|

시장보고서

상품코드

1892730

EV 배터리 상태 모니터링 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)EV Battery Health Monitoring Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

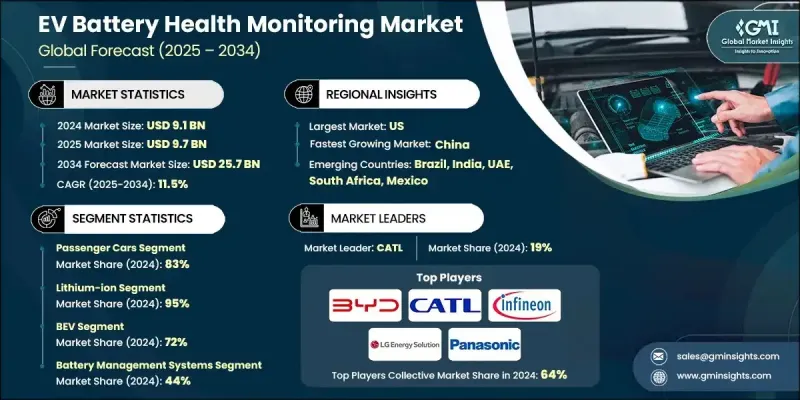

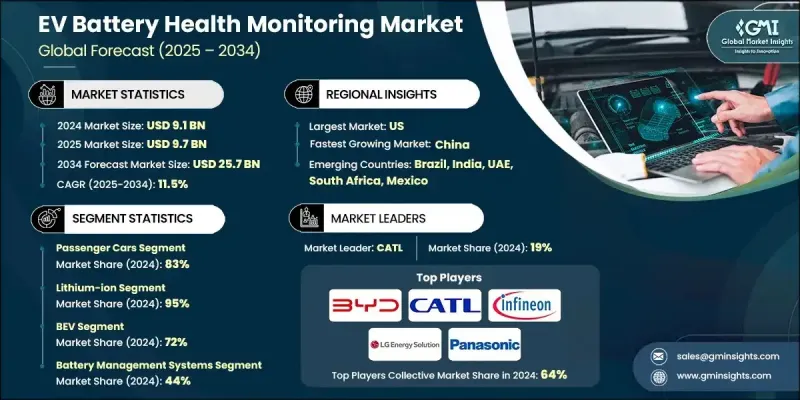

세계의 EV 배터리 상태 모니터링 시장은 2024년 91억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 11.5%를 나타내 257억 달러에 이를 것으로 예측됩니다.

전기자동차의 보급 가속에 따라 정확하고 실시간 배터리 건강 상태 데이터 수요가 급증하고 있습니다. 배터리는 EV 총 비용의 거의 절반을 차지하기 때문에 OEM 제조업체와 플릿 운영자는 보증 청구 감소, 운영 안전성 향상, 소비자 신뢰 강화를 목적으로 충전 상태(SOC) 및 건강 상태(SOH)의 엄격한 감시를 추진하고 있습니다. 첨단 배터리 모니터링 시스템은 고장 예측, 충전 패턴 최적화, 열 문제 방지를 위해 예지 보전, 인공지능, 머신러닝 통합을 추진하고 있습니다. 이러한 기술 혁신은 다운타임 최소화, 배터리 수명 연장, 함대의 신뢰성 향상을 실현합니다. 소프트웨어로 정의된 배터리 플랫폼이 증가함에 따라 효율적인 배터리 관리를 위해서는 예측 분석과 디지털 트윈이 필수적입니다. 또한, 배터리 안전 및 재활용에 관한 정부 규정 및 수명 주기 투명성 요구 사항은 전 세계의 고급 진단 및 모니터링 솔루션의 도입을 촉진하고 예측 기간 동안 견조한 시장 성장을 지원합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 가치 | 91억 달러 |

| 예측 금액 | 257억 달러 |

| CAGR | 11.5% |

승용차 부문은 2024년에 83%의 점유율을 차지했고 2025년부터 2034년에 걸쳐 CAGR 11%를 나타낼 것으로 예측됩니다. 승용차에서 전기자동차(EV)의 보급 확대가 정확하고 실시간 배터리 데이터에 대한 수요를 촉진하고 있습니다. 보증 기간의 장기화, 안전성 향상, 예측 가능한 성능으로 제조업체는 정교한 상태 평가(SOH) 및 충전 상태(SOC) 알고리즘의 통합을 강요받아 소비자의 신뢰를 높이고 모델 간의 차별화를 도모하고 있습니다.

리튬 이온 배터리 부문은 2024년에 95%의 점유율을 차지했으며, 2025년부터 2034년에 걸쳐 CAGR 11.5%를 나타낼 것으로 예상됩니다. EV의 광범위한 사용은 주요 성능 지표 모니터링의 필요성을 강조합니다. 높은 에너지 밀도, 온도 변동에 대한 민감성, 전압 불균형, 빈번한 충전 사이클은 다양한 주행 조건 하에서 균일한 성능을 유지하고, 안전성을 확보하고, 배터리 수명을 연장하는 고급 진단 기술을 필요로 합니다.

미국의 EV 배터리 상태 모니터링 시장은 2024년 86%의 점유율을 차지했으며 31억 달러 시장 규모를 창출했습니다. 정부 인센티브, 세제 우대 조치, 청정 모빌리티 시책에 뒷받침되는 EV의 보급 확대를 통해 OEM 제조업체 및 플릿 운영자는 안전성 확보, 보증 최적화, 다양한 조건 하에서 신뢰성 높은 장기 운용을 실현하기 위해 첨단 배터리 상태 모니터링 시스템의 도입을 추진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 이익률 분석

- 비용 구조

- 각 단계별 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 커넥티드 EV 플랫폼의 보급 확대

- AI 구동형 배터리 진단으로의 이행

- 배터리 안전 규제 및 투명성 확보의 의무

- 전동화 상용 플릿의 성장

- 업계의 잠재적 위험 및 과제

- 고급 감시 하드웨어의 고비용

- 전지 화학 조성 및 설계의 다양성

- 열안전성에 대한 우려사항

- 데이터 보안 및 개인 정보 보호 문제

- 시장 기회

- 2차 생활 및 재활용 시장 확대

- 아시아태평양의 전기자동차 제조 성장

- 충전 인프라 통합

- 플릿용 예지 보전 서비스

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 전망

- 현행 기술

- 고급 배터리 관리 시스템

- 차재 배터리 진단 및 내장 센싱

- 클라우드 접속형 배터리 분석 플랫폼

- 차량 텔레매틱스 및 CAN 버스 기반 데이터 통합

- 신흥 기술

- AI를 활용한 예측형 배터리 건강 상태 및 잔존 수명(RUL) 모델링

- 디지털 트윈에 의한 배터리 모델링

- 블록체인을 활용한 배터리 추적 가능성과 라이프사이클 무결성

- 5G 대응 저지연 배터리 텔레메트리 및 V2X 통합

- 현행 기술

- 특허 분석

- 생산 통계

- 생산 거점

- 소비 허브

- 수출과 수입

- 가격 동향

- 지역별

- 배터리별

- 가격 분석과 비용 구조

- BMS 하드웨어 비용 내역

- 소프트웨어 라이선싱 및 구독 모델

- 차량 운영사용 총 소유 비용

- 가격 하락 동향과 상품화 위험

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 제조 공정에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 배터리 화학의 다양성과 모니터링의 복잡성

- 리튬 이온 전지의 화학 조성 변형

- 고체 전지 모니터링의 과제

- 열 관리 및 열폭주 방지 아키텍처

- 열폭주 메커니즘과 감지 단계

- 멀티 포인트 온도 감지 전략

- 열 전파 모니터링 및 조기 경보 시스템

- 능동적 vs. 수동적 열 관리 통합

- V2G 통합 및 배터리 소모량 관리

- ISO 15118-20 양방향 전력 전송 프로토콜

- V2G 운용에 있어서 배터리의 열화 메커니즘

- V2G 전용 SOH 추적·보고

- 그리드 서비스 최적화 알고리즘

- 세컨드 라이프 전지의 평가와 순환형 경제의 실행 가능성

- 초수명 종료 기준 및 건전성 임계치

- 세컨드 라이프 용도 적합성 분석

- 세컨드 라이프 인증을 위한 건전성 모니터링

- 함대 텔레매틱스 통합 및 총소유비용 최적화

- 플릿 관리 플랫폼의 아키텍처

- 함대 총 소유 비용 절감을 위한 배터리 건전성 모니터링

- 여러 차량의 배터리 건강 상태의 벤치 마크

- 플릿 전동화의 ROI 모델링

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병

- 파트너십 및 협력

- 신제품 출시

- 사업 확대 계획과 자금 조달

제5장 시장 추계·예측 : 배터리별(2021-2034년)

- 주요 동향

- 리튬 이온

- 납산

- 니켈 메탈 하이드라이드

- 기타

제6장 시장 추계·예측 : 추진력별(2021-2034년)

- 주요 동향

- BEV

- PHEV

- HEV

제7장 시장 추계·예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형차

- 중형차

- 대형차

제8장 시장 추계·예측 : 기술별(2021-2034년)

- 주요 동향

- 배터리 관리 시스템

- 모니터링 및 진단

- AI/머신러닝 및 클라우드 기반 분석

- 차량 관리 시스템 및 원격 모니터링

- 애프터마켓 진단 솔루션

- 기타

제9장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 차량 초기 운영

- 차량 관리

- 충전 인프라 통합

- 차량-그리드 서비스

- 기타

제10장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 자동차 제조업체

- 차량 운영사

- 배터리 제조업체 및 공급업체

- 충전 인프라 제공업체

- 애프터마켓 서비스 제공업체

- 기타

제11장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ANZ

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 프로파일

- 세계 기업

- Continental

- LG Energy Solution

- Panasonic

- CATL

- BYD

- Analog Devices

- 삼성SDI

- Texas Instruments

- Infineon

- LEM International

- 지역 기업

- Samsara

- Geotab

- NXP Semiconductors

- Denso

- Valeo

- Renesas Electronics

- STMicroelectronics

- 신흥 기업

- Qnovo

- Teltonika

- Twaice Technologies

- Breathe Battery Technologies

- Voltaiq

- Brill Power

The Global EV Battery Health Monitoring Market was valued at USD 9.1 billion in 2024 and is estimated to grow at a CAGR of 11.5% to reach USD 25.7 billion by 2034.

The accelerating adoption of electric vehicles has created a critical demand for accurate, real-time battery health data. Batteries account for nearly half of an EV's total cost, prompting OEMs and fleet operators to closely monitor state-of-charge (SOC) and state-of-health (SOH) to reduce warranty claims, enhance operational safety, and strengthen consumer confidence. Advanced battery monitoring systems are increasingly incorporating predictive maintenance, artificial intelligence, and machine learning to anticipate failures, optimize charging patterns, and prevent thermal issues. These innovations minimize downtime, extend battery longevity, and improve fleet reliability. With the rise of software-defined battery platforms, predictive analytics, and digital twins are becoming essential for efficient battery management. Government regulations and lifecycle transparency requirements for battery safety and recycling further drive the deployment of sophisticated diagnostic and monitoring solutions worldwide, supporting robust market growth over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.1 Billion |

| Forecast Value | $25.7 Billion |

| CAGR | 11.5% |

The passenger car segment held an 83% share in 2024 and is expected to grow at a CAGR of 11% from 2025 to 2034. Increasing EV adoption in passenger vehicles is fueling the demand for precise, real-time battery data. Longer warranty terms, improved safety, and predictable performance compel manufacturers to integrate advanced SOH and SOC algorithms, enhancing consumer trust and differentiating models.

The lithium-ion batteries segment held a 95% share in 2024, expected to grow at a CAGR of 11.5% from 2025 to 2034. Their widespread use in EVs underscores the necessity of monitoring key performance metrics. High energy density, sensitivity to temperature fluctuations, voltage imbalance, and frequent charge cycles require sophisticated diagnostics to maintain uniform performance, ensure safety, and extend battery life under diverse driving conditions.

US EV Battery Health Monitoring Market held an 86% share, generating USD 3.1 billion in 2024. Strong EV adoption supported by government incentives, tax benefits, and clean mobility initiatives has driven OEMs and fleet operators to seek advanced battery health management systems for safety, warranty optimization, and reliable long-term operation across varying conditions.

Major players in the EV Battery Health Monitoring Market include LG Energy Solution, Analog Devices, BYD, CATL, Continental, Infineon, LEM International, Panasonic, Samsung SDI, and Texas Instruments. Market leaders in EV battery health monitoring are focusing on developing advanced chipsets and sensor solutions to enhance real-time monitoring capabilities. Companies are investing heavily in AI-driven predictive maintenance platforms and machine learning algorithms to anticipate failures, optimize charging cycles, and improve safety. Strategic partnerships with EV manufacturers and fleet operators ensure widespread integration of monitoring systems. Firms are also expanding their global distribution networks and local service capabilities to support diverse regional requirements. Continuous research and development efforts are driving innovation in software-defined battery management and digital twin technologies. Regulatory compliance, product customization, and technology differentiation remain central to maintaining competitive advantage and securing long-term market presence.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Battery

- 2.2.3 Technology

- 2.2.4 Propulsion

- 2.2.5 Vehicle

- 2.2.6 Application

- 2.2.7 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of connected EV platforms

- 3.2.1.2 Shift toward AI-driven battery diagnostics

- 3.2.1.3 Battery safety regulations and transparency mandates

- 3.2.1.4 Growth of electrified commercial fleets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced monitoring hardware

- 3.2.2.2 Variability in battery chemistries and designs

- 3.2.2.3 Thermal safety concerns

- 3.2.2.4 Data security and privacy issues

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of second-life and recycling markets

- 3.2.3.2 Growth in APAC EV manufacturing

- 3.2.3.3 Charging infrastructure integration

- 3.2.3.4 Predictive maintenance services for fleets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current Technologies

- 3.7.1.1 Advanced battery management systems

- 3.7.1.2 On-board battery diagnostics & embedded sensing

- 3.7.1.3 Cloud-connected battery analytics platforms

- 3.7.1.4 Vehicle telematics & can-based data integration

- 3.7.2 Emerging Technologies

- 3.7.2.1 AI-powered predictive battery health & RUL modeling

- 3.7.2.2 Digital twin battery modeling

- 3.7.2.3 Blockchain-Enabled Battery Traceability & Lifecycle Integrity

- 3.7.2.4 5G-enabled low-latency battery telemetry & V2X integration

- 3.7.1 Current Technologies

- 3.8 Patent analysis

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By battery

- 3.11 Pricing analysis & cost structure

- 3.11.1 BMS hardware cost breakdown

- 3.11.2 Software licensing & subscription models

- 3.11.3 Total cost of ownership for fleet operators

- 3.11.4 Price erosion trends & commoditization risk

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Battery chemistry diversity & monitoring complexity

- 3.13.1 Lithium-ion chemistry variants

- 3.13.2 Solid-state battery monitoring challenges

- 3.14 Thermal management & thermal runaway prevention architecture

- 3.14.1 Thermal runaway mechanism & detection stages

- 3.14.2 Multi-point temperature sensing strategies

- 3.14.3 Thermal propagation monitoring & early warning systems

- 3.14.4 Active vs. Passive thermal management integration

- 3.15 V2G integration & battery wear accounting

- 3.15.1 ISO 15118-20 bidirectional power transfer protocol

- 3.15.2. Battery degradation mechanisms in V2 G operation

- 3.15.3. V2 G-specific SOH tracking & reporting

- 3.15.4 Grid service optimization algorithms

- 3.16 Second-life battery assessment & circular economy viability

- 3.16.1 End-of-first-life criteria & health thresholds

- 3.16.2 Second-life application suitability analysis

- 3.16.3 Health monitoring for second-life certification

- 3.17 Fleet telematics integration & total cost of ownership optimization

- 3.17.1 Fleet management platform architecture

- 3.17.2 Battery health monitoring for fleet tco reduction

- 3.17.3 Multi-vehicle battery health benchmarking

- 3.17.4 Fleet electrification roi modeling

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Battery, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Lithium-ion

- 5.3 Lead-acid

- 5.4 NiMH

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 BEV

- 6.3 PHEV

- 6.4 HEV

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger car

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 Light duty

- 7.3.2 Medium duty

- 7.3.3 Heavy duty

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Battery management systems

- 8.3 Monitoring & diagnostic

- 8.4 AI/ML & cloud-based analytics

- 8.5 Fleet telematics & remote monitoring

- 8.6 Aftermarket diagnostic solutions

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 First-life vehicle operation

- 9.3 Fleet management

- 9.4 Charging infrastructure integration

- 9.5 Vehicle-to-grid services

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Automotive OEMs

- 10.3 Fleet operators

- 10.4 Battery manufacturers & suppliers

- 10.5 Charging infrastructure providers

- 10.6 Aftermarket service providers

- 10.7 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global players

- 12.1.1 Continental

- 12.1.2 LG Energy Solution

- 12.1.3 Panasonic

- 12.1.4 CATL

- 12.1.5 BYD

- 12.1.6 Analog Devices

- 12.1.7 Samsung SDI

- 12.1.8 Texas Instruments

- 12.1.9 Infineon

- 12.1.10 LEM International

- 12.2 Regional players

- 12.2.1 Samsara

- 12.2.2 Geotab

- 12.2.3 NXP Semiconductors

- 12.2.4 Denso

- 12.2.5 Valeo

- 12.2.6 Renesas Electronics

- 12.2.7 STMicroelectronics

- 12.3 Emerging Players:

- 12.3.1 Qnovo

- 12.3.2 Teltonika

- 12.3.3 Twaice Technologies

- 12.3.4 Breathe Battery Technologies

- 12.3.5 Voltaiq

- 12.3.6 Brill Power