|

시장보고서

상품코드

1885848

석유화학 재활용 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Petrochemical Recycling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

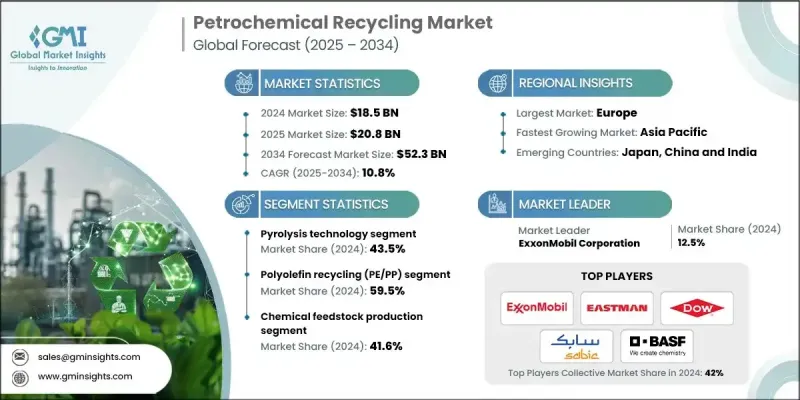

세계의 석유화학 재활용 시장은 2024년 185억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 10.8%로 성장할 전망이며, 523억 달러에 이를 것으로 예측됩니다.

시장의 급성장은 플라스틱 폐기물 관리에서 지속가능한 해결책에 대한 수요 증가와 첨단 화학적 재활용 기술의 진화를 반영합니다. 환경 압력 증가 및 세계 폐기물 규제 강화로 산업계와 정부는 혁신 가속화와 재활용 능력 확대를 촉구하고 있습니다. 화학적 재활용은 기존의 기계적 시스템에서는 효과적으로 처리할 수 없는 혼합 및 오염 플라스틱 폐기물을 유용한 출력물로 변환하는 실현 가능한 수단으로서 주목을 받고 있습니다. 세계 플라스틱 소비량이 증가함에 따라 폐기물 발생량 및 재활용 능력의 격차는 확장 가능한 화학적 재활용 대체 수단에 대한 긴급 수요를 돋보이게 합니다. 주요 지역의 발전과 강력한 정책 지원과 대규모 산업 투자가 결합되어 세계 상황이 재구성되고 있으며, 석유화학 재활용은 순환형 경제의 중요한 구성 요소로서의 지위를 확립하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 시 가치 | 185억 달러 |

| 예측 금액 | 523억 달러 |

| CAGR | 10.8% |

열분해 기술 부문은 2024년에 43.5%의 점유율을 차지하였으며, 2034년까지 연평균 복합 성장률(CAGR) 10.4%로 성장할 것으로 예측됩니다. 그것의 이점은 높은 상업적 실현 가능성 및 무산소 조건 하에서 복잡한 중합체 구조를 분해하고 정제 가능한 탄화수소 제품을 생산하는 능력에 기인합니다. 혼합 플라스틱 및 오염 플라스틱에 대한 유연한 대응 능력에 의해 기계적 재활용으로는 처리할 수 없는 폐기물 스트림의 처리에 필수적인 기술이 되고 있습니다. 시설 네트워크의 확대 및 지속적인 투자 지원은 업계의 높은 수용성을 뒷받침합니다.

폴리올레핀 재활용 분야는 2024년에 59.5%의 점유율을 차지하였으며, 2025-2034년 CAGR 10.5%로 성장할 것으로 예측됩니다. 폴리에틸렌과 폴리프로필렌과 같은 소재는 세계 포장 생산에 있어서 다용도로 주도적인 지위를 유지하고 있습니다. 이러한 열가소성 특성은 열분해 및 가스화와 같은 변환 기술과의 높은 호환성을 만들어 내고 귀중한 탄화수소 유도체로의 효율적인 전환을 촉진합니다.

북미의 석유화학 재활용 시장은 2024년 24.8%의 점유율을 차지했습니다. 이 지역은 신뢰할 수 있는 폐기물 수집 시스템, 산업 투자, 재생재 채용을 촉진하는 지원 규제 조치의 혜택을 받고 있습니다. 생산자 책임을 강화하고 매립폐기물을 줄이기 위한 정책은 시장 성장을 가속하고 화학적 재활용 물질에 대한 장기적인 수요를 자극하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 확대 생산자 책임(EPR)의 의무화

- 재생재 함유율의 요건 및 규제

- 플라스틱 폐기물 위기와 환경 문제

- 업계의 잠재적 위험 및 과제

- 많은 자본 투자 필요

- 기술적 과제 및 품질 제약

- 시장 기회

- 정부 자금 및 투자 프로그램

- 아시아태평양의 신흥 시장으로 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 기술 유형별

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가만 제공)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국 고려

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 기술 유형별(2021-2034년)

- 주요 동향

- 열분해 기술

- 기존 열분해 시스템

- 촉매를 이용한 고도의 열분해

- 마이크로파 보조 열분해

- 탈중합(케모리시스)

- 용해 분해 프로세스

- PET 재활용을 위한 글리콜 분해

- 효소 분해에 의한 탈중합

- 촉매 분해

- 가스화 기술

- 공기 취입식 가스화 시스템

- 산소 불어 가스화

- 증기 가스화 공정

- 플라즈마 가스화 기술

- 용해 및 용제 베이스의 리사이클

- 선택적 용해 기술

- 용제 회수 및 정제

제6장 시장 추계 및 예측 : 원료 유형별(2021-2034년)

- 주요 동향

- 폴리올레핀 재활용(PE/PP)

- 고밀도 폴리에틸렌(HDPE) 재활용

- 저밀도 폴리에틸렌(LDPE) 재활용

- 폴리프로필렌(PP) 재활용

- 혼합 폴리올레핀 스트림

- PET 재활용

- 병에서 병으로의 재활용

- 섬유에서 섬유로의 용도

- 식품 등급 PET 재활용

- 착색 PET의 가공

- 혼합 플라스틱 폐기물의 재활용

- 다층 포장 재료

- 오염 플라스틱 원료

- 전자 폐기물 플라스틱

- 자동차용 플라스틱 부품

- 특수 폴리머의 재활용

- 엔지니어링 플라스틱의 재활용

- 열경화성 플라스틱 가공

- 복합재료의 재활용

- 바이오베이스 폴리머의 재활용

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 화학 원료 생산

- 연료 생산 용도

- 신규 폴리머 생산

- 특수 제품 제조

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- ExxonMobil Corporation

- Eastman Chemical Company

- Dow Inc.

- SABIC(Saudi Basic Industries Corporation)

- BASF SE

- LyondellBasell Industries

- PETRONAS Chemicals Group

- Plastic Energy

- Agilyx Corporation

- Pyrowave Inc.

- Recycling Technologies Ltd

- Brightmark LLC

- Quantafuel ASA

- Carbios SA

The Global Petrochemical Recycling Market was valued at USD 18.5 billion in 2024 and is estimated to grow at a CAGR of 10.8% to reach USD 52.3 billion by 2034.

The market's rapid rise reflects the growing need for sustainable solutions to manage plastic waste and the increasing refinement of advanced chemical recycling technologies. Rising environmental pressures and stricter global waste regulations are pushing industries and governments to accelerate innovation and expand recycling capacity. Chemical recycling is gaining traction as it provides a viable pathway for converting mixed and contaminated plastic waste into usable outputs that traditional mechanical systems cannot process effectively. As plastic consumption continues to climb worldwide, the gap between waste generation and recycling capacity highlights the urgent demand for scalable chemical recycling alternatives. Progress across major regions, combined with strong policy backing and substantial industrial investments, is reshaping the global landscape and positioning petrochemical recycling as a critical component of the circular economy.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.5 Billion |

| Forecast Value | $52.3 Billion |

| CAGR | 10.8% |

The pyrolysis technology segment held 43.5% share in 2024 and is anticipated to grow at a CAGR of 10.4% through 2034. Its dominance stems from its high commercial readiness and ability to break down complex polymer structures under oxygen-free conditions, yielding hydrocarbon products that can be refined. Its flexibility with mixed and contaminated plastics makes it essential for processing waste streams that mechanical recycling cannot accommodate. Its growing network of facilities and consistent investment support confirm its strong industry acceptance.

The polyolefin recycling segment accounted for a 59.5% share in 2024 and is expected to grow at a CAGR of 10.5% from 2025 to 2034. Materials such as polyethylene and polypropylene maintain a leading position due to their heavy use in global packaging production. Their thermoplastic properties make them highly compatible with conversion technologies such as pyrolysis and gasification, facilitating efficient transformation into valuable hydrocarbon derivatives.

North America Petrochemical Recycling Market held a 24.8% share in 2024. This region benefits from reliable waste collection systems, industry investments, and supportive regulatory measures that encourage recycled content adoption. Policies aimed at strengthening producer responsibility and reducing landfill waste reinforce market growth and stimulate long-term demand for chemically recycled materials.

Key companies in the Petrochemical Recycling Market include PETRONAS Chemicals Group, Quantafuel ASA, ExxonMobil Corporation, Plastic Energy, LyondellBasell Industries, Recycling Technologies Ltd., BASF SE, Eastman Chemical Company, Agilyx Corporation, Brightmark LLC, Pyrowave Inc., Dow Inc., Carbios SA, and SABIC (Saudi Basic Industries Corporation). Companies in the Petrochemical Recycling Market enhance their competitive standing by investing in advanced depolymerization technologies, expanding plant capacity, and forming long-term feedstock agreements to ensure stable input supply. Many firms pursue collaborations with packaging producers and petrochemical manufacturers to integrate recycled outputs directly into product value chains. Strategic partnerships accelerate technology development and support commercialization at scale. Organizations also increase R&D spending to improve process efficiency, reduce energy consumption, and enhance the purity of recycled hydrocarbons.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology type

- 2.2.3 Feedstock type

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Extended producer responsibility (EPR) mandates

- 3.2.1.2 Recycled content requirements & regulations

- 3.2.1.3 Plastic waste crisis & environmental concerns

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital investment requirements

- 3.2.2.2 Technical challenges & quality constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Government funding & investment programs

- 3.2.3.2 Emerging market expansion in Asia-Pacific

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By technology type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Technology Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pyrolysis technology

- 5.2.1 Conventional pyrolysis systems

- 5.2.2 Advanced pyrolysis with catalysts

- 5.2.3 Microwave-assisted pyrolysis

- 5.3 Depolymerization (chemolysis)

- 5.3.1 Solvolysis processes

- 5.3.2 Glycolysis for PET recycling

- 5.3.3 Enzymatic depolymerization

- 5.3.4 Catalytic depolymerization

- 5.4 Gasification technology

- 5.4.1 Air-blown gasification systems

- 5.4.2 Oxygen-blown gasification

- 5.4.3 Steam gasification processes

- 5.4.4 Plasma gasification technology

- 5.5 Dissolution & solvent-based recycling

- 5.5.1 Selective dissolution technologies

- 5.5.2 Solvent recovery & purification

Chapter 6 Market Estimates and Forecast, By Feedstock Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Polyolefin recycling (PE/PP)

- 6.2.1 High-density polyethylene (HDPE) recycling

- 6.2.2 Low-density polyethylene (LDPE) recycling

- 6.2.3 Polypropylene (pp) recycling

- 6.2.4 Mixed polyolefin streams

- 6.3 PET recycling

- 6.3.1 Bottle-to-bottle recycling

- 6.3.2 Fiber-to-fiber applications

- 6.3.3 Food-grade PET recycling

- 6.3.4 Colored PET processing

- 6.4 Mixed plastic waste recycling

- 6.4.1 Multi-layer packaging materials

- 6.4.2 Contaminated plastic streams

- 6.4.3 Electronic waste plastics

- 6.4.4 Automotive plastic components

- 6.5 Specialty polymer recycling

- 6.5.1 Engineering plastics recycling

- 6.5.2 Thermoset plastic processing

- 6.5.3 Composite material recycling

- 6.5.4 Bio-based polymer recycling

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Chemical feedstock production

- 7.3 Fuel production applications

- 7.4 New polymer production

- 7.5 Specialty product manufacturing

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 ExxonMobil Corporation

- 9.2 Eastman Chemical Company

- 9.3 Dow Inc.

- 9.4 SABIC (Saudi Basic Industries Corporation)

- 9.5 BASF SE

- 9.6 LyondellBasell Industries

- 9.7 PETRONAS Chemicals Group

- 9.8 Plastic Energy

- 9.9 Agilyx Corporation

- 9.10 Pyrowave Inc.

- 9.11 Recycling Technologies Ltd

- 9.12 Brightmark LLC

- 9.13 Quantafuel ASA

- 9.14 Carbios SA