|

시장보고서

상품코드

1892821

운송 관리 시스템 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Transportation Management System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 -2035 |

||||||

세계의 운송 관리 시스템 시장은 2025년에 150억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 10.6%로 성장하여 403억 달러에 이를 것으로 예측됩니다.

전자상거래의 급속한 성장으로 소량 화물 및 LTL(소량 화물)의 취급량이 크게 증가하는 반면, 예상 배송 시간은 단축되고 수동 경로 설정 및 문제 해결은 더 많은 비용이 소요되고 효과가 떨어지고 있습니다. 클라우드 네이티브 플랫폼이 초기 투자를 줄이고 도입 기간을 단축하기 때문에 모든 규모의 조직이 업무 효율화를 위해 운송관리시스템(TMS)을 도입하고 있습니다. 각 벤더들은 예측 도착 시간(ETA) 정확도 향상, 가격 책정 자동화, 용량 활용률 최적화를 위해 마이크로 서비스, 광범위한 API 액세스, 임베디드 AI를 활용한 플랫폼 재설계를 진행하고 있습니다. 그 결과, TMS 플랫폼은 단순한 비용절감 수단이 아닌 안정적이고 확장성 있는 운송 업무를 구축하기 위한 필수 도구로 인식되고 있습니다. 세계 공급망의 상호 연결성과 멀티모달성이 증가함에 따라, 기업들은 운송업체 조정, 문서 디지털화, 컴플라이언스 지원, 국경 간 가시성 향상을 위한 시스템을 필요로 하고 있습니다. TMS 플랫폼은 현재 GPS 데이터, 텔레매틱스, IoT 신호를 통합하고 실시간 추적을 제공하여 물류팀과 최종 고객 모두에게 투명성을 강화합니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 시장 규모 | 150억 달러 |

| 예측 금액 | 403억 달러 |

| CAGR | 10.6% |

솔루션 분야는 2025년 67%의 점유율을 차지할 것으로 예상되며, 2025년부터 2035년까지 연평균 복합 성장률(CAGR) 10%로 성장할 것으로 전망됩니다. 핵심 TMS 플랫폼은 계획, 실행, 경로 설정, 화물 조달, 인보이스 발행, 가시성, 분석을 관리합니다. 워크플로우 자동화와 실시간 인사이트 제공 능력이 높은 도입률을 견인하고 있습니다. 앞으로의 성장은 AI를 활용한 경로 최적화, 예측 분석, IoT 강화를 통한 가시성 확보 등 새로운 기능들이 뒷받침할 것으로 보입니다.

On-Premise 부문은 2025년 61%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 9.2%의 성장률을 보일 것으로 전망됩니다. On-Premise 솔루션은 커스터마이징 및 데이터 관리 요구 사항으로 인해 매출 점유율에서 우위를 유지하고 있지만, 모듈형 플랫폼 도입, 빠른 구현 주기, 사용량 기반 가격 모델을 채택하는 조직이 증가함에 따라 클라우드 도입은 더 빠른 속도로 성장하고 있습니다. 기업들이 규제 요건과 최신 분석 및 워크플로우 자동화의 균형을 맞추기 위해 하이브리드 아키텍처가 주목받고 있습니다.

미국 운송관리시스템(TMS) 시장은 2025년 52억 달러 규모에 달했습니다. 복잡한 국내 화물 운송 환경과 서비스 품질 향상에 대한 압력이 높아지는 가운데, 중국은 AI 기반 클라우드 기반 TMS 플랫폼 도입에 있어 선도적인 위치를 유지하고 있습니다. 도로, 화물, 소량 배송, 라스트마일 배송을 아우르는 운송 네트워크가 인력 부족과 수요 변동에 직면하면서 예측 계획 도구, 자동화, 실시간 데이터 통합이 필수적입니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 정보원

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 비용 구조

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- FMCSA 전자 기록 장치(ELD) 의무화

- 운전 시간 규제(HOS)

- DOT 안전 규제(CFR 제300-399부)

- 유럽

- 출하 데이터 GDPR(EU 개인정보보호규정) 준거

- C-ITS(협조형 지능형 교통시스템)

- 국경을 넘은 운송 규제

- 아시아태평양

- 중국의 ITS 투자와 표준 규격

- 인도 GST(물품서비스세)가 물류에 미치는 영향

- ASEAN 역내 국경간 운송 원활화

- 라틴아메리카

- 중동 및 아프리카

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 가격 분석

- SaaS 구독 가격 모델

- 영구 라이선스 가격 결정

- 트랜잭션 기반 가격 결정(출하 단위)

- 사용자 기반 가격 모델

- 비용 내역 분석

- 특허 분석

- TMS 기술에 관한 미국 특허 상표청(USPTO) 특허 분류

- 주요 특허 보유 기업과 혁신 리더

- 신흥 특허 동향(AI, 블록체인, IoT)

- 지속가능성과 환경 측면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국에 관한 고려사항

- 이용 사례

- 기능 채택 비율과 이용 상황 분석

- 코어 기능 도입률

- 첨단기능 도입률

- 신흥 기능 도입률

- 업계별 기능 채택 상황

- 이동 패턴과 변환 동향

- TMS 이동 촉진요인

- 도입 형태별 이동 패턴

- 벤더 변환 동향

- 이동 스케줄과 복잡성

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- LATAM

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협력 관계

- 신제품 발매

- 사업 확대 계획과 자금조달

- TMS 스타트업 기업에의 벤처캐피털 투자

- 물류 기술 분야 프라이빗 에퀴티 활동

- 정부에 의한 인프라 투자(세계 은행 ITS 보고서)

- 주요 벤더의 기업 연구개발비

- 벤더 선정 기준

- 시장 진출 전략

제5장 시장 추산 및 예측 : 플랫폼별, 2021-2034

- 주요 동향

- 솔루션

- 출하 계획

- 주문 관리

- 감사 및 지불 업무

- 분석 및 보고서

- 배송 추적 서비스

- 기타

- 서비스

- 컨설팅

- 도입 및 통합

- 지원 및 유지보수

제6장 시장 추산 및 예측 : 운송 수단별, 2021-2034

- 주요 동향

- 도로 운송

- 철도

- 항공 수송

- 수로

제7장 시장 추산 및 예측 : 도입 모델별, 2021-2034

- 주요 동향

- On-Premise

- 클라우드

제8장 시장 추산 및 예측 : 기업 규모별, 2021-2034

- 주요 동향

- 대기업

- 중소기업

제9장 시장 추산 및 예측 : 업종별, 2021-2034

- 주요 동향

- 소매업 및 전자상거래

- 의료 및 의약품

- 유통 및 물류

- 제조업

- 정부

- 기타

제10장 시장 추산 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 폴란드

- 루마니아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ANZ

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 개요

- Global companies

- Blue Yonder

- C.H. Robinson

- Descartes

- E2 open

- Infor

- Manhattan Associates

- Oracle

- SAP

- Trimble

- Wise Tech Global

- 지역 기업

- 11.2.1. Gtms

- Alpega

- Blujay Solutions

- CTSI-Global

- Korber

- Kuebix

- Logility

- MercuryGate

- Shippeo

- Transporeon

- 신규 기업

- Arrive Logistics

- FourKites

- Loadsmart

- Locus

- Motive

- Parade

- project44

- Samsara

- Shipsy

- Transfix

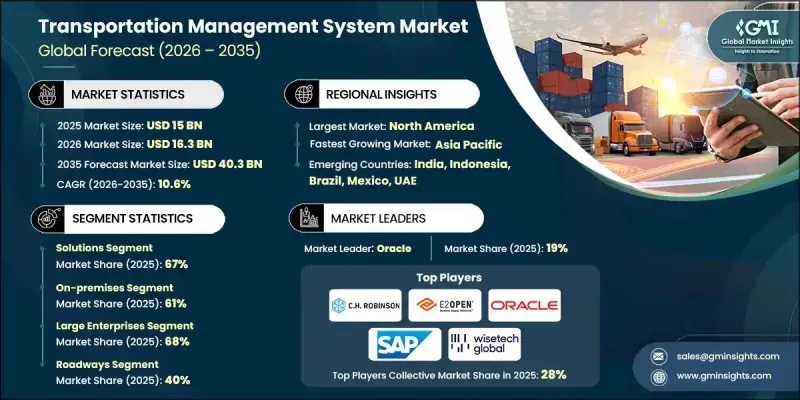

The Global Transportation Management System Market was valued at USD 15 billion in 2025 and is estimated to grow at a CAGR of 10.6% to reach USD 40.3 billion by 2035.

Rapid growth in e-commerce has significantly increased parcel and LTL activity while shortening delivery expectations, making manual routing and issue resolution more expensive and less effective. As cloud-native platforms reduce upfront investment and shorten deployment timelines, organizations of all sizes are turning to Transportation Management Systems to streamline operations. Vendors are redesigning their platforms with microservices, broader API access, and embedded AI to improve predictive ETAs, automate pricing, and optimize capacity utilization. As a result, TMS platforms are now viewed as essential tools for building reliable, scalable transportation operations rather than solely an avenue for cost reduction. With global supply chains growing more interconnected and multimodal, businesses need systems that coordinate carriers, digitize documentation, support compliance, and enhance cross-border visibility. TMS platforms now combine GPS data, telematics, and IoT signals to offer real-time tracking, strengthening transparency for both logistics teams and end customers.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $15 Billion |

| Forecast Value | $40.3 Billion |

| CAGR | 10.6% |

The solutions segment held a 67% share in 2025 and is expected to grow at a CAGR of 10% from 2025 to 2035. Core TMS platforms manage planning, execution, routing, freight sourcing, invoicing, visibility, and analytics. Their ability to automate workflows and deliver real-time insights drives their strong adoption curve. Future growth will be supported by emerging capabilities such as AI-enabled route optimization, predictive analytics, and IoT-enhanced visibility.

The on-premises segment held a 61% share in 2025 and is projected to grow at a CAGR of 9.2% through 2035. While on-premises solutions maintain a larger revenue share due to customization and data control requirements, cloud deployments continue to grow more quickly as organizations adopt modular platforms, faster implementation cycles, and usage-based pricing models. Hybrid architectures are gaining traction as companies balance regulatory needs with modern analytics and workflow automation.

US Transportation Management System Market generated USD 5.2 billion in 2025. The country remains a leader in adopting AI-driven and cloud-based TMS platforms, supported by a complex domestic freight landscape and rising pressure to enhance service quality. Predictive planning tools, automation, and real-time data integration are essential as transportation networks across road, freight, parcel, and last-mile delivery face labor shortages and fluctuating demand.

Major players in the Global Transportation Management System Market include SAP, Oracle, CH Robinson, Trimble, Manhattan Associates, Blue Yonder, MercuryGate International, E2open, Descartes, and Wise Tech Global. Companies operating in the Transportation Management System Market strengthen their competitive position by investing heavily in AI automation, modular platform designs, and advanced analytics that enhance forecasting accuracy and shipment visibility. Many organizations expand through strategic integrations with telematics providers, freight platforms, and warehouse management systems, creating unified logistics ecosystems for their customers. Vendors also focus on cloud-native architectures that deliver continuous updates and scalable deployments, enabling clients to adopt new features without operational disruption. Customized solutions for different transportation modes, along with flexible pricing based on shipment volume or usage, help broaden customer reach. Partnerships with carriers and 3PLs further enhance network data quality, ensuring TMS platforms deliver more reliable insights and measurable efficiency gains.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Platform

- 2.2.3 Transportation mode

- 2.2.4 Deployment mode

- 2.2.5 Enterprise size

- 2.2.6 Industry vertical

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising e-commerce and online retail demand

- 3.2.1.2 Globalization of supply chains

- 3.2.1.3 Need for real-time shipment visibility

- 3.2.1.4 Increasing focus on cost optimization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial implementation cost

- 3.2.2.2 Data security and compliance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Growth in small and medium-sized enterprises (SMEs)

- 3.2.3.3 Fleet electrification and green logistics

- 3.2.3.4 Partnerships with 3PL and logistics providers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 FMCSA Electronic Logging Device (ELD) mandate

- 3.4.1.2 Hours-of-Service (HOS) regulations

- 3.4.1.3 DOT safety regulations (CFR Parts 300-399)

- 3.4.2 Europe

- 3.4.2.1 GDPR compliance for shipment data

- 3.4.2.2 C-ITS (Cooperative Intelligent Transport Systems)

- 3.4.2.3 Cross-border transportation regulations

- 3.4.3 Asia Pacific

- 3.4.3.1 China ITS investment & standards

- 3.4.3.2 India GST impact on logistics

- 3.4.3.3 ASEAN cross-border transport facilitation

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Cloud-native microservices architecture

- 3.7.1.2 Artificial Intelligence & Machine Learning integration

- 3.7.2 Emerging technologies

- 3.7.2.1 Digital twin technology for network modeling

- 3.7.2.2 Autonomous vehicle integration readiness

- 3.7.1 Current technological trends

- 3.8 Pricing analysis

- 3.8.1 SaaS subscription pricing models

- 3.8.2 Perpetual license pricing

- 3.8.3 Transaction-based pricing (per shipment)

- 3.8.4 User-based pricing models

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.10.1 USPTO patent classification for TMS technologies

- 3.10.2 Key patent holders & innovation leaders

- 3.10.3 Emerging patent trends (AI, Blockchain, IoT)

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use cases

- 3.12.1 Retail & e-commerce use case economics

- 3.12.2 Healthcare & pharmaceuticals use case economics

- 3.12.3 Food & beverage use case economics

- 3.12.4. 3 PL & freight forwarders use case economics

- 3.13 Feature adoption rates & utilization analysis

- 3.13.1 Core feature adoption rates

- 3.13.2 Advanced feature adoption rates

- 3.13.3 Emerging feature adoption rates

- 3.13.4 Feature adoption by industry vertical

- 3.14 Migration patterns & switching trends

- 3.14.1 TMS migration drivers

- 3.14.2 Migration patterns by deployment type

- 3.14.3 Vendor switching trends

- 3.14.4 Migration timeline & complexity

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.6.4.1 Venture capital investment in TMS startups

- 4.6.4.2 Private equity activity in logistics technology

- 4.6.4.3 Government infrastructure investment (World Bank ITS report)

- 4.6.4.4 Corporate R&D spending by major vendors

- 4.7 Vendor selection criteria

- 4.8 Go-to-Market Strategies

Chapter 5 Market Estimates & Forecast, By Platform, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Solutions

- 5.2.1 Shipment planning

- 5.2.2 Order management

- 5.2.3 Audit & payments

- 5.2.4 Analytics & reporting

- 5.2.5 Routing & Tracking

- 5.2.6 Others

- 5.3 Services

- 5.3.1 Consulting

- 5.3.2 Implementation & integration

- 5.3.3 Support & maintenance

Chapter 6 Market Estimates & Forecast, By Transportation Mode, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Roadways

- 6.3 Railways

- 6.4 Airways

- 6.5 Waterways

Chapter 7 Market Estimates & Forecast, By Deployment model, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 On-premises

- 7.3 Cloud

Chapter 8 Market Estimates & Forecast, By Enterprise size, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Large enterprises

- 8.3 SMEs

Chapter 9 Market Estimates & Forecast, By Industry vertical, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Retail & e-commerce

- 9.3 Healthcare & pharmaceuticals

- 9.4 Distribution & logistics

- 9.5 Manufacturing

- 9.6 Government

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 Blue Yonder

- 11.1.2 C.H. Robinson

- 11.1.3 Descartes

- 11.1.4. E2 open

- 11.1.5 Infor

- 11.1.6 Manhattan Associates

- 11.1.7 Oracle

- 11.1.8 SAP

- 11.1.9 Trimble

- 11.1.10 Wise Tech Global

- 11.2 Regional players

- 11.2.1. Gtms

- 11.2.2 Alpega

- 11.2.3 Blujay Solutions

- 11.2.4 CTSI-Global

- 11.2.5 Korber

- 11.2.6 Kuebix

- 11.2.7 Logility

- 11.2.8 MercuryGate

- 11.2.9 Shippeo

- 11.2.10 Transporeon

- 11.3 Emerging players

- 11.3.1 Arrive Logistics

- 11.3.2 FourKites

- 11.3.3 Loadsmart

- 11.3.4 Locus

- 11.3.5 Motive

- 11.3.6 Parade

- 11.3.7 project44

- 11.3.8 Samsara

- 11.3.9 Shipsy

- 11.3.10 Transfix