|

시장보고서

상품코드

1885874

균사체 기반 단백질 원료 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Mycelium-Based Protein Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

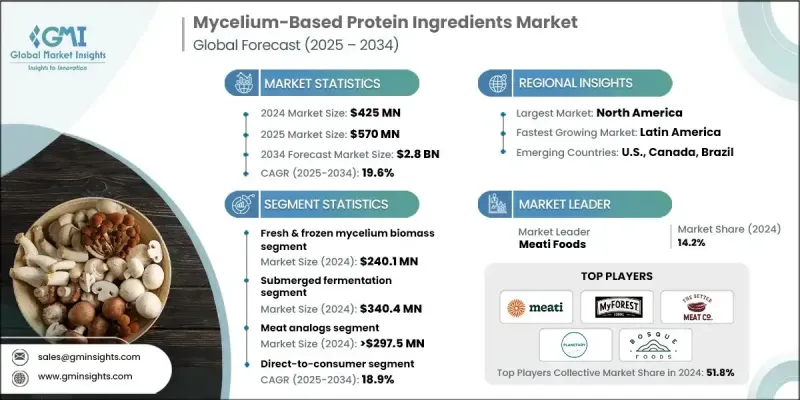

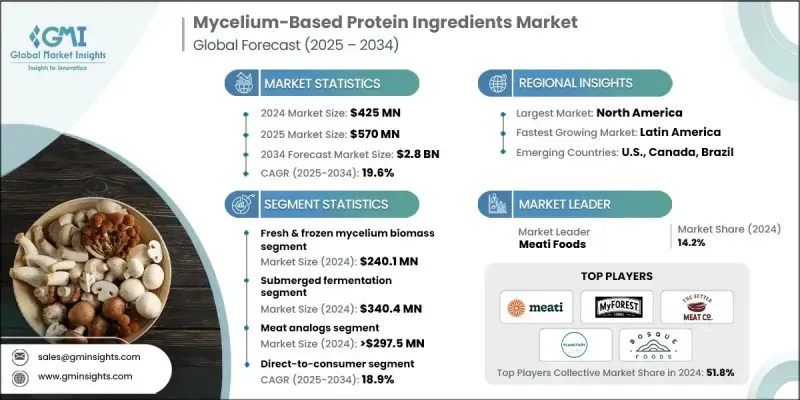

세계의 균사체 기반 단백질 원료 시장은 2024년에 4억 2,500만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 19.6%를 나타낼 것으로 예측되며 28억 달러로 성장할 전망입니다.

영양가가 높고 지속 가능한 대체 식품을 찾는 소비자가 증가함에 따라 환경 친화적인 단백질 원료에 대한 소비자 수요가 증가하면서 시장 확장이 지속되고 있습니다. 이러한 관심 증대는 소매업체와 식품 서비스 기업들이 더 다양한 균류 유래 제품을 출시하도록 장려하여 대체 단백질 산업 전반에 걸쳐 제품 개발 속도를 높이고 제조 역량을 확대하고 있습니다. 발효 과학 및 생물공정 공학의 발전은 더 큰 제어력, 높은 수율, 일관된 품질을 제공하도록 설계된 산업용 생물반응기의 지원을 받아 생산을 대규모 역량으로 이끌고 있습니다. 파일럿 운영에서 상업 규모 시설로의 전환은 자금 조달 활동 증가와 신규 생산 시설에 대한 상당한 투자로 강화되어 식품 제조업체의 균사체 원료 확보를 촉진하고 있습니다. 민간 및 공공 부문의 재정 지원은 공장 건설을 가속화하고 공급망 전반에 걸친 급속한 확장을 주도하고 있습니다. 이러한 자본 유입 급증은 상용화 기간을 단축하고 규모의 경제를 통한 비용 절감을 실현하며, 생산자와 구매자가 기록한 바와 같이 전체 시장 용량을 확대하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 가치 | 4억 2,500만 달러 |

| 예측 가치 | 28억 달러 |

| CAGR | 19.6% |

신선 및 냉동 균사체 바이오매스 부문은 전체 식품 적용 및 클린 라벨 선호도와 부합하여 2024년 2억 4,010만 달러에 달했습니다. 자연스러운 질감과 풍부한 섬유질 프로필 덕분에 생산자들은 과도한 가공 없이 통째로 썰어 만든 대체 식품, 패티 또는 즉석 조리 식품을 만들 수 있습니다. 이 형식은 더 짧은 성분 목록, 생산 단계 감소, 확장 가능한 생산량, 소매 및 외식 채널로의 신속한 진입을 원하는 브랜드에 이상적입니다.

침지 발효 부문은 2024년 3억 4,040만 달러의 가치를 보였으며, 효율성과 확장성 덕분에 주요 생산 방식으로 계속 사용되고 있습니다. 이 기술은 온도, 산소, 영양분 유동, pH를 정밀하게 모니터링할 수 있는 대형 산업용 바이오리액터를 활용하여 지속적인 생물질 성장과 예측 가능한 생산량을 지원합니다. 공정 제어 개선으로 생산성이 향상되고, 비용 효율성 덕분에 대형 식품 제조업체 및 패스트푸드 업체에 공급하는 기업에 적합합니다.

북미의 균사체 기반 단백질 원료 시장은 2024년에 36.4%의 점유율을 차지해 미국의 활발한 움직임이 주도했습니다. 해당 지역은 기존 발효 시설, 경험 많은 인프라, 균류 단백질 개발 기업에 대한 초기 투자로 혜택을 받고 있습니다. 상당한 벤처 자금 지원은 생산 능력 확대를 가속화하고 소매 및 외식 서비스 부문 모두에서 신속한 상용화를 뒷받침합니다. 소매업체들이 제품 포트폴리오를 다양화하려는 가운데, 고단백, 클린 라벨, 환경 친화적 옵션에 대한 소비자 관심이 높아지면서 균사체 기반 제품 수요가 강화되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 지속 가능한 단백질 원천에 대한 소비자 수요 증가

- 동물 농업 대비 환경적 이점

- 발효 기술 발전

- 대체 단백질에 대한 투자 증가

- 업계의 잠재적 위험 및 과제

- 식물성 단백질 대비 높은 생산 비용

- 제한된 소비자 인식 및 수용도

- 시장 기회

- 임상 영양 응용 부문 개발

- 식품 폐기물 가치화와의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품

- 장래 시장 동향

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 제품 형태별(2021-2034년)

- 주요 동향

- 신선 및 냉동 균사체 바이오매스

- 건조 균사체

- 균사체 분말 및 분말상품

- 단백질 분리물 및 농축물

- 홀컷 제품

제6장 시장 추계 및 예측 : 제조기술별(2021-2034년)

- 주요 동향

- 침지 발효

- 고형 발효

- 연속 호기성 발효

- 배치 및 피드 배치 발효

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 고기 대체품

- 버거 및 갈은 고기

- 통조림 스테이크 및 커틀릿

- 베이컨 및 소시지

- 너겟 및 가공육 제품

- 유제품 대체품

- 우유 및 크림 대체품

- 요구르트 및 발효 제품

- 치즈 대체품

- 아이스크림 및 냉동 디저트

- 구운 과자

- 음료

- 스낵 및 가공식품

- 스포츠 영양 및 보충제

- 임상영양

- 동물사료

제8장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- B2B 원료 공급업체

- 소비자용 직접 판매

- 소매(모던 트레이드)

- 슈퍼마켓 및 대형 슈퍼마켓

- 편의점

- 전문건강식품점

- 온라인 및 전자상거래

- 전통 시장 및 노점상

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Bosque Foods

- Maia Farms

- Planetary

- Meati Foods

- Cargill

- My Forest Foods

- Optimized Foods

- Esencia Foods

- Better Meat Co

The Global Mycelium-Based Protein Ingredients Market was valued at USD 425 million in 2024 and is estimated to grow at a CAGR of 19.6% to reach USD 2.8 billion by 2034.

Rising consumer demand for environmentally conscious protein sources continues to help in this expansion, as more individuals seek nutrient-dense, sustainable alternatives. This growing interest has encouraged retailers and foodservice companies to introduce a wider range of fungi-derived offerings, prompting faster product development and broader manufacturing capabilities across the alternative-protein landscape. Advancements in fermentation science and bioprocess engineering are pushing production toward large-scale capabilities, supported by industrial bioreactors designed to deliver greater control, higher yields, and consistent quality. The shift from pilot operations to commercial-scale facilities is reinforced by increased funding activities and significant investments in new production sites, boosting the availability of mycelium ingredients for food manufacturers. Financial support from both private and public sectors is accelerating the construction of factories and driving rapid expansion across the supply chain. This surge in capital flow shortens commercialization timelines, reduces costs through scale efficiencies, and expands overall market capacity as documented by producers and purchasers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $425 Million |

| Forecast Value | $2.8 Billion |

| CAGR | 19.6% |

The fresh and frozen mycelium biomass segment reached USD 240.1 million in 2024, driven by alignment with whole-food applications and clean-label preferences. Its natural texture and fiber-rich profile allow producers to create whole-cut alternatives, patties, or ready-made meals without heavy processing. This format is ideal for brands looking for shorter ingredient lists, reduced production steps, scalable volume, and quicker entry into retail and foodservice channels.

The submerged fermentation segment was valued at USD 340.4 million in 2024 and continues to serve as the primary production method due to its efficiency and scalability. This technique leverages large industrial bioreactors that allow precise monitoring of temperature, oxygen, nutrient flow, and pH, supporting continuous biomass growth and more predictable output. Improved process control results in higher productivity, while cost efficiencies make it suitable for companies supplying large food manufacturers and quick-service businesses.

North America Mycelium-Based Protein Ingredients Market held a 36.4% share in 2024, led by strong activity in the United States. The region benefits from established fermentation facilities, experienced infrastructure, and early investments in companies developing fungal proteins. Substantial venture funding accelerates capacity growth and supports rapid commercialization in both retail and foodservice sectors. Rising consumer interest in high-protein, clean-label, and environmentally friendly options strengthens the demand for mycelium-based products as retailers seek to diversify their product offerings.

Major companies active in the Mycelium-Based Protein Ingredients Market include Maia Farms, My Forest Foods, Meati Foods, Bosque Foods, Optimized Foods, Cargill, Planetary, Better Meat Co., and Esencia Foods. Companies in the Mycelium-Based Protein Ingredients Market use multiple strategies to enhance their competitive position. Many focus on expanding fermentation capacity and optimizing bioprocesses to increase output while lowering production costs. Investments in R&D help firms improve texture, flavor, and nutritional profiles to meet the expectations of food manufacturers and consumers. Strategic partnerships with retailers, ingredient suppliers, and foodservice operators expand distribution networks and support quicker market integration. Brands also emphasize clean-label positioning and sustainability messaging to strengthen consumer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Form

- 2.2.3 Production Technology

- 2.2.4 Application

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for sustainable protein sources

- 3.2.1.2 Environmental benefits over animal agriculture

- 3.2.1.3 Technological advancements in fermentation

- 3.2.1.4 Increasing investment in alternative proteins

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs compared to plant proteins

- 3.2.2.2 Limited consumer awareness & acceptance

- 3.2.3 Market opportunities

- 3.2.3.1 Development of clinical nutrition applications

- 3.2.3.2 Integration with food waste valorization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Form, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Fresh & frozen mycelium biomass

- 5.3 Dried mycelium

- 5.4 Mycelium powder & flour

- 5.5 Protein isolates & concentrates

- 5.6 Whole-cut formats

Chapter 6 Market Estimates and Forecast, By Production Technology, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Submerged fermentation

- 6.3 Solid-state fermentation

- 6.4 Continuous aerobic fermentation

- 6.5 Batch & fed-batch fermentation

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Meat analogs

- 7.2.1 Burgers & ground meat

- 7.2.2 Whole-cut steaks & cutlets

- 7.2.3 Bacon & sausages

- 7.2.4 Nuggets & processed meats

- 7.3 Dairy analogs

- 7.3.1 Milk & cream alternatives

- 7.3.2 Yogurt & fermented products

- 7.3.3 Cheese alternatives

- 7.3.4 Ice cream & frozen desserts

- 7.4 Baked goods

- 7.5 Beverages

- 7.6 Snacks & processed foods

- 7.7 Sports nutrition & supplements

- 7.8 Clinical nutrition

- 7.9 Animal feed

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD million) (Kilo Tons)

- 8.1 Key trends

- 8.2 B2B ingredient suppliers

- 8.3 Direct-to-consumer

- 8.4 Retail (modern trade)

- 8.4.1 Supermarkets & hypermarkets

- 8.4.2 Convenience stores

- 8.4.3 Specialty health food stores

- 8.5 Online & e-commerce

- 8.6 Traditional markets & street vendors

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Bosque Foods

- 10.2 Maia Farms

- 10.3 Planetary

- 10.4 Meati Foods

- 10.5 Cargill

- 10.6 My Forest Foods

- 10.7 Optimized Foods

- 10.8 Esencia Foods

- 10.9 Better Meat Co