|

시장보고서

상품코드

1892690

전기 밴 컨버전 키트 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Electric Van Conversion Kits Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

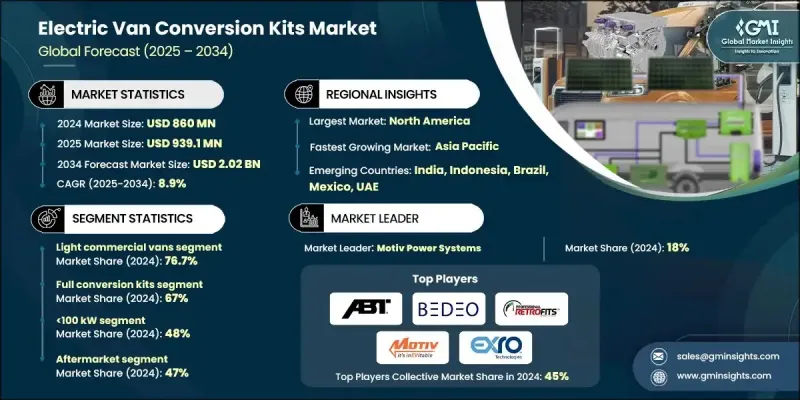

세계의 전기 밴 컨버전 키트 시장은 2024년에 8억 6,000만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 8.9%를 나타내 20억 2,000만 달러에 이를 것으로 예측됩니다.

텔레매틱스, IoT 시스템 및 최신 플릿 관리 소프트웨어의 진보를 통해 사업자는 루트 계획, 배터리 이용 효율, 유지 보수 일정 개선을 통해 차량 사용을 최적화할 수 있게 되었습니다. 기술이 발전함에 따라 전환 키트 자체도 더욱 정교 해지고 유연한 소유 모델로의 전환을 지원하고 있습니다. 많은 차량 운영사는 일괄 구입에서 구독 및 종량 과금제 옵션으로 이행하고 있으며 초기 투자를 최소화하면서 밴을 전동화할 수 있습니다. 이러한 재무 모델은 월간 비용을 보다 예측 가능하게 하며, 특히 중소기업을 포함한 함대 운영자가 업무 요구의 변화에 따라 규모를 조정할 수 있습니다. 전기 이동성으로의 광범위한 마이그레이션은 하드웨어 제공업체와 디지털 서비스 플랫폼 간의 협력 강화에 의해 더욱 강화되고 있으며, 운영자는 턴키 방식의 전기화 솔루션을 보다 쉽게 이용할 수 있게 되었습니다. 시장이 가속화됨에 따라 전기 밴으로의 개조는 도시 및 지역의 운송 경로에서 배출량 감소, 효율성 향상 및 운영 관리 개선을 요구하는 조직에 실용적이고 비용 효율적인 옵션이되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 가치 | 8억 6,000만 달러 |

| 예측 금액 | 20억 2,000만 달러 |

| CAGR | 8.9% |

소형 상용 밴 부문은 2024년에 76.7%의 점유율을 차지했고 2025년부터 2034년에 걸쳐 CAGR 9.6%를 나타낼 것으로 예측됩니다. 이러한 이점은 전형적인 소형 상업용 차량의 가동 사이클과 현재 배터리 전기자동차의 성능이 일치하는 것에 의해 지원되며, 일상적인 주행 거리 요구 사항 및 적재 요구는 현대 전기 밴의 성능 프로파일에 적합합니다. 낮은 배출가스 지역에 대한 접근성 확대와 유리한 운영비용은 주요 지역 전반에 걸쳐 총소유비용(TCO)이 개선되고 있는 가운데 도입을 더욱 촉진하고 있습니다.

전체 전환 키트 부문은 2024년에 67%의 점유율을 차지했으며 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 10%를 나타낼 것으로 예측됩니다. 완전 전동화 컨버전 패키지는 모듈식으로 플랫폼 독립적인 설계로 전환하여 설치 시간을 단축하고 다양한 밴 모델로의 호환성 확대를 실현하고 있습니다. 표준화된 고전압 구성 요소를 기반으로 한 통합형 배터리·모터 시스템과 텔레매틱스 지원형 진단 기능의 조합으로 플릿의 가동률이 향상되어 라스트마일 배송 및 도시 배송 용도에 있어서 전동화의 매력이 높아지고 있습니다.

미국의 전기 밴 컨버전 키트 시장은 2024년 2억 5,710만 달러에 달했습니다. 기업의 강력한 지속가능성 목표와 연방 및 주 배출가스 규제가 결합되어, 차량 운영사는 새로운 전기 밴 구매를 위한 비용 효율적인 선택으로 전환 키트의 도입을 추진하고 있습니다. 정부자금, 세제우대조치, 조성금은 중소규모 조직의 신속한 이행을 지원하고, 지방자치단체와 물류사업자가 규제 준수 기한을 충족하기 위해 개조에 크게 의존하는 요인이 되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 이익률

- 비용 구조

- 각 단계별 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 소유보다 유연한 모빌리티를 우선하는 사고방식

- 전기자동차의 보급 확대와 플릿 전동화

- 증가하는 기업용 플릿 수요

- 커넥티드카 및 텔레매틱스의 진전

- 업계의 잠재적 위험 및 과제

- 고액의 자본 투자

- 규제 및 보험에 관한 과제

- 시장 기회

- 신흥도시 시장에서의 확대

- 스마트 시티 및 MaaS 플랫폼과의 통합

- 보험 및 유지관리와의 세트 서비스

- 특수 EV 및 상용차 솔루션

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 세계

- EPA 대체연료변환규제

- NHTSA FMVSS 기준(FMVSS 305a)

- 캘리포니아주 대기자원국(CARB) 인증 요건

- 연식 기반 인증 절차

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 세계

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신 현황

- 현재 기술 동향

- 배터리 기술의 진화(NMC, LFP, 고체 전지의 로드맵)

- 모터 및 인버터의 기술 혁신(코일 구동 기술, 효율 향상)

- 열 관리 시스템(수동 냉각과 능동 냉각의 비교)

- 신흥 기술

- 차량 제어 유닛(VCU) 및 소프트웨어 아키텍처

- 회생 브레이크의 최적화

- 모듈식 확장 가능 배터리 구성

- 통합 충전 솔루션(자동차 충전기 통합)

- 현재 기술 동향

- 가격 분석

- 차량 클래스별 전환 키트 가격

- 배터리 팩의 비용 동향

- 설치 작업의 노무 비용 구조

- 충전 인프라 비용(레벨 2 충전과 직류 급속 충전의 비교)

- 코스트 내역 분석

- 특허 분석

- 파워트레인 통합에 관한 특허

- 배터리 패키징 및 열 관리에 관한 특허

- 전자식 변속 기구 및 코일 구동 기술에 관한 특허(Exro)

- 충전 인터페이스 및 통신 프로토콜에 관한 특허

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 이용 사례

- 최상의 시나리오

- 투자 및 자금 조달 분석

- 연방 인프라 자금(NEVI, CFI 프로그램)

- IRA 제조 인센티브 및 OBBBA 개정

- 주 및 지역 보조금 프로그램(HVIP, NYTVIP, 텍사스 주)

- 전환 기술 기업에 대한 민간 투자

- 충전 인프라 통합

- 디포 충전 설계 및 사이트 계획

- 전력회사와의 조정 및 계통 연계 스케줄

- 관리형 충전 전략

- 충전기와 차량의 호환성(CCS, J1772, 전력 레벨)

- 차량 플랫폼의 적합성 및 검증

- 플랫폼 선정 기준

- 포드 트랜짓 플랫폼 분석

- RAM 프로마스터 플랫폼 분석

- GM 익스프레스/사바나 플랫폼 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병

- 파트너십 및 협력

- 신제품 출시

- 사업 확대 계획과 자금 조달

- 제품 및 서비스 벤치마킹

- R&D 투자 분석

- 벤더 선정 기준

제5장 시장 추계·예측 : 차량별(2021-2034년)

- 주요 동향

- 소형 상용차

- 중형 상용차

- 대형 상용차

제6장 시장 추계·예측 : 변환 방식별(2021-2034년)

- 주요 동향

- 완전 전기 컨버전 키트

- 하이브리드 전기 전환 키트

제7장 시장 추계·예측 : 추진력별(2021-2034년)

- 주요 동향

- 최대 100kW

- 100-200kW

- 200kW 초과

제8장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 상업용 차량 사업자

- 물류 및 배송 회사

- 지방자치단체 당국

- 유틸리티 및 서비스 제공업체

- 중소기업

제9장 시장 추계·예측 : 판매 채널별(2021-2034년)

- 주요 동향

- OEM 전환 키트

- 애프터마켓 전환 키트

- 인증된 개조 업체

제10장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 폴란드

- 루마니아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ANZ

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계 기업

- ABT e-Line

- BEDEO

- Contravans

- E-Drive Retrofits

- EV West

- Lightning eMotors

- Motiv Power Systems

- REE Automotive

- Ricardo

- SEA Electric(Exro)

- 지역 기업

- BisonEV Retrofits

- Efficient Drivetrains Inc.(EDI)

- Hyliion

- Logan Bus Company

- Odyne Systems

- Optimal EV

- Phoenix Motorcars

- TransPower

- Unique Electric Solutions

- US Hybrid

- 신흥 기업

- Arrival

- Bollinger Motors

- Canoo

- Chanje

- Electric Last Mile Solutions(ELMS)

- GreenPower Motor Company

- Harbinger Motors

- Proterra

- Rivian(Commercial Van Division)

- Vicinity Motor Corp

The Global Electric Van Conversion Kits Market was valued at USD 860 million in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 2.02 billion by 2034.

Advancements in telematics, IoT systems, and modern fleet-management software are enabling operators to optimize vehicle usage by improving route planning, battery utilization, and maintenance scheduling. Conversion kits themselves are becoming more advanced as technology evolves, supporting the shift toward flexible ownership models. Many fleet operators are moving from outright purchasing to subscription and pay-per-use options, allowing them to convert vans to electric power with minimal upfront capital. These financial models create more predictable monthly expenses and allow fleet operators, especially smaller businesses, to scale as operational needs change. The broader shift toward electric mobility is further supported by increasing integration between hardware providers and digital service platforms, giving operators greater access to turnkey electrification solutions. As the market accelerates, electric van conversions are becoming a practical and cost-effective pathway for organizations seeking lower emissions, higher efficiency, and improved operational control across urban and regional transport routes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $860 Million |

| Forecast Value | $2.02 Billion |

| CAGR | 8.9% |

The light commercial vans segment held a 76.7% share in 2024 and is anticipated to grow at a 9.6% CAGR through 2025-2034. This dominance is supported by the alignment between typical light-commercial duty cycles and current battery-electric capabilities, with daily mileage requirements and payload needs fitting within contemporary electric van performance profiles. Expanding access to low-emission zones and favorable operating costs further strengthen adoption as the total cost of ownership continues to improve across key regions.

The full conversion kits segment held a 67% share in 2024 and is expected to grow at a CAGR of 10% from 2025 to 2034. Fully electric conversion packages are moving toward modular, platform-agnostic engineering that shortens installation times and broadens compatibility across various van models. Integrated battery and motor systems built around standardized high-voltage components, combined with telematics-supported diagnostics, are increasing utilization rates for fleets and enhancing the appeal of electrification for last-mile and urban delivery applications.

US Electric Van Conversion Kits Market reached USD 257.1 million in 2024. Strong corporate sustainability targets, paired with federal and state emissions requirements, are motivating fleets to adopt conversion kits as a cost-effective alternative to purchasing new electric vans. Government funding, tax incentives, and grants assist small and mid-sized organizations in transitioning quickly, prompting municipalities and logistics providers to rely more heavily on retrofitting to meet compliance timelines.

Key companies active in the Electric Van Conversion Kits Market include ABT e-Line, BEDEO, Contravans, E-Drive Retrofits, EV West, Motiv Power Systems, REE Automotive, Ricardo, and SEA Electric (Exro). Companies in the Electric Van Conversion Kits Market are strengthening their market position by developing modular, standardized platforms that work across multiple vehicle types, reducing installation complexity and shortening fleet downtime. Many firms are expanding service partnerships with fleet operators to offer bundled packages that include conversion hardware, software integration, maintenance, and telematics support. Subscriptions and leasing programs are becoming central strategies, allowing customers to adopt electrification with reduced upfront costs.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Conversion

- 2.2.4 Propulsion

- 2.2.5 End Use

- 2.2.6 Sales channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Preference for flexible mobility over ownership

- 3.2.1.2 Growing EV adoption and fleet electrification

- 3.2.1.3 Rising corporate fleet demand

- 3.2.1.4 Connected vehicle and telematics advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital investment

- 3.2.2.2 Regulatory and insurance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging urban markets

- 3.2.3.2 Integration with smart cities and MaaS platforms

- 3.2.3.3 Bundled services with insurance and maintenance

- 3.2.3.4 Specialized EV and commercial vehicle solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Global

- 3.4.1.1 EPA alternative fuel conversion regulations

- 3.4.1.2 NHTSA FMVSS standards (FMVSS 305a)

- 3.4.1.3 CARB certification requirements

- 3.4.1.4 Age-based certification pathways

- 3.4.2 North America

- 3.4.3 Europe

- 3.4.4 Asia Pacific

- 3.4.5 Latin America

- 3.4.6 Middle East & Africa

- 3.4.1 Global

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Battery technology evolution (NMC, LFP, solid-state roadmap)

- 3.7.1.2 Motor & inverter advancements (coil driver tech, efficiency gains)

- 3.7.1.3 Thermal management systems (passive vs active cooling)

- 3.7.2 Emerging technologies

- 3.7.2.1 Vehicle control unit (VCU) & software architecture

- 3.7.2.2 Regenerative braking optimization

- 3.7.2.3 Modular & scalable battery configurations

- 3.7.2.4 Integrated charging solutions (on-board charger integration)

- 3.7.1 Current technological trends

- 3.8 Pricing analysis

- 3.8.1 Conversion kit pricing by vehicle class

- 3.8.2 Battery pack cost trends

- 3.8.3 Installation labor cost structure

- 3.8.4 Charging infrastructure costs (Level 2 vs DC fast charging)

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.10.1 Powertrain integration patents

- 3.10.2 Battery packaging & thermal management patents

- 3.10.3 Electronic gearing & coil driver technology patents (Exro)

- 3.10.4 Charging interface & communication protocol patents

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use cases

- 3.13 Best case scenario

- 3.14 Investment & funding analysis

- 3.14.1 Federal infrastructure funding (NEVI, CFI programs)

- 3.14.2 IRA manufacturing incentives & OBBBA modifications

- 3.14.3 State & regional grant programs (HVIP, NYTVIP, Texas)

- 3.14.4 Private investment in conversion technology companies

- 3.15 Charging infrastructure integration

- 3.15.1 Depot charging design & site planning

- 3.15.2 Utility coordination & interconnection timelines

- 3.15.3 Managed charging strategies

- 3.15.4 Charger-vehicle compatibility (CCS, J1772, power levels)

- 3.16 Vehicle platform suitability & validation

- 3.16.1 Platform selection criteria

- 3.16.2 Ford Transit platform analysis

- 3.16.3 RAM ProMaster platform analysis

- 3.16.4 GM Express/Savana platform analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Product and service benchmarking

- 4.8 R&D investment analysis

- 4.9 Vendor selection criteria

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Light commercial vehicles

- 5.3 Medium commercial vehicles

- 5.4 Heavy commercial vehicles

Chapter 6 Market Estimates & Forecast, By Conversion, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Fully electric conversion kits

- 6.3 Hybrid electric conversion kits

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 < 100 kW

- 7.3 100-200 kW

- 7.4 >200 kW

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Commercial fleet operators

- 8.3 Logistics & delivery companies

- 8.4 Municipal authorities

- 8.5 Utility & service providers

- 8.6 Small & medium enterprises

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM conversion kits

- 9.3 Aftermarket conversion kits

- 9.4 Certified retrofitters

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 ABT e-Line

- 11.1.2 BEDEO

- 11.1.3 Contravans

- 11.1.4 E-Drive Retrofits

- 11.1.5 EV West

- 11.1.6 Lightning eMotors

- 11.1.7 Motiv Power Systems

- 11.1.8 REE Automotive

- 11.1.9 Ricardo

- 11.1.10 SEA Electric (Exro)

- 11.2 Regional players

- 11.2.1 BisonEV Retrofits

- 11.2.2 Efficient Drivetrains Inc. (EDI)

- 11.2.3 Hyliion

- 11.2.4 Logan Bus Company

- 11.2.5 Odyne Systems

- 11.2.6 Optimal EV

- 11.2.7 Phoenix Motorcars

- 11.2.8 TransPower

- 11.2.9 Unique Electric Solutions

- 11.2.10 US Hybrid

- 11.3 Emerging players

- 11.3.1 Arrival

- 11.3.2 Bollinger Motors

- 11.3.3 Canoo

- 11.3.4 Chanje

- 11.3.5 Electric Last Mile Solutions (ELMS)

- 11.3.6 GreenPower Motor Company

- 11.3.7 Harbinger Motors

- 11.3.8 Proterra

- 11.3.9 Rivian (Commercial Van Division)

- 11.3.10 Vicinity Motor Corp