|

시장보고서

상품코드

1892796

트럭 베드라이너 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Truck Bedliners Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

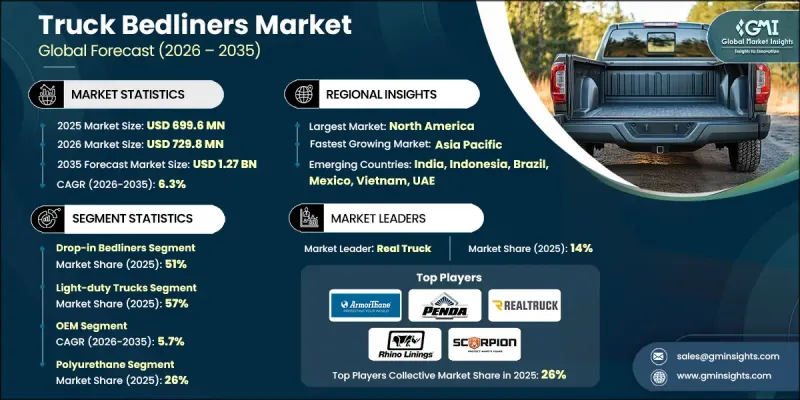

세계의 트럭 베드라이너 시장은 2025년에 6억 9,960만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 6.3%로 성장하여 12억 7,000만 달러에 이를 것으로 예측됩니다.

시장의 성장세는 개인용, 상업용, 레저용을 불문하고 전 세계적으로 픽업트럭이 보급되고 있는 것에 기인합니다. 차량 보유량 증가는 픽업트럭 문화를 더욱 강화시켰고, 이는 직접적으로 화물칸 보호 솔루션에 대한 수요를 증가시켰습니다. 카시트 라이너는 차량의 상태를 유지하고 장기적인 가치 유지를 위한 필수 액세서리로 널리 인식되고 있습니다. OEM 제조업체와 애프터마켓 기업 모두 교체 주기가 길어지고 전체 사용자층에서 커스터마이징으로 꾸준히 전환하는 추세의 혜택을 누리고 있습니다. 소비자들은 픽업트럭을 다기능 자산으로 인식하는 경향이 강해지고 있으며, 내구성, 외관, 실용성을 높이는 액세서리에 대한 지출이 증가하고 있습니다. 화물칸 라이너는 가장 실용적이고 저렴한 업그레이드 중 하나로 널리 받아들여지고 있습니다. 액세서리 소매 네트워크의 확대, DIY의 확산, 제품의 광범위한 가용성, 특히 선진 시장과 급성장하는 도시 지역에서 수요를 더욱 자극하고 있습니다. 상업용 차량 운영업체도 크게 기여하고 있으며, 내구성이 뛰어난 적재함 보호는 차량의 수명을 연장하고 지속적인 유지보수 비용을 절감하여 비용 효율적인 투자로 적재함 라이너의 가치를 높이고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 시장 규모 | 6억 9,960만 달러 |

| 예측 금액 | 12억 7,000만 달러 |

| CAGR | 6.3% |

픽업트럭 오너들은 기능성과 외관을 모두 향상시키기 위해 차량 커스터마이징을 계속하고 있습니다. 베드 라이너는 높은 보호 성능과 가성비로 인해 점점 더 많은 선택을 받고 있습니다. 설치의 용이성과 직접 설치 솔루션에 대한 소비자의 신뢰도가 높아지면서 애프터마켓에서의 보급 확대가 이루어지고 있습니다. 상업용 운영자들은 마모 관련 비용을 절감하기 위해 내구성을 중시하고 있으며, 이는 전체 차량용도에서 안정적인 수요를 뒷받침하고 있습니다.

경트럭 부문은 2025년 57%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 7%로 확대될 것으로 전망됩니다. 이 부문이 선두를 달리고 있는 배경에는 높은 개인 소유율, 액세서리 지출 증가, 커스터마이징 트렌드의 강세, 전기 픽업 모델의 보급 확대 등이 있습니다. 이러한 요인은 대규모 생산 능력과 광범위한 지역에서 일관되게 높은 베드 라이너 장착률로 인해 더욱 강화되었습니다.

OEM 부문은 2026년부터 2035년까지 연평균 5.7%의 성장률을 보일 것으로 예측됩니다. OEM 장착형 베드 라이너는 통합된 착용감, 보증의 무결성, 구매자의 편의성 향상을 제공합니다. 이 부문의 성장은 경트럭 생산량 증가, 프리미엄 공장 장착형 액세서리 제공, 품질 및 규제 기준을 충족하기 위한 공급업체 파트너와의 협력 확대에 힘입어 성장세를 보이고 있습니다.

미국 트럭 베드 라이너 시장은 2025년 2억 6,190만 달러에 달할 것으로 예측됩니다. 미국 내 수요는 가혹한 사용 환경에 적합한 내구성 코팅 솔루션에 대한 선호로 인해 지속적으로 형성되고 있습니다. 이러한 성장은 픽업트럭의 높은 보급률, 차량 맞춤화 증가, 차량 개인화에 대한 소비자의 높은 관심에 힘입어 성장세를 보이고 있습니다. 제조업체들은 성능과 내구성을 유지하면서 공장 출고 시 차량 디자인과 시각적으로 조화를 이루도록 설계된 마감재로 이에 대응하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 비용 구조

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 세계

- 환경 규제

- 배출 규제 요건

- 폐기물 처리 규제

- 노동 안전 위생 기준

- 국제 노동 기관(ILO) 기준

- 자동차 OEM 기준

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 세계

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 폴리우레탄 화학과 배합 설계

- 폴리우레아 화학과 배합 설계

- 하이브리드 시스템 기술

- 용도 기기 기술

- 신기술

- 자기치유 코팅 기술

- 나노테크놀러지 강화 코팅

- 항균 및 항세균 솔루션

- 변색성 및 서모크로믹 마감

- 현재 기술 동향

- 가격 분석

- 전문 설치 가격 결정

- 프리미엄 서비스 가격 결정

- DIY 제품 가격 결정

- 롤 온 키트 가격 분석

- 침대 매트 및 러 가격 결정

- 드롭 인 라이너 가격 결정

- E-Commerce와 소매가격 비교

- OEM 공장 설치 가격

- 생산 통계

- 생산 거점

- 소비 거점

- 수출입

- 비용 내역 분석

- 제조 비용 구조

- 설치·시공 비용

- 유통·채널 비용

- 마케팅 및 판매 비용

- 부문별 수익성 분석

- 비용 최적화 전략

- 특허 분석

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국에 관한 고려사항

- 소비자 행동과 커스터마이즈 동향

- 커스터마이즈 시장 개요

- 색과 마무리 선호도

- 질감·표면 커스터마이즈

- 기능 커스터마이즈

- 인구통계별 퍼스널라이제이션 동향

- 신흥 커스터마이즈 기술

- 지역별 구매 선호도와 사용 패턴

- 상업용과 개인용 부문 구성 비율

- 지역별 사용 패턴 분석

- 사용 빈도와 유지관리

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금조달

제5장 시장 추산 및 예측 : 유형별, 2022-2035

- 주요 동향

- Drop-in bedliners

- Spray-on bedliners

- Bed mats & rugs

- Roll-on/brush-on bedliners

- Hybrid/custom-fitted bedliners

제6장 시장 추산 및 예측 : 재료별, 2022-2035

- 주요 동향

- 폴리우레탄

- 폴리우레아

- 고무

- 복합재료/폴리에틸렌

- 에폭시 수지계 배합제

제7장 시장 추산 및 예측 : 차량별, 2022-2035

- 주요 동향

- 소형 트럭

- 중형 트럭

- 대형 트럭

제8장 시장 추산 및 예측 : 판매채널별, 2022-2035

- 주요 동향

- OEM

- 애프터마켓

- 온라인 소매

- 판매점

제9장 시장 추산 및 예측 : 최종 용도별, 2022-2035

- 주요 동향

- 자동차

- 군 및 방위 분야

- 에너지(석유, 가스, 광업)

- 건설

- 농업

- 소매업 및 전자상거래

- 기타

- 애프터마켓

제10장 시장 추산 및 예측 : 지역별, 2022-2035

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 폴란드

- 루마니아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ANZ

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 개요

- Global companies

- ArmorThane

- BASF

- Dee Zee

- DualLiner

- Husky Liners

- LINE-X

- PPG Industries

- Rhino Linings

- Rugged Liner

- Ultimate Linings

- U-POL(RAPTOR)

- WeatherTech

- 지역 제조업체

- Aeroklas

- Armadillo Liners

- BedRug

- Bullet Liner

- Lund International

- OKULEN

- Penda Corporation

- Scorpion Protective Coatings

- SPEEDLINER

- Tuff Liner

- Vortex Liners

- 신흥 제조업체

- AL’s Liner

- Durabak

- Herculiner

- Iron Armor

- POR-15

The Global Truck Bedliners Market was valued at USD 699.6 million in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 1.27 billion by 2035.

Market momentum is driven by the rising global adoption of pickup trucks across personal, commercial, and recreational use. Increasing vehicle ownership continues to strengthen pickup truck culture, which directly fuels demand for protective cargo bed solutions. Bedliners are widely viewed as essential accessories that help preserve vehicle condition while supporting long-term value retention. Both OEM and aftermarket participants benefit from longer replacement timelines and a steady shift toward customization across user segments. Consumers increasingly view pickup trucks as multifunctional assets, prompting higher spending on accessories that enhance durability, appearance, and usability. Bedliners remain among the most practical and affordable upgrades, supporting their widespread acceptance. Growth in accessory retail networks, expanding do-it-yourself adoption, and broader product availability further stimulate demand, particularly in developed markets and fast-growing urban regions. Commercial fleet operators also contribute significantly, as durable bed protection helps extend vehicle service life and reduce ongoing maintenance expenses, reinforcing bedliners as a cost-efficient investment.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $699.6 Million |

| Forecast Value | $1.27 Billion |

| CAGR | 6.3% |

Pickup owners continue to personalize their vehicles to improve both functionality and visual appeal. Bedliners are increasingly selected for their protective performance and value proposition. Easier installation options and growing consumer confidence in self-installation solutions support rising aftermarket penetration. Commercial operators prioritize durability to limit wear-related expenses, reinforcing steady demand across fleet applications.

The light-duty truck segment accounted for a 57% share in 2025 and is projected to grow at a CAGR of 7% between 2026 and 2035. This segment leads due to higher personal ownership rates, increased spending on accessories, strong customization trends, and the growing presence of electric pickup models. These factors are reinforced by large-scale production capabilities and consistently high bedliner attachment rates across a broad geographic footprint.

The OEM segment is expected to grow at a CAGR of 5.7% from 2026 to 2035. OEM-installed bedliners offer integrated fitment, warranty alignment, and added convenience for buyers. Segment growth is supported by rising light truck production volumes, premium factory-installed accessory offerings, and expanding collaboration with supplier partners to meet quality and regulatory standards.

US Truck Bedliners Market reached USD 261.9 million in 2025. Demand in the US continues to be shaped by preferences for durable coating solutions suited for intensive use. Growth is supported by high adoption of pickup trucks, increased fleet customization, and strong consumer focus on vehicle personalization. Manufacturers are responding with finishes designed to align visually with factory vehicle designs while maintaining performance durability.

Key companies active in the Global Truck Bedliners Market include LINE-X, WeatherTech, Rhino Linings, DualLiner, Truck Hero (BedRug), Rugged Liner, Penda Corporation (Pendaliner), Ultimate Linings, SPEEDLINER (Industrial Polymers), and Scorpion Protective Coatings. Companies in the Global Truck Bedliners Market strengthen their competitive position through product innovation, expanded distribution networks, and strategic partnerships. Manufacturers invest in advanced materials to improve durability, appearance, and environmental performance. Many players focus on expanding OEM relationships to secure factory-fitment opportunities while also enhancing aftermarket reach through specialized retailers and installer networks. Brand differentiation is reinforced through customization options, improved installation efficiency, and consistent product quality. Geographic expansion into high-growth regions supports volume gains, while marketing strategies emphasize durability, long-term cost savings, and vehicle value preservation. Continuous investment in manufacturing efficiency and customer support further helps companies defend market share and build long-term brand loyalty.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Material

- 2.2.4 Vehicle

- 2.2.5 Sales channel

- 2.2.6 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pickup truck sales

- 3.2.1.2 Growth in aftermarket customization

- 3.2.1.3 Increasing demand for vehicle protection

- 3.2.1.4 Advancements in spray-on coating materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatile raw material costs

- 3.2.2.2 Competition from low-cost alternatives

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging pickup markets

- 3.2.3.2 OEM partnership integration

- 3.2.3.3 Development of eco-friendly coatings

- 3.2.3.4 Growth in commercial fleet upfitting

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Global

- 3.4.1.1 Environmental regulations

- 3.4.1.2 Emissions control requirements

- 3.4.1.3 Waste disposal regulations

- 3.4.1.4 Occupational health & safety standards

- 3.4.1.5 International labor organization standards

- 3.4.1.6 Automotive OEM standards

- 3.4.2 North America

- 3.4.3 Europe

- 3.4.4 Asia Pacific

- 3.4.5 Latin America

- 3.4.6 Middle East & Africa

- 3.4.1 Global

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Polyurethane chemistry & formulations

- 3.7.1.2 Polyurea chemistry & formulations

- 3.7.1.3 Hybrid system technologies

- 3.7.1.4 Application equipment technology

- 3.7.2 Emerging technologies

- 3.7.2.1 Self-healing coating technologies

- 3.7.2.2 Nano-technology enhanced coatings

- 3.7.2.3 Antimicrobial & antibacterial solutions

- 3.7.2.4 Color-changing & thermochromic finishes

- 3.7.1 Current technological trends

- 3.8 Pricing analysis

- 3.8.1.1 Professional installation pricing

- 3.8.1.2 Premium service pricing

- 3.8.1.3 DIY product pricing

- 3.8.1.4 Roll-on kit pricing analysis

- 3.8.1.5 Bed mat & rug pricing

- 3.8.1.6 Drop-in liner pricing

- 3.8.1.7 E-commerce vs retail pricing

- 3.8.1.8 OEM factory-install pricing

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.10.1 Manufacturing cost structure

- 3.10.2 Application & installation costs

- 3.10.3 Distribution & channel costs

- 3.10.4 Marketing & sales costs

- 3.10.5 Profitability analysis by segment

- 3.10.6 Cost optimization strategies

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Consumer behavior and customization trends

- 3.13.1 Customization market overview

- 3.13.2 Color & finish preferences

- 3.13.3 Texture & surface customization

- 3.13.4 Functional customization

- 3.13.5 Personalization trends by demographics

- 3.13.6 Emerging customization technologies

- 3.14 Regional purchasing preferences & usage patterns

- 3.14.1 Commercial vs personal segment mix

- 3.14.2 Usage pattern analysis by region

- 3.14.3 Application frequency & maintenance

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Drop-in bedliners

- 5.3 Spray-on bedliners

- 5.4 Bed mats & rugs

- 5.5 Roll-on/brush-on bedliners

- 5.6 Hybrid/custom-fitted bedliners

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Polyurethane

- 6.3 Polyurea

- 6.4 Rubber

- 6.5 Composite/polyethylene

- 6.6 Epoxy-based formulations

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Light-duty trucks

- 7.3 Medium-duty trucks

- 7.4 Heavy-duty trucks

Chapter 8 Market Estimates & Forecast, By Sales channel, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

- 8.4 Online Retail

- 8.5 Dealerships

Chapter 9 Market Estimates & Forecast, By End use, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Automotive

- 9.3 Military & defense

- 9.4 Energy (Oil, Gas, & Mining)

- 9.5 Construction

- 9.6 Agriculture

- 9.7 Retail & e-commerce

- 9.8 Others

- 9.9 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 ArmorThane

- 11.1.2 BASF

- 11.1.3 Dee Zee

- 11.1.4 DualLiner

- 11.1.5 Husky Liners

- 11.1.6 LINE-X

- 11.1.7 PPG Industries

- 11.1.8 Rhino Linings

- 11.1.9 Rugged Liner

- 11.1.10 Ultimate Linings

- 11.1.11 U-POL (RAPTOR)

- 11.1.12 WeatherTech

- 11.2 Regional players

- 11.2.1 Aeroklas

- 11.2.2 Armadillo Liners

- 11.2.3 BedRug

- 11.2.4 Bullet Liner

- 11.2.5 Lund International

- 11.2.6 OKULEN

- 11.2.7 Penda Corporation

- 11.2.8 Scorpion Protective Coatings

- 11.2.9 SPEEDLINER

- 11.2.10 Tuff Liner

- 11.2.11 Vortex Liners

- 11.3 Emerging players

- 11.3.1 AL’s Liner

- 11.3.2 Durabak

- 11.3.3 Herculiner

- 11.3.4 Iron Armor

- 11.3.5 POR-15