|

시장보고서

상품코드

1892785

금속 분말 이용 적층 가공 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Additive Manufacturing With Metal Powders Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

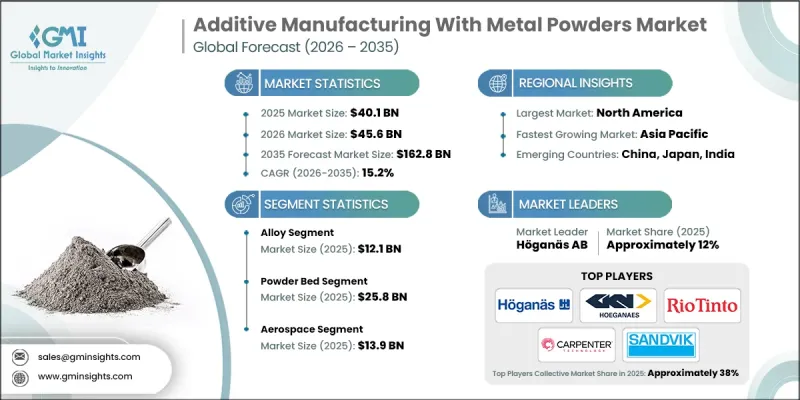

세계의 금속 분말 이용 적층 가공 시장은 2025년에 401억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 15.2%로 성장하여 1,628억 달러에 이를 것으로 예측됩니다.

성능과 연비 향상을 위해 경량화 및 고강도 부품에 대한 산업 수요가 증가함에 따라 시장이 빠르게 확대되고 있습니다. 항공우주, 자동차, 국방 분야에서는 내구성을 유지하면서 복잡한 형상과 경량화를 실현하기 위해 금속 적층조형으로의 전환이 진행되고 있습니다. 레이저 시스템, 전자빔법, 멀티 레이저 장치 등 3D 프린팅 기술의 발전으로 조형 속도의 가속화와 정밀도가 향상되고 있습니다. 분말층 용융 공정의 보급 확대에 따라 공정 신뢰성 향상, 생산 주기 단축, 표면 마감 개선이 실현되어 금속 AM 솔루션의 상용화를 촉진하고 있습니다. 또한, 의료 및 치과 분야에서는 맞춤형 임플란트, 의족, 수술 기구 등에 금속 적층 가공 기술이 적용되어 환자 맞춤형 및 고정밀 용도에 대한 수요가 급증하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 시장 규모 | 401억 달러 |

| 예측 금액 | 1,628억 달러 |

| CAGR | 15.2% |

합금 부문은 2025년 121억 달러 시장 규모를 형성할 것으로 예상되며, 2035년까지 연평균 15.5%의 성장률을 보일 것으로 전망됩니다. 스테인리스 스틸을 포함한 합금은 내식성, 기계적 강도, 복잡한 형상에 대한 적응성 때문에 널리 사용되고 있습니다. 항공우주, 자동차, 의료, 산업 장비 분야에서의 폭넓은 채용으로 지속적인 수요를 창출하고 있습니다. 기타 강재들은 구조물 및 공구 분야에서 비용 효율적인 솔루션을 제공하여 제조업체가 시제품 제작부터 대량 생산까지 효율적으로 규모를 확장할 수 있도록 지원합니다.

항공우주 분야는 2025년 139억 달러(점유율 34.7%)를 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 14.9%의 성장률을 보일 것으로 전망됩니다. 항공우주, 자동차, 의료 산업은 고성능, 경량, 정밀 부품에 대한 수요를 주도하고 있습니다. 항공우주 기업은 첨단 구조 부품과 엔진 부품을 필요로 하고, 자동차 제조업체는 금형, 시제품, 소량 생산의 고성능 부품에 금속 AM을 활용하고 있습니다. 환자맞춤형 임플란트 및 수술기구의 보급과 함께 의료용도가 빠르게 확대되고 있습니다. 이러한 산업의 융합이 고정밀 금속 적층 가공에 대한 추세를 강화하고 있습니다.

북미의 금속 분말 이용 적층 가공 시장은 2025년 138억 달러 규모에 달할 것으로 예측됩니다. 가볍고 정밀한 부품에 대한 수요 증가에 따라 항공우주, 국방, 의료 분야에서 금속 적층조형의 채용이 증가하고 있습니다. 첨단 디지털 제조 기술, 탄탄한 인프라, 지속적인 연구개발 투자가 상용화를 뒷받침하고 있습니다. 시제품, 금형, 특수 부품에 대한 활용 확대와 더불어 하이브리드 및 자동화 공정의 도입이 이 지역 시장의 성장을 주도하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 향후 시장 동향

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 특허 상황

- 무역 통계(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경적 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국에 관한 고려사항

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추산 및 예측 : 재료별, 2022-2035

- 주요 동향

- 합금

- 티타늄

- 티타늄 합금(Ti6Al4V)

- Ti6Al4V(ELI)

- 기타

- 코발트

- CoCr

- CoCrWC

- CoCrMo

- 구리

- C18150

- CuCr1Zr

- CuNi2SiCr

- 니켈

- Inconel 625

- Inconel 718

- Hastelloy X

- 알루미늄

- ALSi12

- ALSi7Mg

- ALSi10Mg

- AL6061

- 기타

- 티타늄

- 스테인리스 스틸

- Austenitic Steel

- Martensitic Steel

- Duplex steel

- Ferritic Steel

- 기타 강재

- 고속도강

- 공구강

- 저합금망

- 귀금속

- 플래티넘

- 기타 귀금속

- 텅스텐

- 기타 재료

- 탄화규소

- 알루미나 분말

- 지르코늄

- 이산화 지르코늄

- 몰리브덴

- 마그네슘

- 질화 알루미늄

- 텅스텐 카바이드

제6장 시장 추산 및 예측 : 제조 기술별, 2022-2035

- 주요 동향

- 분말마루 방식

- Direct Metal Laser Sintering (DMLS)

- Selective Laser Melting (SLM)

- Electron Beam Melting (EBM)

- 분말 분사

- Direct Metal Deposition (DMD)

- Laser Engineering Net Shapes (LENS)

- 기타

제7장 시장 추산 및 예측 : 용도별, 2022-2035

- 주요 동향

- 항공우주

- 자동차

- 의료 분야

- 석유 및 가스

- 에너지

- 원자력

- 재생에너지

- 기타

제8장 시장 추산 및 예측 : 지역별, 2022-2035

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 개요

- Hoganas AB

- GKN Powder Metallurgy(Hoeganaes)

- Rio Tinto

- Carpenter Technology Corporation

- Sandvik Additive Manufacturing

- LPW Technology

- AP&C(Advanced Powders &Coatings)

- Arcam AB

- EOS GmbH

- Bright Laser Technologies

- Huake 3D

- ReaLizer

The Global Additive Manufacturing With Metal Powders Market was valued at USD 40.1 billion in 2025 and is estimated to grow at a CAGR of 15.2% to reach USD 162.8 billion by 2035.

The market is expanding rapidly as industries increasingly demand lightweight, high-strength components to enhance performance and fuel efficiency. Aerospace, automotive, and defense sectors are transitioning to metal additive manufacturing to achieve complex geometries and weight reduction without compromising durability. Advances in 3D printing technologies, including laser systems, electron-beam methods, and multi-laser setups, are accelerating build speed and improving precision. Wider adoption of powder-bed fusion processes has enhanced process reliability, shortened production cycles, and improved surface finishes, driving the commercialization of metal AM solutions. Additionally, the medical and dental sectors are fueling growth by adopting metal additive manufacturing for customized implants, prosthetics, and surgical instruments, creating a surge in demand for patient-specific and high-precision applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $40.1 Billion |

| Forecast Value | $162.8 Billion |

| CAGR | 15.2% |

The alloy segment generated USD 12.1 billion in 2025 and is expected to grow at a CAGR of 15.5% through 2035. Alloys, including stainless steel, are widely used due to their corrosion resistance, mechanical strength, and suitability for complex geometries. Their broad adoption across aerospace, automotive, medical, and industrial equipment sectors is creating sustainable demand. Other types of steel provide cost-effective solutions for structural and tooling applications, allowing manufacturers to scale both prototyping and functional production efficiently.

The aerospace segment accounted for USD 13.9 billion in 2025, holding a 34.7% share, and is anticipated to grow at a CAGR of 14.9% during 2026-2035. Aerospace, automotive, and medical industries are driving demand for high-performance, lightweight, and precision components. Aerospace companies require advanced structural and engine parts, while automotive manufacturers use metal AM for tooling, prototyping, and limited-volume high-performance components. Medical applications are expanding rapidly as patient-specific implants and surgical tools gain traction. The convergence of these industries is reinforcing the trend toward high-precision metal additive manufacturing.

North America Additive Manufacturing With Metal Powders Market held USD 13.8 billion in 2025. Adoption of metal AM is rising across aerospace, defense, and medical sectors for lightweight, precise parts. Advanced digital manufacturing, well-established infrastructure, and ongoing R&D investments support commercialization. Growing use in prototyping, tooling, and specialty parts, along with hybrid and automated processes, is driving regional market expansion.

Key players in the Global Additive Manufacturing With Metal Powders Market include Hoganas AB, GKN Powder Metallurgy (Hoeganaes), Rio Tinto, Carpenter Technology Corporation, Sandvik Additive Manufacturing, and others. Companies in the Global Additive Manufacturing With Metal Powders Market are leveraging multiple strategies to strengthen their market presence. They are investing heavily in research and development to enhance printing speed, accuracy, and material compatibility. Strategic collaborations, joint ventures, and acquisitions are expanding product portfolios and geographic reach. Companies are introducing new alloy compositions and customizing solutions for aerospace, automotive, and medical applications. Adoption of digital and hybrid manufacturing systems, alongside automated post-processing and quality control solutions, helps streamline production and reduce costs. Additionally, firms are emphasizing customer training, technical support, and service networks to improve adoption rates, establish long-term partnerships, and maintain competitive advantage in a rapidly evolving industry.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Manufacturing Technique

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Alloy

- 5.2.1 Titanium

- 5.2.1.1 Ti6Al4V

- 5.2.1.2 Ti6Al4V (ELI)

- 5.2.1.3 Others

- 5.2.2 Cobalt

- 5.2.2.1 CoCr

- 5.2.2.2 CoCrWC

- 5.2.2.3 CoCrMo

- 5.2.3 Copper

- 5.2.3.1 C18150

- 5.2.3.2 CuCr1Zr

- 5.2.3.3 CuNi2SiCr

- 5.2.4 Nickel

- 5.2.4.1 Inconel 625

- 5.2.4.2 Inconel 718

- 5.2.4.3 Hastelloy X

- 5.2.5 Aluminium

- 5.2.5.1 ALSi12

- 5.2.5.2 ALSi7Mg

- 5.2.5.3 ALSi10Mg

- 5.2.5.4 AL6061

- 5.2.5.5 Others

- 5.2.1 Titanium

- 5.3 Stainless Steel

- 5.3.1 Austenitic Steel

- 5.3.2 Martensitic Steel

- 5.3.3 Duplex steel

- 5.3.4 Ferritic Steel

- 5.4 Other Steel

- 5.4.1 High Speed Steel

- 5.4.2 Tool Steel

- 5.4.3 Low Alloy Steel

- 5.5 Precious Metal

- 5.5.1 Platinum

- 5.5.2 Other precious metal

- 5.6 Tungsten

- 5.7 Other materials

- 5.7.1 Silicon carbide

- 5.7.2 Aluminium oxide powder

- 5.7.3 Zirconium

- 5.7.4 Zirconium dioxide

- 5.7.5 Molybdenum

- 5.7.6 Magnesium

- 5.7.7 Aluminium nitride

- 5.7.8 Tungsten carbide

Chapter 6 Market Estimates and Forecast, By Manufacturing Technique, 2022 - 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Powder Bed

- 6.2.1 Direct Metal Laser Sintering (DMLS)

- 6.2.2 Selective Laser Melting (SLM)

- 6.2.3 Electron Beam Melting (EBM)

- 6.3 Blown powder

- 6.3.1 Direct Metal Deposition (DMD)

- 6.3.2 Laser Engineering Net Shapes (LENS)

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Aerospace

- 7.3 Automotive

- 7.4 Medical

- 7.5 Oil & Gas

- 7.6 Energy

- 7.6.1 Nuclear

- 7.6.2 Renewable

- 7.7 Other

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Hoganas AB

- 9.2 GKN Powder Metallurgy (Hoeganaes)

- 9.3 Rio Tinto

- 9.4 Carpenter Technology Corporation

- 9.5 Sandvik Additive Manufacturing

- 9.6 LPW Technology

- 9.7 AP&C (Advanced Powders & Coatings)

- 9.8 Arcam AB

- 9.9 EOS GmbH

- 9.10 Bright Laser Technologies

- 9.11 Huake 3D

- 9.12 ReaLizer