|

시장보고서

상품코드

1885917

내구성 의료장비 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Durable Medical Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

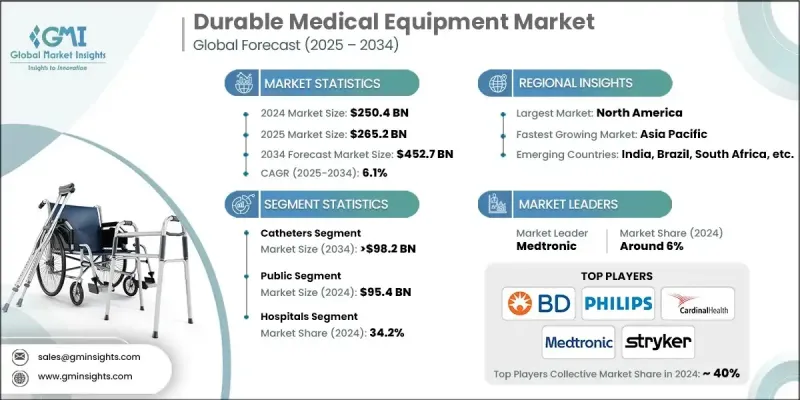

세계의 내구성 의료장비 시장은 2024년에 2,504억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 6.1%를 나타낼 것으로 예측되며 4,527억 달러로 성장할 전망입니다.

시장 성장은 전 세계적으로 만성 질환 유병률 증가, 의료 기술 발전, 가정 의료 서비스 선호도 증가, 그리고 지원적인 보험 정책에 의해 주도되고 있습니다. 재활 치료, 환자 중심 치료, 인체공학적 사용자 친화적 장비에 대한 강조가 증가하면서 수요가 더욱 촉진되고 있습니다. 고령화 인구 역시 특수 장비 수요 증가에 기여하고 있습니다. 기업들은 제품 혁신을 적극적으로 추진하고, 신소재 통합을 도모하며, 지역적 파트너십을 구축해 시장 확대를 도모하고 있습니다. 기술 통합은 핵심 시장 촉진요인으로 부상 중이며, 현재 장비들은 무선 모니터링, 인공지능 기반 진단, 모바일 앱 연동 기능을 제공해 실시간 데이터 공유와 맞춤형 치료를 가능하게 합니다. 의료 서비스가 디지털 및 가치 기반 모델로 전환됨에 따라, 기술이 강화된 DME는 효율적이고 환자 중심의 치료에 점점 더 중요해지고 있으며, 차별화와 시장 성장의 새로운 기회를 열어주고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 2,504억 달러 |

| 예측 금액 | 4,527억 달러 |

| CAGR | 6.1% |

카테터 부문은 수술 절차 및 비뇨기과 관련 치료 증가에 힘입어 2024년 22.3%의 점유율을 차지했습니다. 카테터는 체액 배출, 약물 투여, 순환계 접근 제공에 필수적인 역할을 수행합니다. 특히 요폐, 심혈관 질환 환자 또는 투석 치료를 받는 환자를 중심으로 병원, 장기 요양 시설, 가정 간호 환경에서 광범위하게 사용됩니다.

공공 보험자 부문은 2024년 954억 달러로 평가되었습니다. 공공 보험자는 정부 지원 건강 프로그램 및 보험 가입자에게 보장을 제공하는 보험 플랜이 포함됩니다. 이들은 대량 구매 가격 협상을 진행하며 비용 효율적인 필수 의료장비(DME)를 중시합니다. 공공 지불자는 특히 저소득층 및 농촌 지역에서 접근성 확대에 핵심적이며, 보상 정책이 제품 가용성과 시장 수요에 직접적인 영향을 미칩니다.

북미의 내구성 의료장비 시장은 첨단 의료 인프라, 높은 의료 지출, 노인 인구가 많아 2024년에 큰 점유율을 차지했습니다. 당뇨병, 심혈관 질환, 호흡기 질환 등의 만성 질환의 유병률이 높아져 장기간의 장비 사용을 촉진하고 있습니다. 가정 의료 및 디지털 건강 기술의 보급 확대로 휴대 가능하고 연결 기능을 갖춘 장치에 대한 수요가 가속화되고 있습니다. 메디케어와 메디케이드를 포함한 정부의 이니셔티브는 특히 노인과 장애인을 대상으로 필수 DME 제품에 대한 액세스를 더욱 지원합니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 재택치료에 대한 환자 선호 고조

- 세계의 만성 질환 증가 경향

- 고령화 인구 증가

- 제품의 기술적 진보

- 업계의 잠재적 위험 및 과제

- 높은 기기 비용 및 경제성 문제

- 소아용 제품에 대한 수요 증가

- 기회

- AI/머신러닝의 통합과 예측 분석

- 신흥 시장의 사업 확대와 인프라 정비

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 투자환경

- 보험급여 시나리오

- 의료 제공 모델의 변화

- 맞춤형 의료 및 정밀의료의 응용

- 소프트웨어로서의 의료장비(SaMD) 통합 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

- 장래 시장 동향

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 개인용 이동 보조구

- 휠체어와 스쿠터

- 목발 및 지팡이

- 보행기

- 기타 개인용 이동 보조구

- 모니터링 및 치료장비

- 산소 공급 장비

- 혈당 측정기

- 바이탈 사인 모니터

- 주입 펌프

- 지속적기도양압(CPAP)장치

- 분무기

- 기타 모니터링 및 치료장비

- 욕실안전장치

- 의료용 가구

- 실금용 패드

- 유축기

- 카테터

- 소모품 및 부속품

- 기타 제품

제6장 시장 추계 및 예측 : 지불 주체별(2021-2034년)

- 주요 동향

- 공공

- 민간

- 자기 부담

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 재택치료

- 외래수술센터(ASC)

- 기타 용도

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- B Braun

- Baxter

- BD

- Cardinal Health

- CAREX

- Coloplast

- COMPASS HEALTH

- convaTec

- drive DeVilbiss Healthcare

- Getinge

- graham-field

- INTCO MEDICAL

- INVACARE

- Koninklijke Philips

- MEDLINE

- Medtronic

- ResMed

- Stryker

- SUNRISE MEDICAL

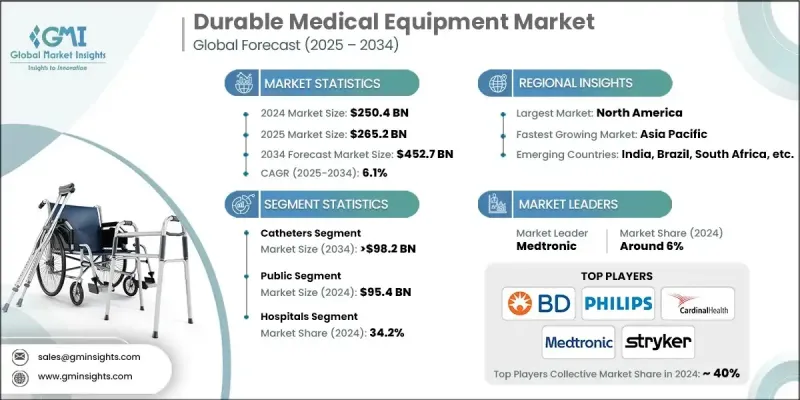

The Global Durable Medical Equipment Market was valued at USD 250.4 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 452.7 billion by 2034.

Market growth is driven by the rising prevalence of chronic illnesses worldwide, advancements in medical technology, the growing preference for home healthcare, and supportive reimbursement policies. Increasing emphasis on rehabilitation, patient-centered care, and ergonomic, user-friendly equipment is further fueling demand. The aging population also contributes to the need for specialized devices. Companies are actively innovating products, integrating novel materials, and forming regional partnerships to expand geographically. Technological integration is becoming a core market driver, with devices now offering wireless monitoring, AI-powered diagnostics, and mobile app connectivity to enable real-time data sharing and personalized care. As healthcare shifts toward digital and value-based models, technology-enhanced DME is increasingly critical for efficient, patient-focused treatment, opening new opportunities for differentiation and market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $250.4 Billion |

| Forecast Value | $452.7 Billion |

| CAGR | 6.1% |

The catheters segment held a 22.3% share in 2024, driven by the growing number of surgical procedures and urology-related treatments. Catheters serve essential roles in draining fluids, administering medication, and providing circulatory system access. They are widely used across hospitals, long-term care facilities, and home care settings, particularly among patients with urinary retention, cardiovascular conditions, or those undergoing dialysis.

The public payer segment was valued at USD 95.4 billion in 2024. Public payers include government-backed health programs and insurance plans that provide coverage for insured individuals. They often negotiate bulk pricing and emphasize cost-effective essential DME. Public payers are crucial in expanding access, especially in low-income and rural areas, with reimbursement policies directly influencing product availability and market demand.

North America Durable Medical Equipment Market held a substantial share in 2024, owing to advanced healthcare infrastructure, high medical expenditure, and a significant elderly population. The prevalence of chronic illnesses such as diabetes, cardiovascular disorders, and respiratory diseases drives long-term equipment use. The growing adoption of home healthcare and digital health technologies has accelerated demand for portable, connected devices. Government initiatives, including Medicare and Medicaid, further support access to essential DME products, particularly for geriatric and disabled populations.

Prominent players in the Global Durable Medical Equipment Market include B Braun, Baxter, BD, Cardinal Health, CAREX, Coloplast, COMPASS HEALTH, ConvaTec, Drive DeVilbiss Healthcare, Getinge, Graham-Field, INTCO MEDICAL, INVACARE, Koninklijke Philips, MEDLINE, Medtronic, ResMed, Stryker, and SUNRISE MEDICAL. Market leaders focus on product innovation, developing ergonomic, patient-specific, and connected devices to enhance usability and improve clinical outcomes. Companies invest heavily in R&D to integrate AI, wireless monitoring, and mobile connectivity into their equipment, differentiating themselves in the market. Strategic partnerships and collaborations with regional distributors, healthcare providers, and technology firms allow broader geographic reach and faster market penetration. Firms also leverage mergers and acquisitions to expand portfolios and strengthen supply chains. Focus on regulatory compliance, quality certifications, and government reimbursement programs to ensure market credibility and access.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Payer trends

- 2.2.4 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising patient preference for home-based care

- 3.2.1.2 Increasing prevalence of chronic diseases across the globe

- 3.2.1.3 Growing geriatric population

- 3.2.1.4 Technological advancements in products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High device costs and affordability challenges

- 3.2.2.2 Growing demand for pediatric-focused products

- 3.2.3 Opportunities

- 3.2.3.1 AI/ML integration and predictive analytics

- 3.2.3.2 Emerging markets expansion and infrastructure development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Investment landscape

- 3.7 Reimbursement scenario

- 3.8 Healthcare delivery model transformation

- 3.9 Personalized medicine and precision healthcare applications

- 3.10 Software as medical device (SaMD) integrated analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Gap analysis

- 3.14 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Personal mobility devices

- 5.2.1 Wheelchair and scooter

- 5.2.2 Crutches and canes

- 5.2.3 Walkers

- 5.2.4 Other personal mobility devices

- 5.3 Monitoring and therapeutic devices

- 5.3.1 Oxygen equipment

- 5.3.2 Blood glucose analyzers

- 5.3.3 Vital sign monitors

- 5.3.4 Infusion pumps

- 5.3.5 Continuous positive airway pressure (CPAP) devices

- 5.3.6 Nebulizers

- 5.3.7 Other monitoring and therapeutic devices

- 5.4 Bathroom safety devices

- 5.5 Medical furniture

- 5.6 Incontinent pads

- 5.7 Breast pumps

- 5.8 Catheters

- 5.9 Consumables and accessories

- 5.10 Other products

Chapter 6 Market Estimates and Forecast, By Payer, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Public

- 6.3 Private

- 6.4 Out-of-pocket

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Home healthcare

- 7.4 Ambulatory surgical centers

- 7.5 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 B Braun

- 9.2 Baxter

- 9.3 BD

- 9.4 Cardinal Health

- 9.5 CAREX

- 9.6 Coloplast

- 9.7 COMPASS HEALTH

- 9.8 convaTec

- 9.9 drive DeVilbiss Healthcare

- 9.10 Getinge

- 9.11 graham-field

- 9.12 INTCO MEDICAL

- 9.13 INVACARE

- 9.14 Koninklijke Philips

- 9.15 MEDLINE

- 9.16 Medtronic

- 9.17 ResMed

- 9.18 Stryker

- 9.19 SUNRISE MEDICAL