|

시장보고서

상품코드

1885871

양방향 EV 충전 시스템 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Bidirectional EV Charging (V2G/V2H) System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

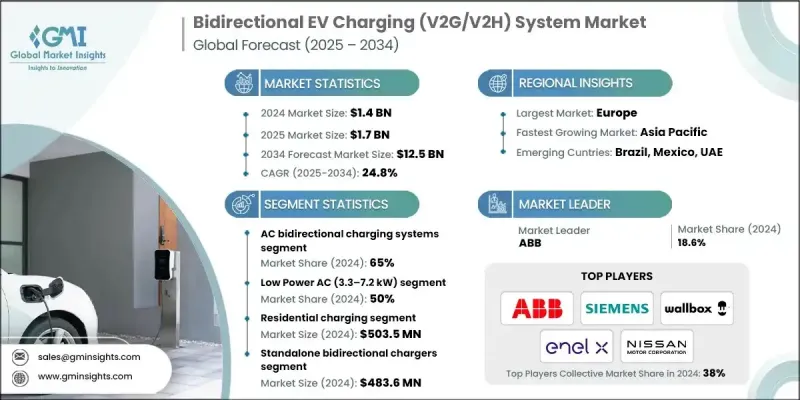

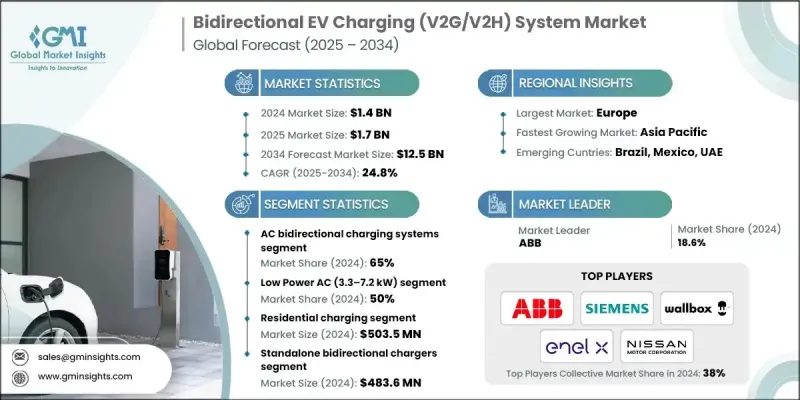

세계의 양방향 EV 충전(V2G/V2H) 시스템 시장은 2024년에 14억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 24.8%를 나타낼 것으로 예측되며 125억 달러로 성장할 전망입니다.

시장 성장은 전기차의 급속한 보급, 상업용 및 개인용 전기차 함대의 확대, 스마트 에너지 관리 솔루션에 대한 수요 증가에 힘입고 있습니다. 차량-전력망(V2G) 및 차량-가정(V2H) 기술이 발전함에 따라 이해관계자들은 운영 효율성 향상, 전력망 안정성 강화, 최적화된 부하 분배에 주력하고 있습니다. 시장은 데이터 기반의 자동화되고 연결된 V2G/V2H 네트워크로 전환되며, 기존 에너지 관리 방식을 혁신하고 있습니다. IoT 기반 양방향 충전기, AI 기반 부하 균형 알고리즘, 클라우드 기반 에너지 플랫폼의 활용 증가는 운영에 혁신을 가져오고 있습니다. 이를 통해 예측적 에너지 방전, 유틸리티와 차량 운영자 간의 원활한 협업, 실시간 모니터링이 가능해져 효율성 향상, 피크 부하 감소, 운영 비용 절감이 이루어지고 있습니다. 이러한 혁신은 주거용, 상업용, 차량용 전반에 걸쳐 확장 가능하고 비용 효율적이며 탄력적인 양방향 충전 생태계를 지원합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 가치 | 14억 달러 |

| 예측 가치 | 125억 달러 |

| CAGR | 24.8% |

AC 양방향 충전 시스템 부문은 2024년 65%의 점유율을 기록했으며, 2025년부터 2034년까지 연평균 25.2%의 성장률을 보일 것으로 전망됩니다. AC 양방향 시스템은 효율적인 V2G/V2H 에너지 흐름에 필수적이며, 온보드 AC 충전기, 스마트 부하 제어기 및 통신 인터페이스를 활용하여 EV에서 가정이나 그리드로의 에너지 방전을 용이하게 합니다.

저전력 AC 부문(3.3-7.2kW)은 2024년에 50%의 점유율을 차지했으며, 2034년까지 연평균 24.5%의 성장률을 보일 것으로 예상됩니다. 이 부문은 주로 주거용 및 소규모 상업용 애플리케이션에 의해 주도되며, 대부분의 전기차와 호환되는 비용 효율적이고 설치가 용이한 솔루션을 제공하며, IoT 모니터링 및 AI 기반 에너지 스케줄링으로 강화됩니다.

독일의 양방향 EV 충전(V2G/V2H) 시스템 시장은 40%의 점유율을 차지했으며, 2024년에는 1억 9,480만 달러 시장 규모를 창출했습니다. 이 나라의 주도적 지위는 강력한 자동차 제조 역량, 규제 인센티브, 연결형 V2G 지원 인프라의 광범위한 도입에 힘입었습니다. 독일은 진화하는 에너지 규정을 준수하면서 전력망 안정성과 운영 효율성을 보장하기 위해 AI 기반 부하 최적화, IoT 지원 양방향 충전기, 예측 에너지 스케줄링, 클라우드 통합 에너지 관리 플랫폼을 점차 도입하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전기차의 급속한 보급 및 차량 군 확대

- 스마트 그리드와 에너지 관리 요구

- 기술 발전

- 정부 정책 및 인센티브

- 업계의 잠재적 위험 및 과제

- 높은 인프라 비용과 도입 비용

- 규제 및 표준화 격차

- 시장 기회

- 재생에너지 및 가정용 에너지 시스템과의 통합

- 차량 및 상업용도

- 규제 인센티브 및 지원 정책

- 스마트 시티 및 차량 전기화 프로젝트

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미의 규제 환경

- 유럽연합의 지령과 의무

- 아시아태평양의 정책 틀

- 상호연결기준과 유틸리티자의 요건

- 차량의 안전성 및 인증 요건

- 건축 기준법 및 전기 설비 기준의 갱신

- 보험 및 배상 책임에 관한 규제 프레임워크

- 데이터 프라이버시 및 소비자 보호 규제

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- AC 양방향 충전 기술의 진화

- DC 양방향 충전 기술의 진전

- 온보드 및 오프보드 아키텍처의 트레이드오프

- 파워 일렉트로닉스 및 인버터 기술의 동향

- 배터리 관리 시스템의 통합

- 스마트 인버터의 기능과 계통 지원 능력

- 무선/유도식 양방향 충전 기술에 관한 조사

- 기술 요소별 기술 성숙도 평가

- 차세대 기술 파이프라인

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출과 수입

- 비용 내역 분석

- 특허 분석

- 지속가능성과 환경적 측면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산의 에너지 효율

- 환경에 배려한 대처

- 최상의 시나리오

- 파일럿 프로그램과 도입 사례 연구

- 유틸리티용 버전 2 파일럿 프로그램 개요

- PG&E BMW 충전 포워드 프로그램

- 콘 에디슨의 스마트 과금

- OPG V2G 파일럿

- 영국의 V2G 시험 운용

- 일본의 V2H 도입 프로그램

- 소비자 행동과 도입 상황 분석

- 지역별 소비자 인지도 레벨

- 구매결정요인과 우선순위

- 지불 의사 분석

- 유틸리티 프로그램에의 참가율

- 해약율과 고객유지율 분석

- 고객 만족도 지표

- 거시경제 요인과 시장에 미치는 영향

- 에너지 가격 변동의 영향

- 전기요금 체계와 시간대별 요금제도

- 도매 에너지 시장 가격의 동향

- 금리환경과 자금조달 비용

- 설비 비용에 대한 인플레이션의 영향

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 충전 방식별(2021-2034년)

- 주요 동향

- AC 양방향 충전 시스템

- DC 양방향 충전 시스템

제6장 시장 추계 및 예측 : 발전 용량별(2021-2034년)

- 주요 동향

- 저전력 AC(3.3-7.2 kW)

- 중전력 AC(11-22kW)

- DC 급속 충전(50-150kW)

- 고전력 DC(150kW 이상)

제7장 시장 추계 및 예측 : 충전 장소별(2021-2034년)

- 주요 동향

- 주택용 충전

- 직장용 충전

- 차량 기지 충전

- 공공 충전

제8장 시장 추계 및 예측 : 통합 레벨별(2021-2034년)

- 주요 동향

- 독립형 양방향 충전기

- 태양광 발전과의 통합

- 고정형 축전지와의 통합

- 완전 통합형 가정용 에너지 시스템

- 마이크로그리드 통합 시스템

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 주택 사용자

- 상용차 및 차량 운영사

- 전력회사 및 송배전 사업자

- 산업시설

- 공공 부문 및 긴급 서비스

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제11장 기업 프로파일

- 세계적 기업

- ABB

- ChargePoint

- Eaton

- Enel X

- Nissan Motor

- Nuvve

- Schneider Electric

- Shell Recharge Solutions

- Siemens

- Wallbox Chargers

- 지역 기업

- Blink charging

- Engie EV solutions

- Evbox

- Pod point

- Star charge

- Tesla energy

- TGOOD

- The mobility house

- Tritium

- Virta

- 신흥 기업

- Freewire technologies

- Greenlots

- Incharge energy

- Ohme

- Ovo energy V2G solutions

The Global Bidirectional EV Charging (V2G/V2H) System Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 24.8% to reach USD 12.5 billion by 2034.

Market growth is fueled by the rapid adoption of electric vehicles, the expansion of commercial and private EV fleets, and rising demand for smart energy management solutions. As vehicle-to-grid and vehicle-to-home technologies advance, stakeholders are focusing on enhancing operational efficiency, grid stability, and optimized load distribution. The market is shifting toward data-driven, automated, and connected V2G/V2H networks, transforming conventional energy management approaches. Increasing use of IoT-enabled bidirectional chargers, AI-powered load balancing algorithms, and cloud-based energy platforms is revolutionizing operations, enabling predictive energy discharge, seamless coordination between utilities and fleet operators, and real-time monitoring to improve efficiency, reduce peak load, and lower operational costs. These innovations support scalable, cost-effective, and resilient bidirectional charging ecosystems across residential, commercial, and fleet applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $12.5 Billion |

| CAGR | 24.8% |

The AC bidirectional charging systems segment accounted for a 65% share in 2024 and is projected to grow at a CAGR of 25.2% between 2025 and 2034. AC bidirectional systems are integral for efficient V2G/V2H energy flow, leveraging onboard AC chargers, smart load controllers, and communication interfaces to facilitate energy discharge from EVs to homes or grids.

The low-power AC segment (3.3-7.2 kW) held a 50% share in 2024 and is expected to grow at a CAGR of 24.5% through 2034. This segment is primarily driven by residential and small commercial applications, offering cost-effective, easily installable solutions compatible with most EVs, enhanced by IoT monitoring and AI-enabled energy scheduling.

Germany Bidirectional EV Charging (V2G/V2H) System Market held a 40% share, generating USD 194.8 million in 2024. The country's leadership is supported by strong automotive manufacturing, regulatory incentives, and widespread adoption of connected, V2G-enabled infrastructure. Germany is increasingly implementing AI-based load optimization, IoT-enabled bidirectional chargers, predictive energy scheduling, and cloud-integrated energy management platforms to ensure grid reliability and operational efficiency while adhering to evolving energy regulations.

Key players driving growth in the Bidirectional EV Charging (V2G/V2H) System Market include Nuvve, Wallbox Chargers, Eaton, ABB, Siemens, Enel X, ChargePoint, The Mobility House, Schneider Electric, and Nissan Motor. Companies are strengthening their presence through strategic initiatives such as expanding regional charging networks, forming partnerships with utilities and fleet operators, and investing in AI and IoT-based bidirectional technologies. Product innovations include cost-efficient, low-power AC solutions and scalable commercial V2G systems. Firms also focus on integrating cloud platforms, predictive energy scheduling, and smart load balancing to improve performance and compliance. Marketing efforts target residential, commercial, and fleet customers to increase adoption, while mergers, acquisitions, and long-term service agreements enhance distribution, brand recognition, and market foothold globally.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Charging

- 2.2.3 Power capacity

- 2.2.4 Charging location

- 2.2.5 Integration level

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid EV adoption & fleet expansion

- 3.2.1.2 Smart grid & energy management needs

- 3.2.1.3 Technological advancements

- 3.2.1.4 Government policies & incentives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure & implementation costs

- 3.2.2.2 Regulatory & standardization gaps

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with renewable energy & home energy systems

- 3.2.3.2 Fleet & commercial applications

- 3.2.3.3 Regulatory incentives and supportive policies

- 3.2.3.4 Smart city and fleet electrification projects

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America regulatory environment

- 3.4.2 European union directives & mandates

- 3.4.3 Asia pacific policy frameworks

- 3.4.4 Interconnection standards & utility requirements

- 3.4.5 Vehicle safety & certification requirements

- 3.4.6 Building code & electrical code updates

- 3.4.7 Insurance & liability regulatory framework

- 3.4.8 Data privacy & consumer protection regulations

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 AC bidirectional charging technology evolution

- 3.7.2 DC bidirectional charging advancements

- 3.7.3 Onboard vs offboard architecture trade-offs

- 3.7.4 Power electronics & inverted technology trends

- 3.7.5 Battery management system integration

- 3.7.6 Smart inverter functions & grid support capabilities

- 3.7.7 Wireless/inductive bidirectional charging research

- 3.7.8 Technology readiness assessment by component

- 3.7.9 Next-generation technology pipeline

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Best case scenarios

- 3.14 Pilot programs & deployment case studies

- 3.14.1. Utility v2 g pilot programs overview

- 3.14.2 Pg&e BMW chargeforward program

- 3.14.3 Con Edison smart charge

- 3.14.4. Opg v2 g pilot

- 3.14.5. Uk v2 g trials

- 3.14.6. Japanese v2 h deployment programs

- 3.15 Consumer Behavior & Adoption Analysis

- 3.15.1 Consumer awareness levels by region

- 3.15.2 Purchase decision factors & priorities

- 3.15.3 Willingness to pay analysis

- 3.15.4 Participation rates in utility programs

- 3.15.5 Churn rates & retention analysis

- 3.15.6 Customer satisfaction metrics

- 3.16 Macroeconomic Factors & Market Impact

- 3.16.1 Energy price volatility impact

- 3.16.2 Electricity rate structures & time-of-use pricing

- 3.16.3 Wholesale energy market price trends

- 3.16.4 Interest rate environment & financing costs

- 3.16.5 Inflation impact on equipment costs

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Charging, 2021 - 2034 ($ Bn, Units)

- 5.1 Key trends

- 5.2 AC bidirectional charging systems

- 5.3 DC bidirectional charging systems

Chapter 6 Market Estimates & Forecast, By Power Capacity, 2021 - 2034 ($ Bn, Units)

- 6.1 Key trends

- 6.2 Low power AC (3.3-7.2 kW)

- 6.3 Medium power AC (11-22 kW)

- 6.4 DC fast charging (50-150 kW)

- 6.5 High power DC (150+ kW)

Chapter 7 Market Estimates & Forecast, By Charging Location, 2021 - 2034 ($ Bn, Units)

- 7.1 Key trends

- 7.2 Residential charging

- 7.3 Workplace charging

- 7.4 Fleet depot charging

- 7.5 Public charging

Chapter 8 Market Estimates & Forecast, By Integration Level, 2021 - 2034 ($ Bn, Units)

- 8.1 Key trends

- 8.2 Standalone bidirectional chargers

- 8.3 Integrated with solar PV

- 8.4 Integrated with stationary battery storage

- 8.5 Fully integrated home energy systems

- 8.6 Microgrid-integrated systems

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($ Bn, Units)

- 9.1 Key trends

- 9.2 Residential users

- 9.3 Commercial & fleet operators

- 9.4 Electric utilities & grid operators

- 9.5 Industrial facilities

- 9.6 Public sector & emergency services

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 ABB

- 11.1.2 ChargePoint

- 11.1.3 Eaton

- 11.1.4 Enel X

- 11.1.5 Nissan Motor

- 11.1.6 Nuvve

- 11.1.7 Schneider Electric

- 11.1.8 Shell Recharge Solutions

- 11.1.9 Siemens

- 11.1.10 Wallbox Chargers

- 11.2 Regional Player

- 11.2.1 Blink charging

- 11.2.2 Engie EV solutions

- 11.2.3 Evbox

- 11.2.4 Pod point

- 11.2.5 Star charge

- 11.2.6 Tesla energy

- 11.2.7 TGOOD

- 11.2.8 The mobility house

- 11.2.9 Tritium

- 11.2.10 Virta

- 11.3 Emerging Players

- 11.3.1 Freewire technologies

- 11.3.2 Greenlots

- 11.3.3 Incharge energy

- 11.3.4 Ohme

- 11.3.5. Ovo energy V2 G solutions