|

시장보고서

상품코드

1892699

이식형 약물전달 펌프 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Implantable Drug Delivery Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

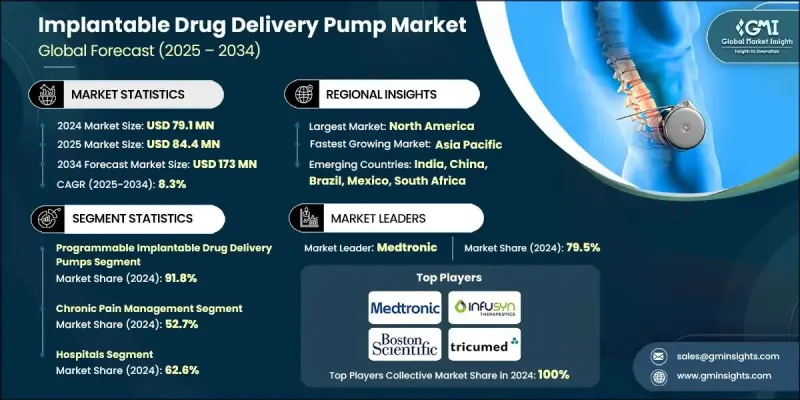

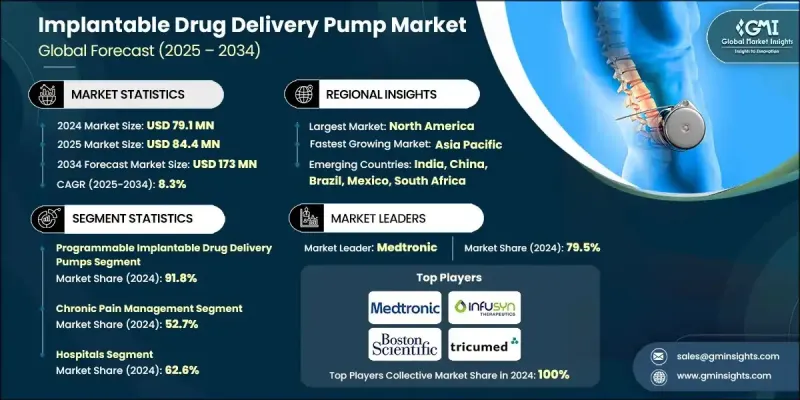

세계의 이식형 약물전달 펌프 시장은 2024년에 7,910만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 8.3%로 성장하여 1억 7,300만 달러에 이를 것으로 예측됩니다.

만성 통증, 경련 및 기타 장기 질환의 유병률 증가는 제어되고 지속적인 약물 전달을 보장하는 첨단 임플란트 펌프에 대한 수요를 주도하고 있습니다. 병원, 전문 클리닉, 외래수술센터(ASC)에서는 환자 결과 개선, 만성 질환의 효과적인 관리, 운영 효율성 향상을 목적으로 이러한 시스템 도입이 확대되고 있습니다. 본 시장에서는 정밀하고 표적화된 치료를 제공하고, 전신 부작용을 줄이며, 복약 순응도를 향상시키는 프로그래머블 펌프 및 정속 펌프가 제공되고 있습니다. 소형화된 펌프 설계, 생체 적합성 3D 프린팅 부품, 무선 원격 측정, 원격 환자 모니터링 등의 기술 발전은 장치의 기능, 안전성, 편의성을 향상시켜 임상 도입을 가속화하고 전 세계 만성 질환 관리에 더 광범위하게 사용하도록 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 개시 연도 시장 규모 | 7,910만 달러 |

| 예측 금액 | 1억 7,300만 달러 |

| CAGR | 8.3% |

2024년 기준, 프로그래밍이 가능한 이식형 약물 전달 펌프 부문은 91.8%의 점유율을 차지했습니다. 이 펌프는 개별화된 정밀하고 제어된 약물 투여를 가능하게 하는 특성으로 높은 평가를 받고 있습니다. 임상의는 환자의 반응, 질병 진행 상황, 치료 요구에 따라 용량을 조절할 수 있어 부작용을 최소화하면서 치료 결과를 개선할 수 있습니다. 이러한 유연성으로 인해 프로그램 가능한 펌프는 지속적이고 정밀한 약물 투여가 필요한 만성 질환에서 필수적인 존재가 되었습니다.

만성 통증 관리 부문은 2024년 52.7%의 점유율을 차지했으며, 2025년부터 2034년까지 8,790만 달러에 달할 것으로 예측됩니다. 신경병증성 통증, 근골격계 통증, 수술 후 통증 증가가 수요를 견인하고 있으며, 이식형 펌프는 진통제를 직접적이고 효율적으로 투여하기 때문에 경구약이나 전신치료에 비해 빠른 효과 발현과 치료 효과의 향상을 기대할 수 있습니다.

북미 이식형 약물 전달 펌프 시장은 선진화된 의료 인프라, 강력한 상환 제도, 혁신적인 의료 기술의 조기 도입에 힘입어 2024년 61.8%의 점유율을 차지했습니다. 이 지역의 높은 만성질환 유병률과 저침습적 치료에 대한 선호도가 높아지면서 병원과 전문 클리닉에서 펌프 도입을 촉진하고 있습니다. 미국 FDA와 캐나다 보건부의 유리한 규제 경로가 더욱 빠른 상용화와 혁신을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술적 진보

- 현재 기술 동향

- 소형화 임플란트 펌프

- 프로그래밍 가능한 환자 친화적인 주입 시스템

- 저침습 임베디드 기술

- 신기술

- AI 기반 투여 알고리즘을 탑재한 스마트팜프

- 무선 접속과 원격 모니터링

- 통합된 안전 및 경보 시스템

- 현재 기술 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 향후 시장 동향

- AI, 디지털 헬스 및 접속형 수액 시스템 통합

- 약물 및 의료기기 복합 요법 개발

- 의료 인프라가 개선되는 신흥 시장 성장

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추산 및 예측 : 제품 유형별, 2021-2034

- 주요 동향

- 프로그래머블 이식형 약물전달 펌프

- 정속(고정 유량) 이식형 펌프

제6장 시장 추산 및 예측 : 용도별, 2021-2034

- 주요 동향

- 만성 통증 관리

- 경련성 관리

- 종양학 및 화학요법

- 기타 만성질환

제7장 시장 추산 및 예측 : 최종 용도별, 2021-2034

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타 용도

제8장 시장 추산 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 지역

제9장 기업 개요

- Boston Scientific(Integra Oncology)

- Infusyn Therapeutics

- Medtronic

- Tricumed Medizintechnik

The Global Implantable Drug Delivery Pump Market was valued at USD 79.1 million in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 173 million by 2034.

The rising prevalence of chronic pain, spasticity, and other long-term disorders is driving demand for advanced implantable pumps that ensure controlled and sustained drug delivery. Hospitals, specialty clinics, and ambulatory surgical centers are increasingly adopting these systems to enhance patient outcomes, manage chronic conditions more effectively, and improve operational efficiency. The market offers programmable and constant-rate pumps that provide precise, targeted therapy, reducing systemic side effects and improving adherence. Technological advancements, including miniaturized pump designs, biocompatible 3D-printed components, wireless telemetry, and remote patient monitoring, are enhancing device functionality, safety, and convenience, accelerating clinical adoption and encouraging broader use in chronic disease management globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $79.1 Million |

| Forecast Value | $173 Million |

| CAGR | 8.3% |

The programmable implantable drug delivery pumps segment held 91.8% share in 2024. These pumps are favored due to their ability to provide personalized, precise, and controlled drug administration. Clinicians can adjust dosages based on patient response, disease progression, and therapy needs, improving outcomes while minimizing adverse effects. This flexibility makes programmable pumps essential for chronic conditions requiring ongoing, precise medication delivery.

The chronic pain management segment accounted for a 52.7% share in 2024 and is expected to reach USD 87.9 million during 2025-2034. Rising cases of neuropathic, musculoskeletal, and post-surgical pain are fueling demand, as implantable pumps deliver analgesics directly and efficiently, ensuring rapid onset and enhanced therapeutic efficacy compared to oral or systemic treatments.

North America Implantable Drug Delivery Pump Market held a 61.8% share in 2024, supported by advanced healthcare infrastructure, strong reimbursement systems, and early adoption of innovative medical technologies. The high prevalence of chronic diseases in the region and the growing preference for minimally invasive therapies are driving pump adoption in hospitals and specialty clinics. Favorable regulatory pathways by the U.S. FDA and Health Canada further encourage rapid commercialization and innovation.

Major players operating in the Global Implantable Drug Delivery Pump Market include Medtronic, Infusyn Therapeutics, Boston Scientific (Integra Oncology), and Tricumed Medizintechnik. Companies in the implantable drug delivery pump market are focusing on strategies such as investing heavily in R&D to develop miniaturized, programmable, and remote-monitoring-enabled pumps. Strategic partnerships with hospitals, specialty clinics, and research institutions help expand their distribution networks and clinical adoption. Firms are also emphasizing global market expansion, enhancing regulatory compliance, and implementing targeted marketing strategies to raise awareness among clinicians and patients. Product differentiation through advanced telemetry, wireless communication, and customizable therapy options ensures competitive advantage, while ongoing innovation and service support strengthen brand loyalty and penetration in chronic disease management segments.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic pain, spasticity, and cancer

- 3.2.1.2 Advantages of targeted and controlled drug delivery

- 3.2.1.3 Technological advancements in pump design

- 3.2.1.4 Growing preference for minimally invasive therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High device and implantation cost

- 3.2.2.2 Risk of device malfunction and infection

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of IoT and remote monitoring

- 3.2.3.2 Rising demand for personalized medicine

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancemnets

- 3.5.1 Current technological trends

- 3.5.1.1 Miniaturized implantable pumps

- 3.5.1.2 Programmable and patient-friendly infusion systems

- 3.5.1.3 Minimally invasive implantation techniques

- 3.5.2 Emerging technologies

- 3.5.2.1 Smart pumps with AI-based dosing algorithms

- 3.5.2.2 Wireless connectivity and remote monitoring

- 3.5.2.3 Integrated safety and alert systems

- 3.5.1 Current technological trends

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.9.1 Integration of AI, digital health, and connected infusion systems

- 3.9.2 Development of combination drug-device therapies

- 3.9.3 Growth in emerging markets with improving healthcare infrastructure

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Programmable implantable drug delivery pumps

- 5.3 Constant-rate (Fixed-flow) implantable pumps

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Chronic pain management

- 6.3 Spasticity management

- 6.4 Oncology/Chemotherapy

- 6.5 Other chronic conditions

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 RoW

Chapter 9 Company Profiles

- 9.1 Boston Scientific (Integra Oncology)

- 9.2 Infusyn Therapeutics

- 9.3 Medtronic

- 9.4 Tricumed Medizintechnik