|

시장보고서

상품코드

1885840

산업용 여과 시스템 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Industrial Filtration System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

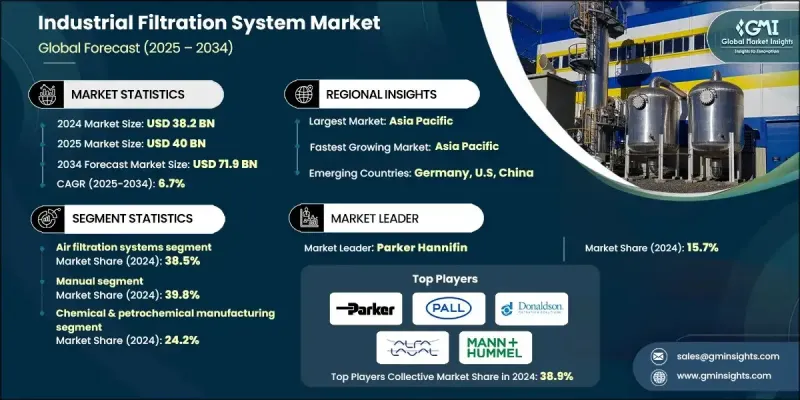

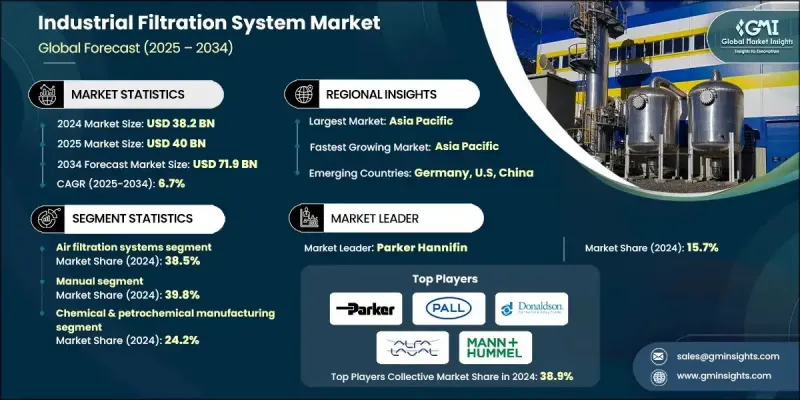

세계의 산업용 여과 시스템 시장은 2024년 382억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 6.7%로 성장할 전망이며, 719억 달러에 이를 것으로 예측되고 있습니다.

규제 요건의 변화, 고객의 요구 진화, 기술 혁신의 진전에 의해 산업 오퍼레이션이 재구축되는 가운데, 시장은 급속히 확대하고 있습니다. 환경 지속가능성은 혁신의 핵심 추진력이 되고, 제조업체 각사는 환경에 배려한 여과재, 에너지 소비 삭감, 장기적인 환경 목표를 지지하는 시스템 설계에 주력하고 있습니다. 고성능 여과 매체에 대한 관심 증가는 부식성, 고온, 고압 환경을 다루는 산업 전체에 있어서, 보다 강한 내구성, 보다 높은 정밀도, 보다 폭넓은 적용성을 가능하게 하고 있습니다. 재료 과학의 진보는 여과 수명 및 신뢰성의 향상을 지속적으로 촉진하고, 점점 엄격화하는 환경 기준의 적합을 확보하는 시스템에 대한 산업 투자를 추진하고 있습니다. 이러한 발전은 전 세계 산업 시설의 자본 배분, 현대화 전략 및 인프라 업그레이드에 영향을 미칩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 시 가치 | 382억 달러 |

| 예측 금액 | 719억 달러 |

| CAGR | 6.7% |

공기 여과 카테고리는 2024년에 38.5%의 점유율을 차지했으며, 2025-2034년 7.4%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다. 이 부문이 주도적인 지위에 있는 배경으로는 배출가스 규제, 직장 안전 요건, 고급 공기 여과 솔루션을 요구하는 환경 가이드라인 등에 대한 세계의 관심이 높아지고 있습니다. 주요 지역의 규제 체제는 근로자를 보호하고 산업 오염물질을 줄이기 위해 고안된 고효율 시스템에 대한 투자에 계속 영향을 미치고 있습니다.

반자동 여과 시스템은 2024년에 107억 달러 시장 규모(공유 28%)를 기록했으며, 2034년까지 연평균 복합 성장률(CAGR) 6.9%로 확대될 것으로 전망됩니다. 이러한 시스템은 자동 모니터링 기능과 운영자 관리 유지보수를 통합한 하이브리드 모델로, 효율성을 높이면서 중요한 기능에 대한 인적 모니터링을 유지합니다. 일관된 검증된 성능이 요구되는 산업 분야에서는 신뢰할 수 있는 여과와 컴플라이언스 기준을 유지하기 위해 이러한 시스템에 대한 의존도가 높아지고 있습니다.

북미의 산업용 여과 시스템 시장은 2024년에 107억 달러(28%의 점유율)에 이르렀으며, 2034년까지 연평균 복합 성장률(CAGR) 6.9%로 추이할 것으로 예측됩니다. 이 지역의 성장은 업데이트 수요, 인프라 업그레이드 및 규제 시행에 의해 지원됩니다. 미국은 엄격한 환경 규제, 노후화된 산업 자산 및 견고한 여과 기술을 필요로 하는 생산 활동 증가로 인해 지역 소비의 대부분을 견인하고 있습니다. 국가 및 주 수준의 가이드라인 준수는 산업 시설 전체에서 투자 우선순위를 형성하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 규제 준수 및 환경 기준

- 산업 성장 및 공정의 고도화

- 기술 진보의 통합

- 업계의 잠재적 위험 및 과제

- 자본 투자 및 운영 비용

- 복잡성 및 노동력 요건의 통합

- 공급망 및 사용후 제품 관리

- 기회

- 지속가능하고 에너지 효율적인 솔루션

- 고도의 용도 분야의 확대

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 제품별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 공기 여과 시스템

- HEPA 필터 및 ULPA 필터

- 전기 집진 장치

- 버그하우스 및 집진장치

- 카트리지 필터 및 패널 필터

- 막 여과 시스템

- 정밀 여과(MF)

- 한외 여과(UF)

- 나노 여과(NF)

- 역삼투(RO)

- 세라믹 막 필터

- 탄화규소(SIC)막

- 알루미나계막

- 지르코니아 및 티타니아막

- 압력 구동식 여과

- 필터 프레스

- 카트리지 필터 및 백 필터

- 진공 여과 시스템

- 이온 교환 및 흡착 시스템

- 활성탄 시스템

- 이온 교환 수지

- 분자체 및 특수 흡착제

제6장 시장 추계 및 예측 : 자동화 레벨별(2021-2034년)

- 주요 동향

- 수동

- 반자동

- 자동화

- IoT는 스마트 시스템을 실현합니다

제7장 시장 추계 및 예측 : 압력 범위별(2021-2034년)

- 주요 동향

- 저압(50 psi 미만)

- 중압(50-500 psi)

- 고압(500 psi 초과)

제8장 시장 추계 및 예측 : 입자 사이즈 범위별(2021-2034년)

- 주요 동향

- 거친 여과(10μm 이상)

- 정밀 여과(1-10μm)

- 초미립자(1μm 미만)

제9장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 대기오염 방지

- 상수도 및 하수 처리

- 프로세스 여과

- 광업 및 미광 관리

- 클린 룸 및 무균 용도

- 유압 및 윤활유 여과

- 압축공기처리

- 가스 정제

- 용제 및 촉매의 회수

제10장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 화학제품 및 석유화학제품 제조

- 의약품 및 바이오테크놀러지

- 식품 및 음료 가공

- 광업 및 금속

- 발전

- 펄프 및 종이

- 자동차 제조

- 항공우주 및 방위

- 석유 및 가스

- 철강 및 1차 금속

- 기타

제11장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제12장 기업 프로파일

- 3M Company

- Ahlstrom-Munksjo

- Alfa Laval AB

- Camfil Group

- Cummins Filtration

- Donaldson Company, Inc.

- Eaton Corporation Plc

- Filtration Group Corporation

- Freudenberg Filtration Technologies

- Lenntech BV

- MANN HUMMEL Group

- Pall Corporation

- Parker Hannifin Corporation

- Pentair Plc

- WL Gore & Associates, Inc.

The Global Industrial Filtration System Market was valued at USD 38.2 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 71.9 billion by 2034.

The market is advancing rapidly as shifting regulatory expectations, evolving customer demands, and ongoing technology upgrades reshape industrial operations. Environmental sustainability has become a central driver of innovation as manufacturers focus on eco-conscious filtration materials, reduced energy consumption, and system designs that support long-term environmental goals. Rising interest in high-performance filtration media is enabling stronger durability, greater precision, and wider applicability across industries dealing with corrosive, high-temperature, or high-pressure environments. Improvements in material science continue to extend filtration lifespan and reliability, encouraging industries to invest in systems that ensure compliance with increasingly strict environmental standards. These advancements are influencing capital allocation, modernization strategies, and infrastructure upgrades across global industrial facilities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $38.2 Billion |

| Forecast Value | $71.9 Billion |

| CAGR | 6.7% |

The air filtration category held a 38.5% share in 2024 and is anticipated to grow at a 7.4% CAGR from 2025 to 2034. This segment leads due to increasing global attention on emission controls, workplace safety requirements, and environmental guidelines that demand advanced air filtration solutions. Regulatory frameworks in major regions continue to influence investment in higher-efficiency systems designed to protect workers and reduce industrial pollutants.

The semi-automatic filtration systems generated USD 10.7 billion in 2024, accounting for a 28% share, and are expected to grow at a CAGR of 6.9% through 2034. These systems integrate automated monitoring features with operator-managed maintenance, offering a hybrid model that enhances efficiency while maintaining human oversight of essential functions. Industries that require consistent, validated performance rely heavily on these systems to support dependable filtration and compliance standards.

North America Industrial Filtration System Market reached USD 10.7 billion in 2024 with a 28% share and is expected to register a 6.9% CAGR through 2034. Growth in this region is supported by replacement demand, infrastructure upgrades, and regulatory enforcement. The United States drives most of the regional consumption due to strict environmental regulations, aging industrial assets, and increasing production activity that requires robust filtration technologies. Compliance with national and state-level guidelines continues to shape investment priorities across industrial facilities.

Leading companies in the Industrial Filtration System Market include Parker Hannifin Corporation, Pall Corporation, Donaldson Company, Inc., Ahlstrom-Munksjo, Eaton Corporation Plc, 3M Company, Lenntech B.V., Pentair Plc, W. L. Gore & Associates, Inc., Alfa Laval AB, Camfil Group, Filtration Group Corporation, MANN+HUMMEL Group, Freudenberg Filtration Technologies, and Cummins Filtration. Major industry players strengthen their competitive standing by expanding filtration portfolios, enhancing material innovation, and investing in advanced, energy-efficient designs. Many companies accelerate R&D to introduce systems with extended durability, improved efficiency, and reduced operational costs. Strategic acquisitions, global distribution partnerships, and facility expansions support broader geographic reach and faster market penetration. Firms also focus on developing filtration technologies that align with evolving environmental and workplace safety regulations, ensuring seamless compliance for end users.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.3 Data collection methods

- 1.4 Data mining sources

- 1.4.1 Global

- 1.4.2 Regional/Country

- 1.5 Base estimates and calculations

- 1.5.1 Base year calculation

- 1.5.2 Key trends for market estimation

- 1.6 Primary research and validation

- 1.6.1 Primary sources

- 1.7 Forecast model

- 1.8 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Automation level

- 2.2.4 Pressure range

- 2.2.5 Particle size range

- 2.2.6 Application

- 2.2.7 End Use

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Regulatory compliance and environmental standards

- 3.2.1.2 Industrial growth and process intensification

- 3.2.1.3 Technological advancement integration

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Capital investment and operational costs

- 3.2.2.2 Integration of complexity and workforce requirements

- 3.2.2.3 Supply chain and end-of-life management

- 3.2.3 Opportunities

- 3.2.3.1 Sustainable and energy-efficient solutions

- 3.2.3.2 Advanced application expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Product

- 3.7 Regulatory landscape

- 3.7.1 standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Thousand Units)

- 5.1 Key trends

- 5.2 Air filtration systems

- 5.2.1 Hepa & Ulpa filters

- 5.2.2 Electrostatic precipitators

- 5.2.3 Baghouse & dust collectors

- 5.2.4 Cartridge & panel filters

- 5.3 Membrane filtration systems

- 5.3.1 Microfiltration (MF)

- 5.3.2 Ultrafiltration (UF)

- 5.3.3 Nanofiltration (NF)

- 5.3.4 Reverse osmosis (RO)

- 5.4 Ceramic membrane filters

- 5.4.1 Silicon carbide (SIC) membranes

- 5.4.2 Alumina-based membranes

- 5.4.3 Zirconia & titania membranes

- 5.5 Pressure-driven filtration

- 5.5.1 Filter presses

- 5.5.2 Cartridge & bag filters

- 5.5.3 Vacuum filtration systems

- 5.6 Ion exchange & adsorption systems

- 5.6.1 Activated carbon systems

- 5.6.2 Ion exchange resins

- 5.6.3 Molecular sieves & specialty adsorbents

Chapter 6 Market Estimates & Forecast, By Automation Level, 2021 - 2034 ($Bn, Thousand Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automatic

- 6.4 Automatic

- 6.5 IoT enables smart system

Chapter 7 Market Estimates & Forecast, By Pressure Range, 2021 - 2034 ($Bn, Thousand Units)

- 7.1 Key trends

- 7.2 Low-pressure (<50 psi)

- 7.3 medium pressure (50-500 psi)

- 7.4 high-pressure (>500 psi)

Chapter 8 Market Estimates & Forecast, By Particle Size Range, 2021 - 2034 ($Bn, Thousand Units)

- 8.1 Key trends

- 8.2 Coarse filtration (>10 im)

- 8.3 Fine filtration (1-10 μm)

- 8.4 Ultrafine (<1 μm)

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Thousand Units)

- 9.1 Key trends

- 9.2 Air pollution control

- 9.3 Water & wastewater treatment

- 9.4 Process filtration

- 9.5 Mining & tailings management

- 9.6 Cleanroom & sterile applications

- 9.7 Hydraulic & lubricant filtration

- 9.8 Compressed air treatment

- 9.9 Gas purification

- 9.10 Solvent & catalyst recovery

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Thousand Units)

- 10.1 Key trends

- 10.2 Chemical & petrochemical manufacturing

- 10.3 Pharmaceutical & biotechnology

- 10.4 Food & beverage processing

- 10.5 Mining & metals

- 10.6 Power generation

- 10.7 Pulp & paper

- 10.8 Automotive manufacturing

- 10.9 Aerospace & defense

- 10.10 Oil & gas

- 10.11 Steel & primary metals

- 10.12 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 3M Company

- 12.2 Ahlstrom-Munksjo

- 12.3 Alfa Laval AB

- 12.4 Camfil Group

- 12.5 Cummins Filtration

- 12.6 Donaldson Company, Inc.

- 12.7 Eaton Corporation Plc

- 12.8 Filtration Group Corporation

- 12.9 Freudenberg Filtration Technologies

- 12.10 Lenntech B.V.

- 12.11 MANN+HUMMEL Group

- 12.12 Pall Corporation

- 12.13 Parker Hannifin Corporation

- 12.14 Pentair Plc

- 12.15 W. L. Gore & Associates, Inc.