|

시장보고서

상품코드

1892711

나트륨 이온 배터리 재료 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Sodium Ion Battery Material Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

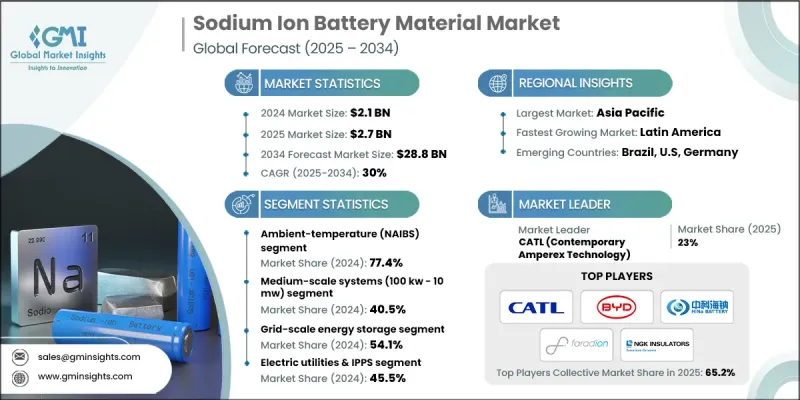

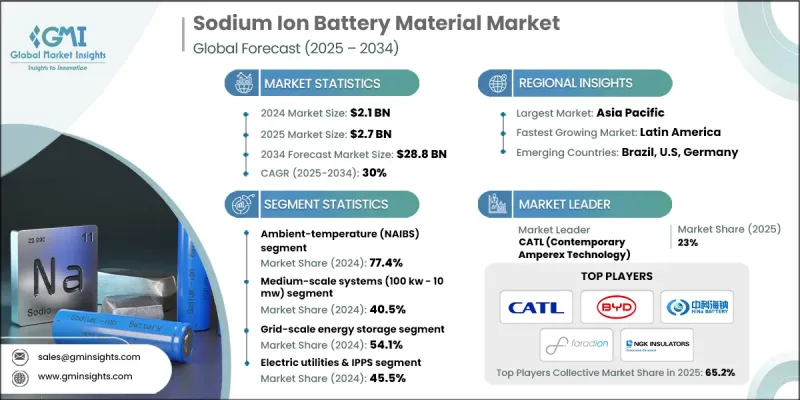

세계의 나트륨 이온 배터리 재료 시장은 2024년 21억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 30%를 나타내 288억 달러에 이를 것으로 예측됩니다.

플루시안 블루 유사체(PBA) 양극 재료의 혁신과 고출력 특성 향상이 지속적으로 주목을 받고 있는 가운데, 이 기술은 초기 개발 단계를 넘어 보다 광범위한 상업화를 향해 진전하고 있습니다. 160-175 Wh/kg에 달하는 에너지 밀도의 향상과 확대되는 수 GWh 규모의 제조 능력이 함께 세계의 보급이 가속하고 있습니다. 또, 리튬계 재료에의 의존도 저감을 목표로 하는 세계의 이해 관계자의 움직임을 받아, 정부의 지원책도 나트륨 이온 배터리 생산에 대한 투자를 촉진하고 있습니다. 각종 인센티브 프로그램을 통한 국내 공급망 구축의 추진은 산업 인프라를 더욱 강화하고 있습니다. 성능 향상과 자본 요건의 감소로 나트륨 이온 시스템은 그리드 규모의 축전, 백업 전원 네트워크, 마이크로그리드, 단거리 이동성 용도에 대한 채택이 확대되고 있습니다. 여러 지역에서는 중요한 광물 공급 체인의 부담 경감을 목적으로 한 생산 촉진이 진행되고 있으며, 경질 탄소 음극, 셀 조립 프로세스, 재활용 시설에서의 지속적인 기술 진보가 본 기술의 대규모 전개를 가능하게 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 가치 | 21억 달러 |

| 예측 금액 | 288억 달러 |

| CAGR | 30% |

상온(NAIBS) 시스템 부문은 2024년에 77.4%의 점유율을 차지했고 2034년까지 연평균 복합 성장률(CAGR) 29.4%를 나타낼 것으로 예측됩니다. 상업용도로의 급속한 도입, 유리한 비용구조, 거치형 축전시스템과 단거리 모빌리티와의 높은 호환성이 함께 주요기술로서의 역할을 강화하고 있습니다. 차세대 PBA 및 적층 산화물 재료의 생산이 여러 시설에서 확대됨에 따라 성장이 계속될 것으로 예측됩니다.

중규모 시스템 부문은 백업 전원 네트워크, 배전 레벨 에너지 자원, 마이크로그리드 환경 등 상업 및 산업 분야의 설치 증가에 힘입어 2024년 8억 8,370만 달러 시장 규모를 창출했습니다. 그 적응성과 간편한 도입성은 데이터 집약적인 환경, 통신 분야, 고 수요 충전 오퍼레이션을 지원하는 솔루션에서 매력적인 선택이 되고 있습니다.

북미의 나트륨 이온 배터리 재료 시장은 2024년에 21.3%의 점유율을 차지했고, 대규모 에너지 저장 및 재생에너지 용량 확대 수요 증가에 따라 기세를 늘리고 있습니다. 이 지역은 지원 금융 정책, 조달 요구 사항 및 필수 원료에 대한 접근을 통해 안정적인 공급을 보장 할 수있는 이점이 있습니다. 미국 및 캐나다의 유틸리티회사는 장시간 저장, 내장해성 강화, 한랭지에서의 효과적인 성능을 목적으로 나트륨 이온 시스템의 도입을 검토하고 있습니다. 마이크로그리드에 대한 관심 증가와 원격지의 전기화도 함께 북미는 상업 전개에 있어서 새로운 핫스팟으로 자리매김하고 있습니다. 데이터 네트워크 및 통신 인프라에서도 신뢰성과 전력 안정성을 지원하기 위해 나트륨 이온 기술의 이용이 확대되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 이익률

- 각 단계별 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 중요 광물에의 의존 탈각 : 리튬, 코발트, 니켈에 대한 의존 해소

- 비용 경쟁력 : 대규모 생산 시 LFP 배터리에 비해 20-30% 낮은 제조 비용

- 한랭지 성능 : -40°C에서 90% 이상의 용량 유지율을 실현해, 북방 시장 전개를 가능하게 합니다.

- 업계의 잠재적 위험 및 과제

- 에너지 밀도의 낮음 : 140-175 Wh/kg 승용 전기자동차의 보급을 제한하는 요인

- 규격 및 인증의 갭 : 나트륨 이온 배터리 전용의 시험 프로토콜의 부족

- 경질 탄소 양극 공급 제약 : 국내 생산 능력의 제한

- 시장 기회

- 22,255MW의 미국 유틸리티 규모 배터리 증설(2023-2026)이 거치형 축전을 목표로

- 방위 및 군사 용도 : BABA 준거의 국내 공급 체인

- 고사이클 수명 주파수 조정 : 50,000사이클 이상을 실현해, 110달러/kW-년(연간 kW당)의 수익을 가능하게 합니다.

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 배터리 기술 유형별

- 향후 시장 동향

- 기술 및 혁신 현황

- 현재 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 파트너십 및 협력

- 신제품 출시

- 사업 확대 계획

제5장 시장 추계·예측 : 배터리 기술 유형별(2021-2034년)

- 상온 나트륨 이온 배터리

- 프러시안 블루 유사체(PBA) 양극

- 층상 전이 금속 산화물 양극

- 폴리아니온 음극

- 고온 용융 배터리

- 나트륨-황(NaS) 배터리

- 나트륨-금속 할라이드(Na-NiCl2/ZEBRA) 배터리

- 중온 나트륨 배터리(200℃ 미만)

- 고체 배터리

- 세라믹 고체 전해질

- 폴리머 고체 전해질

제6장 시장 추계·예측 : 용량 규모별(2021-2034년)

- 소규모(100kW 미만)

- 중규모(100kW-10MW)

- 대규모(10MW-100MW)

- 초대규모(100MW 초과)

제7장 시장 추계·예측 : 용도별(2021-2034년)

- 그리드 규모 에너지 저장

- 주파수 조정 및 부대 서비스

- 에너지 차익 거래 및 피크 절감

- 신재생에너지 통합 및 안정화

- 송배전망 업그레이드 연기

- 블랙 스타트 및 그리드 복원력

- 상업 및 산업용 저장

- 데이터센터 및 통신 백업 전력

- 산업용 피크 절감 및 수요 반응

- 마이크로그리드 및 분산 발전 지원

- EV 급속 충전 인프라

- 주택용 에너지 저장

- 태양광 자가 소비 및 백업

- 가상 발전소(VPP) 집계

- 전기자동차의 응용 분야

- 승용 전기자동차(BEV 및 PHEV)

- 이륜차 및 삼륜차

- 상용 버스 및 대형 트럭

- 배터리 교환 시스템

- 국방 및 군사

- 군용 차량 및 휴대용 전력

- 원격지 시설 및 중요 인프라

제8장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 전력 회사 및 독립 발전 사업자(IPP)

- 통신 및 데이터센터

- 자동차 제조업체 및 전기자동차 제조업체

- 산업 및 제조

- 재생에너지 개발사

- 정부 및 방위

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Altris AB

- AMTE Power plc

- BYD

- CATL(Contemporary Amperex Technology Co., Ltd.)

- Hina Battery

- NGK Insulators

- Natron Energy, Inc.

- Reliance

- Tiamat Energy(Neogy)

- Xiamen Tob New Technology Co Ltd

The Global Sodium Ion Battery Material Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 30% to reach USD 28.8 billion by 2034.

This technology is moving beyond early-stage development and progressing toward broader commercialization as innovations in prussian blue analog (PBA) cathodes and improved high-rate capabilities continue to gain traction. Energy density enhancements reaching 160-175 Wh/kg, combined with expanding multi-GWh manufacturing capacity, are accelerating worldwide adoption. Supportive government initiatives are also encouraging investment in sodium-ion production as global stakeholders aim to reduce dependence on lithium-based materials. The push toward domestic supply chains through various incentive programs is further strengthening industry infrastructure. As performance improves and capital requirements decline, sodium-ion systems are increasingly being incorporated into grid-scale storage, backup power networks, microgrids, and short-distance mobility applications. Several regions are promoting production to ease the pressure on critical mineral supply chains, while ongoing advancements in hard-carbon anodes, cell assembly processes, and recycling facilities position the technology for large-scale deployment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $28.8 Billion |

| CAGR | 30% |

The ambient-temperature (NAIBS) systems segment held 77.4% in 2024 and is projected to grow at a CAGR of 29.4% through 2034. Their rapid integration into commercial uses, combined with favorable cost profiles and strong compatibility with stationary storage and short-range mobility, is reinforcing their role as a key technology. Growth is expected to continue as production of next-generation PBA and layered-oxide materials is expanded across multiple facilities.

The medium-scale systems segment generated USD 883.7 million in 2024, supported by rising installations across commercial and industrial applications, including backup power networks, distribution-level energy resources, and microgrid environments. Their adaptability and straightforward deployment make them an appealing choice for data-intensive environments, telecommunications, and solutions that assist high-demand charging operations.

North America Sodium Ion Battery Material Market accounted for 21.3% share in 2024 and continues to gain momentum as demand for large-scale energy storage and renewable capacity expansion increases. The region benefits from supportive financial policies, procurement requirements, and access to essential raw materials, enabling consistent supply availability. Utilities across the U.S. and Canada are evaluating sodium-ion systems for long-duration storage, resilience enhancement, and effective cold-weather performance. Growing interest in microgrids and electrification of remote areas also positions North America as an emerging hotspot for commercial deployment. Data networks and communication infrastructure are expanding their use of sodium-ion technology to support reliability and power stability.

Key participants in the Sodium Ion Battery Material Market include Altris AB, AMTE Power plc, BYD, CATL (Contemporary Amperex Technology Co., Ltd.), Hina Battery, NGK Insulators, Natron Energy, Inc., Reliance, Tiamat Energy (Neogy), and Xiamen Tob New Technology Co. Ltd. Companies active in the Sodium Ion Battery Material Market are adopting several strategies to enhance their competitive edge and broaden their market reach. Many are rapidly scaling manufacturing capacity to support multi-GWh output, enabling cost reductions and improved supply stability. Firms are investing heavily in advanced anode and cathode material development to boost energy density, cycle life, and performance in extreme temperatures. Strategic collaborations with energy storage developers and mobility solution providers are strengthening integration across end-use sectors. Organizations are also focusing on regional production localization to benefit from policy incentives and reduce supply chain risks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Battery Technology Type

- 2.2.3 Capacity Size

- 2.2.4 Application

- 2.2.5 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Critical Mineral Independence: Eliminating Lithium, Cobalt & Nickel Dependencies

- 3.2.1.2 Cost Competitiveness: 20-30% Lower Production Costs vs. LFP at Scale

- 3.2.1.3 Cold-Climate Performance: >90% Capacity Retention at -40°C Enabling Northern Markets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lower Energy Density: 140-175 Wh/kg Limiting Passenger EV Adoption

- 3.2.2.2 Standards & Certification Gaps: Lack of Sodium-Ion-Specific Testing Protocols

- 3.2.2.3 Hard Carbon Anode Supply Constraints: Limited Domestic Production Capacity

- 3.2.3 Market opportunities

- 3.2.3.1 22,255 MW U.S. Utility-Scale Battery Additions (2023-2026) Targeting Stationary Storage

- 3.2.3.2 Defense & Military Applications: BABA-Compliant Domestic Supply Chains

- 3.2.3.3 High-Cycle-Life Frequency Regulation: >50,000 Cycles Enabling $110/kW-yr Revenue

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Battery Technology Type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Battery Technology Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Ambient-Temperature NaIBs

- 5.2.1 Prussian Blue Analog (PBA) Cathodes

- 5.2.2 Layered Transition Metal Oxide Cathodes

- 5.2.3 Polyanion Cathodes

- 5.3 High-Temperature Molten

- 5.3.1 Sodium-Sulfur (NaS) Batteries

- 5.3.2 Sodium-Metal Halide (Na-NiCl2/ZEBRA) Batteries

- 5.3.3 Intermediate-Temperature Sodium Batteries (<200°C)

- 5.4 Solid State Battery

- 5.4.1 Ceramic Solid Electrolytes

- 5.4.2 Polymer Solid Electrolytes

Chapter 6 Market Estimates and Forecast, By Capacity Size, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Small-Scale (<100 kW)

- 6.3 Medium-Scale (100 kW - 10 MW)

- 6.4 Large-Scale (10 MW - 100 MW)

- 6.5 Extra-Large-Scale (>100 MW)

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Grid-Scale Energy Storage

- 7.2.1 Frequency Regulation & Ancillary Services

- 7.2.2 Energy Arbitrage & Peak Shaving

- 7.2.3 Renewable Energy Integration & Firming

- 7.2.4 Transmission & Distribution Upgrade Deferral

- 7.2.5 Black Start & Grid Resilience

- 7.3 Commercial & Industrial Storage

- 7.3.1 Data Center & Telecom Backup Power

- 7.3.2 Industrial Peak Shaving & Demand Response

- 7.3.3 Microgrid & Distributed Generation Support

- 7.3.4 EV Fast Charging Infrastructure

- 7.4 Residential Energy Storage

- 7.4.1 Solar Self-Consumption & Backup

- 7.4.2 Virtual Power Plant (VPP) Aggregation

- 7.5 Electric Vehicle Applications

- 7.5.1 Passenger Electric Vehicles (BEVs & PHEVs)

- 7.5.2 Two-Wheelers & Three-Wheelers

- 7.5.3 Commercial Buses & Heavy-Duty Trucks

- 7.5.4 Battery Swapping Systems

- 7.6 Defense & Military

- 7.6.1 Military Vehicles & Portable Power

- 7.6.2 Remote Installations & Critical Infrastructure

Chapter 8 Market Estimates and Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Electric Utilities & IPPs

- 8.3 Telecommunications & Data Centers

- 8.4 Automotive OEMs & EV Manufacturers

- 8.5 Industrial & Manufacturing

- 8.6 Renewable Energy Developers

- 8.7 Government & Defense

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Altris AB

- 10.2 AMTE Power plc

- 10.3 BYD

- 10.4 CATL (Contemporary Amperex Technology Co., Ltd.)

- 10.5 Hina Battery

- 10.6 NGK Insulators

- 10.7 Natron Energy, Inc.

- 10.8 Reliance

- 10.9 Tiamat Energy (Neogy)

- 10.10 Xiamen Tob New Technology Co Ltd