, and economic expansion. Its primary applications span construction, mining, agriculture, and material handling, sectors that are pivotal for growth worldwide. Demand is being led by emerging economies investing heavily in roads, energy projects, and housing, while established markets are modernizing fleets with fuel-efficient, digitally connected, and technologically advanced machinery. Automation, telematics, and electrification are transforming operations, helping companies achieve sustainability goals while reducing operational costs. The growing emphasis on efficiency and productivity, coupled with technological integration, is reshaping the heavy equipment landscape and enabling smarter, greener operations across industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $184.2 Billion |

| Forecast Value | $337.9 Billion |

| CAGR | 6.4% |

The rental segment is witnessing strong growth as companies seek flexible, cost-effective solutions, avoiding large upfront investments. However, the industry faces challenges, including fluctuating raw material prices, labor shortages, and stricter emission regulations, which are pushing manufacturers to accelerate innovation while maintaining compliance and competitiveness. Despite these challenges, the market outlook remains strong.

The construction companies segment held 42% share in 2024. Machinery such as excavators, loaders, bulldozers, and cranes is heavily utilized in earthmoving, material handling, site preparation, and structural assembly. Rising urbanization and government infrastructure projects are steadily boosting demand for these machines.

The diesel-powered equipment segment generated significant share in 2024, supported by high torque, reliability, and established performance in construction, mining, and agricultural operations. Diesel engines benefit from a well-developed fuel supply infrastructure, extended operational range, and operator familiarity, making them essential in remote or hard-to-access areas where electric charging networks are limited. Diesel remains critical for continuous heavy-duty operations.

U.S. Heavy Equipment Market held 82% share with USD 39.2 billion in 2024. The region emphasizes advanced machinery, automation, and telematics, with large-scale infrastructure and mining projects driving high demand. Strong replacement demand and a mature rental equipment sector ensure steady revenue streams, while ongoing investment in research and development reinforces North America's global market position.

Major players in the Global Heavy Equipment Market include Hitachi Construction Machinery, Tadano Ltd., Volvo Construction Equipment, Liebherr Group, Komatsu Ltd., Sany Heavy Industry, Caterpillar Inc., Zoomlion Heavy Industry, JCB, John Deere, Develon (formerly Doosan Infracore), Terex Corporation, HD Hyundai Construction Equipment, Manitowoc Company, and other leading manufacturers. Companies in the heavy equipment market are focusing on technological innovation, including automation, telematics, and electrification, to differentiate their products and attract environmentally conscious customers. Strategic partnerships and collaborations with contractors, rental service providers, and fleet operators help expand market reach and strengthen distribution networks. Manufacturers are investing in research and development to improve fuel efficiency, durability, and operational performance while complying with stricter emission regulations. Expanding into high-growth emerging markets ensures access to large infrastructure and industrial projects.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Machine type

- 2.2.3 Mobility

- 2.2.4 Power source

- 2.2.5 Application

- 2.2.6 End Use industry

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Infrastructure development and urbanization

- 3.2.1.2 Technological advancements and automation

- 3.2.1.3 Sustainability and emission regulations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment and maintenance costs

- 3.2.2.2 Supply chain disruptions and raw material volatility

- 3.2.3 Opportunities

- 3.2.3.1 Electrification and green equipment solutions

- 3.2.3.2 Digitalization and predictive maintenance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By machine type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Machine Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Excavators

- 5.3 Cranes

- 5.4 Backhoe Loaders

- 5.5 Bulldozers/Dozers

- 5.6 Wheel loaders

- 5.7 Motor Graders

- 5.8 Dump Trucks

- 5.9 Compactors/Rollers

- 5.10 Others

Chapter 6 Market Estimates and Forecast, By Mobility, 2021 - 2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Mobile equipment

- 6.3 Stationary equipment

- 6.4 Semi-mobile equipment

Chapter 7 Market Estimates and Forecast, By Power Source, 2021 - 2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Diesel-powered

- 7.3 Electric-powered

- 7.4 Hybrid-powered

Chapter 8 Market Estimates and Forecast, By Application 2021 - 2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Construction

- 8.3 Mining

- 8.4 Infrastructure development

- 8.5 Industrial manufacturing

- 8.6 Material handling

- 8.7 Demolition

- 8.8 Others (agriculture, forestry, utilities, etc.)

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Construction companies

- 9.3 Rental service providers

- 9.4 Mining companies

- 9.5 Infrastructure developers

- 9.6 Manufacturing plants

- 9.7 Others (utilities, government, etc.)

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Caterpillar Inc.

- 12.2 Doosan Infracore (now Develon)

- 12.3 Hitachi Construction Machinery

- 12.4 Hyundai Construction Equipment (now HD Hyundai Construction Equipment)

- 12.5 JCB

- 12.6 John Deere

- 12.7 Komatsu Ltd.

- 12.8 Liebherr Group

- 12.9 Manitowoc Company

- 12.10 Sany Heavy Industry

- 12.11 Tadano Ltd.

- 12.12 Terex Corporation

- 12.13 Volvo Construction Equipment

- 12.14 XCMG Group

- 12.15 Zoomlion Heavy Industry