|

시장보고서

상품코드

1885865

클린 라벨 단백질 가수분해물 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Clean Label Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

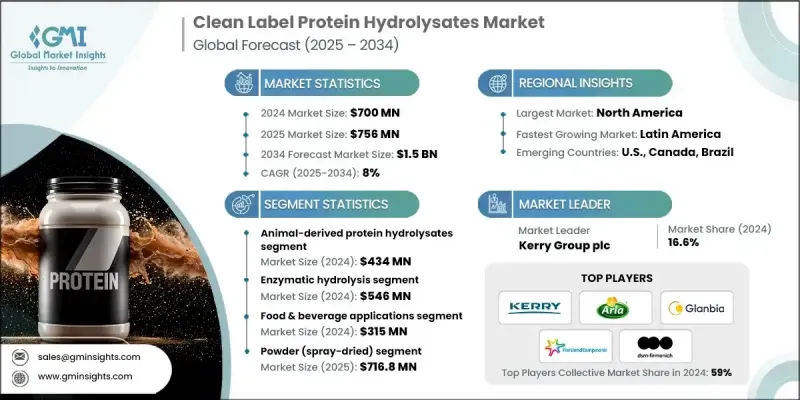

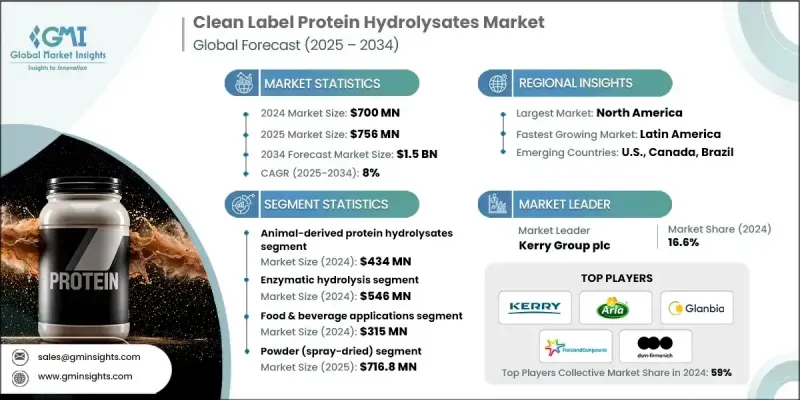

세계의 클린 라벨 단백질 가수분해물 시장은 2024년에 7억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 8%를 나타낼 것으로 예측되며 15억 달러로 성장할 전망입니다.

스포츠 영양 및 성능 중심 제품이 주류로 부상하면서 성장이 가속화되고 있으며, 소비자들은 근육 회복과 지속적인 에너지 공급을 돕는 빠른 흡수 및 소화 용이한 단백질을 우선시하고 있습니다. 이러한 변화로 인해 브랜드들은 아미노산 이용률과 소화 편의성을 개선하기 위해 효소 처리 단백질을 사용해 음료, 스낵, 분말 보충제를 재구성하고 있습니다. 구매자들이 최소한의 가공, 투명한 원료 조달, 인식 가능한 성분 목록을 선호함에 따라 클린 라벨에 대한 기대가 조달 관행을 재편하고 있습니다. 효소 생성 가수분해물은 제어된 가공, 높은 기능성, 검증된 순도로 이러한 선호도와 잘 부합합니다. 그 활용 범위는 영유아 영양, 웰빙 음료, 강화 식품으로 확대되고 있습니다. 가수분해 단백질의 탁월한 소화율과 생체 이용률 덕분에 임상 및 치료 영양 부문도 강력한 적용 영역으로 부상하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 가치 | 7억 달러 |

| 예측 가치 | 15억 달러 |

| CAGR | 8% |

효소 가수분해 부문은 2024년 5억 4,600만 달러를 창출했으며, 정밀한 펩타이드 구조를 가진 깨끗하고 고품질의 가수분해물을 생산할 수 있는 능력 덕분에 선도적인 점유율을 유지하고 있습니다. 이 방법은 소화율, 생체이용률 및 감각적 성능을 최적화하여 유아 영양, 의료용 조제분유 및 고성능 보충제에 적합합니다.

분말(분무 건조) 형태 부문은 2034년까지 연평균 복합 성장률(CAGR)은 7.8%로 성장할 전망입니다. 이 분말들은 긴 유통기한, 안정성, 글로벌 운송 용이성으로 시장을 주도합니다. 낮은 수분 함량과 높은 농도는 대규모 생산을 지원하여 스포츠 분말, 유아 영양제, 임상 영양 제품에 원활하게 통합될 수 있습니다.

북미의 클린 라벨 단백질 가수분해물 시장은 2024년 2억 2,400만 달러 규모로 32%의 점유율을 차지했습니다. 이 지역의 주도적 위상은 미국이 주도하며, 잘 발달된 스포츠 영양 산업, 광범위한 임상 영양 제조 역량, 유아용 조제분유 및 식이 보조제에 대한 강력한 수요가 이를 뒷받침합니다. 높은 1인당 단백질 섭취량과 견고한 유제품 및 생명공학 생태계는 지역 확장을 더욱 강화합니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 스포츠 영양 식품 및 기능성 식품 소비 증가

- 클린 라벨 제품에 대한 소비자 수요 증가

- 임상 및 의료 영양 응용 부문 성장

- 업계의 잠재적 위험 및 과제

- 효소 가수분해의 높은 생산 비용

- 복잡한 규제 준수 요건

- 시장 기회

- 고온 음료 응용을 위한 내열성 가수분해물

- 유기농 및 비유전자변형(Non-GMO) 인증 가수분해물

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품

- 장래 시장 동향

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 원료별(2021-2034년)

- 주요 동향

- 동물 유래 단백질 가수분해물

- 유제품 유래 가수분해물

- 유청 단백질 가수분해물

- 카제인 가수분해물

- 우유 단백질 가수분해물

- 육류 및 가금류 가수분해물

- 가수분해 가금 단백질

- 가수분해 소 및 돼지고기 단백질

- 해양 유래 가수분해물

- 기타 동물성 원료

- 콜라겐 및 젤라틴 가수분해물

- 계란 단백질 가수분해물

- 혈액 단백질 가수분해물

- 유제품 유래 가수분해물

- 식물 유래 단백질 가수분해물

- 콩 단백질 가수분해물

- 완두콩 단백질 가수분해물

- 쌀 단백질 가수분해물

- 밀 단백질 가수분해물

- 옥수수 단백질 가수분해물

- 기타 식물 유래 원료(소라마메, 햄프, 수수)

제6장 시장 추계 및 예측 : 가공 방법별(2021-2034년)

- 주요 동향

- 효소 가수분해

- 화학적 가수분해(산성 및 알칼리성)

- 미생물 발효

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 식품 및 음료 용도

- 스포츠 영양 및 성능 제품

- 유아 영양 및 저알레르기성 분유

- 임상 및 의료 영양

- 기능성 식품 및 음료

- 제빵 및 과자류

- 풍미 강화 및 풍미 향상

- 유제품

- 동물사료 및 영양

- 수산 양식용 사료

- 반려동물 식품

- 가축 사료

- 바이오 의약품 및 세포 배양

- 포유류 세포 배양 배지

- 백신 제조

- 단일클론항체 제조

- 화장품 및 퍼스널케어

제8장 시장 추계 및 예측 : 형태별(2021-2034년)

- 주요 동향

- 분말(분무 건조)

- 액체 및 농축 페이스트

- 반고형 형태

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Arla Foods Ingredients

- Kerry Group plc

- Glanbia Nutritionals

- FrieslandCampina Ingredients

- Archer Daniels Midland Company(ADM)

- Cargill, Incorporated

- DSM-Firmenich

- Norilia AS

- Roquette Freres

- Tate &Lyle PLC

- Lactalis Ingredients

- Peak Protein LLC

- Nuritas

- AB Enzymes GmbH

The Global Clean Label Protein Hydrolysates Market was valued at USD 700 million in 2024 and is estimated to grow at a CAGR of 8% to reach USD 1.5 billion by 2034.

Growth is accelerating as sports nutrition and performance-focused formulations gain mainstream traction, with consumers prioritizing fast-absorbing, easily digestible proteins that assist in muscle recovery and sustained energy. This shift is encouraging brands to reformulate beverages, snacks, and powdered supplements using enzyme-processed proteins to improve amino acid availability and digestive comfort. Clean-label expectations are reshaping procurement practices, as buyers prefer minimal processing, transparent sourcing, and recognizable ingredient lists. Enzyme-generated hydrolysates align well with these preferences due to their controlled processing, high functionality, and verified purity. Their expanding use extends into early-life nutrition, wellness beverages, and fortified foods. Clinical and therapeutic nutrition also represents a strong application area, supported by the exceptional digestibility and bioavailability of hydrolyzed proteins.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $700 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 8% |

The enzymatic hydrolysis segment generated USD 546 million in 2024 and maintains a leading share due to its ability to produce clean, high-quality hydrolysates with precise peptide structures. This method optimizes digestibility, bioavailability, and sensory performance, making it suitable for infant nutrition, medical formulas, and high-performance supplements.

The powder (spray-dried) formats segment will grow at a CAGR of 7.8% through 2034. These powders dominate because of their long shelf life, stability, and ease of global transport. Their low moisture content and high concentration support large-scale production, enabling seamless integration into sports powders, infant nutrition, and clinical nutrition products.

North America Clean Label Protein Hydrolysates Market accounted for USD 224 million in 2024, representing a 32% share. The region's leadership is driven by the United States, supported by a well-developed sports nutrition industry, extensive clinical nutrition manufacturing capacity, and strong demand for infant formula and dietary supplements. High per-capita protein intake and a robust dairy and biotechnology ecosystem further reinforce regional expansion.

Major companies active in the Global Clean Label Protein Hydrolysates Market include Arla Foods Ingredients, Kerry Group plc, Glanbia Nutritionals, FrieslandCampina Ingredients, Archer Daniels Midland Company (ADM), Cargill, Incorporated, DSM-Firmenich, Norilia AS, Roquette Freres, Tate & Lyle PLC, Lactalis Ingredients, Peak Protein LLC, Nuritas, and AB Enzymes GmbH. Companies in the Global Clean Label Protein Hydrolysates Market are enhancing their competitive position through targeted investments in advanced enzymatic processing, high-purity ingredient development, and clean-label certification. Many firms are expanding production capacity to support global distribution while focusing on improving flavor, solubility, and digestibility through precise hydrolysis controls. Strategic partnerships with sports nutrition, infant formula, and medical nutrition manufacturers are helping create long-term supply and innovation pipelines. Businesses are also prioritizing transparent sourcing, traceability systems, and reduced additive use to align with evolving consumer expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Protein Source

- 2.2.3 Processing Method

- 2.2.4 Application

- 2.2.5 Form

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing sports nutrition & functional food consumption

- 3.2.1.2 Rising consumer demand for clean label products

- 3.2.1.3 Growth in clinical & medical nutrition applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs of enzymatic hydrolysis

- 3.2.2.2 Complex regulatory compliance requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Heat-stable hydrolysates for hot beverage applications

- 3.2.3.2 Organic & non-GMO certified hydrolysates

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Protein Source, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Animal-derived protein hydrolysates

- 5.2.1 Dairy-based hydrolysates

- 5.2.1.1 Whey protein hydrolysates

- 5.2.1.2 Casein hydrolysates

- 5.2.1.3 Milk protein hydrolysates

- 5.2.2 Meat & poultry hydrolysates

- 5.2.2.1 Hydrolyzed poultry protein

- 5.2.2.2 Hydrolyzed beef & pork proteins

- 5.2.3 Marine-derived hydrolysates

- 5.2.4 Other animal sources

- 5.2.4.1 Collagen & gelatin hydrolysates

- 5.2.4.2 Egg protein hydrolysates

- 5.2.4.3 Blood protein hydrolysates

- 5.2.1 Dairy-based hydrolysates

- 5.3 Plant-Derived Protein Hydrolysates

- 5.3.1 Soy protein hydrolysates

- 5.3.2 Pea protein hydrolysates

- 5.3.3 Rice protein hydrolysates

- 5.3.4 Wheat protein hydrolysates

- 5.3.5 Corn protein hydrolysates

- 5.3.6 Other plant sources (fava bean, hemp, sorghum)

Chapter 6 Market Estimates and Forecast, By Processing Method, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Enzymatic hydrolysis

- 6.3 Chemical hydrolysis (acid & alkaline)

- 6.4 Microbial fermentation

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage applications

- 7.2.1 Sports nutrition & performance products

- 7.2.2 Infant nutrition & hypoallergenic formulas

- 7.2.3 Clinical & medical nutrition

- 7.2.4 Functional foods & beverages

- 7.2.5 Bakery & confectionery

- 7.2.6 Savory applications & flavor enhancement

- 7.2.7 Dairy products

- 7.3 Animal feed & nutrition

- 7.3.1 Aquaculture feed

- 7.3.2 Pet food

- 7.3.3 Livestock feed

- 7.4 Biopharmaceutical & cell culture

- 7.4.1 Mammalian cell culture media

- 7.4.2 Vaccine production

- 7.4.3 Monoclonal antibody manufacturing

- 7.5 Cosmetics & personal care

Chapter 8 Market Estimates and Forecast, By Form, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Powder (spray-dried)

- 8.3 Liquid & concentrated paste

- 8.4 Semi-solid forms

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arla Foods Ingredients

- 10.2 Kerry Group plc

- 10.3 Glanbia Nutritionals

- 10.4 FrieslandCampina Ingredients

- 10.5 Archer Daniels Midland Company (ADM)

- 10.6 Cargill, Incorporated

- 10.7 DSM-Firmenich

- 10.8 Norilia AS

- 10.9 Roquette Freres

- 10.10 Tate & Lyle PLC

- 10.11 Lactalis Ingredients

- 10.12 Peak Protein LLC

- 10.13 Nuritas

- 10.14 AB Enzymes GmbH