|

시장보고서

상품코드

1892860

광간섭 단층촬영(OCT) 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Optical Coherence Tomography Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

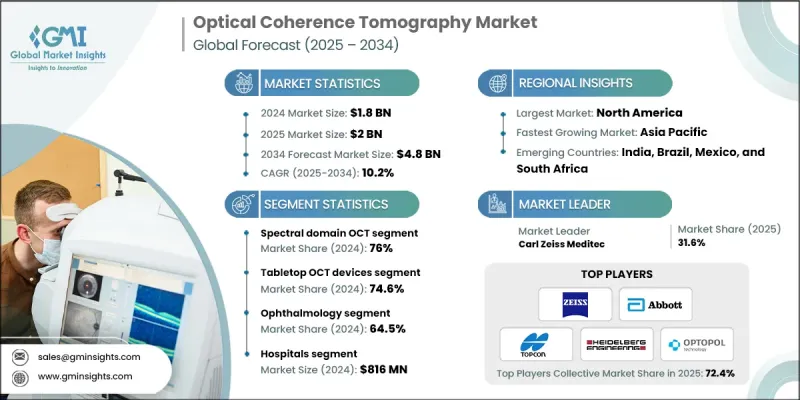

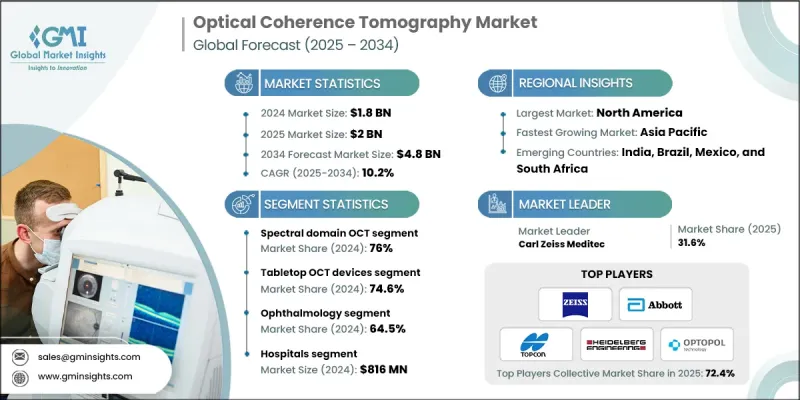

세계의 광간섭 단층촬영(OCT) 시장은 2024년에 18억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 10.2%로 성장하여 48억 달러에 이를 것으로 예측됩니다.

OCT는 저코히어런스 빛을 이용한 비침습적 영상진단법으로, 생체조직의 매우 상세한 단면 영상을 생성합니다. 진단 정확도 향상, 조직 깊숙한 곳까지 도달하는 깊이 확대, 영상 획득 속도의 고속화를 위한 연구개발이 가속화되면서 시장은 지속적으로 성장하고 있습니다. 이러한 발전은 다양한 임상 환경에서 차세대 진단 도구와 치료 모니터링 시스템의 도입을 촉진하고 있습니다. 소형 휴대용 OCT 장비에 대한 수요 증가도 개발 동향에 영향을 미치고 있으며, 특히 의료 서비스 제공업체가 지역 진료소, 이동 진료소, 재택 진료소, 외래 진료소 등에서 현장 검사에 대한 접근 가능한 솔루션을 찾고 있는 상황에서 특히 두드러집니다. 이동성과 워크플로우 효율화로 전환하는 가운데, 각 제조업체들은 보다 광범위한 임상적 용도를 염두에 두고 간소화되고 사용하기 쉬운 이미징 시스템 도입을 촉진하고 있습니다. 주요 안질환에 대한 조기 발견 전략의 도입 확대는 현대 안과 의료에서 OCT 기술에 대한 의존도를 더욱 공고히 하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 연도 시장 규모 | 18억 달러 |

| 예측 금액 | 48억 달러 |

| CAGR | 10.2% |

스펙트럼 도메인 OCT 부문은 2024년 76%의 점유율을 차지했습니다. 이 부문이 선도적인 위치를 차지하고 있는 이유는 망막 건강에 영향을 미치는 만성 안질환의 발생률이 증가함에 따라 정확하고 빠른 고해상도 영상 진단에 대한 필요성이 증가하고 있기 때문입니다. SD-OCT 장비는 망막 진단뿐만 아니라 전안부, 각막질환, 시신경 평가에도 자주 활용되고 있습니다. 질병의 병기 판정부터 치료 후 경과 관찰까지 다양한 임상 업무에 대응할 수 있는 적응성으로 종합적인 시력 평가에 필수적인 존재가 되었습니다.

탁상형 OCT 장비 부문은 2024년 74.6%의 점유율을 차지했습니다. 이러한 시스템은 안정적이고 정확한 이미지 제공과 다중 스캔 기술과의 호환성으로 인해 안과 전문가들 사이에서 여전히 선호되는 선택입니다. 녹내장 진행, 망막 질환, 전안부 건강 상태 분석을 지원하는 능력은 안과 센터, 전문 시설, 병원 부서에서 폭넓게 활용되고 있습니다. 현대의 탁상형 장비는 종종 여러 영상 기술을 단일 플랫폼에 통합하여 효율적인 진단 워크스테이션을 형성합니다.

미국의 광간섭단층촬영기(OCT) 시장은 2024년 6억 3,100만 달러에 달할 것으로 예상되며, 2034년에는 16억 달러에 달할 것으로 예측됩니다. 메디케어 및 민간 보험사의 OCT 관련 시술에 대한 광범위한 보험 적용은 환자와 의료 제공업체 모두에게 비용 절감으로 이어져 시장 도입을 촉진하고 있습니다. 보험 적용은 시신경 분석, 망막 스캔, OCT 혈관조영술 등 다양한 용도에 적용되어 안과 진료에서 OCT를 일상적인 임상 워크플로우에 통합하는 것을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- OCT 컴포넌트 OEM 제조업체

- 제조업체

- 규제기관

- 유통업체 및 공급업체

- 최종 용도

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 미국

- 유럽

- 아시아태평양

- 기술 동향

- 현재 기술 동향

- 신기술

- 동적 3D 조직 시각화를 위한 초고속 OCT

- 특허 분석

- 주요 특허 보유자 및 기술 리더

- 특허 만료 분석과 영향

- 특허 소송 및 분쟁

- 지역별 특허 보호 전략

- 가격 분석, 2024

- 향후 시장 동향

- 공급망과 유통 분석

- 원재료 조달

- 제조거점 분석

- 유통 채널 매핑과 파트너 네트워크

- 공급망 취약성과 리스크 경감책

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

제5장 시장 추산 및 예측 : 기술별, 2021-2034

- 주요 동향

- 스펙트럼 영역 OCT

- 스위프 소스 OCT

- 시간 영역 OCT

제6장 시장 추산 및 예측 : 제품 및 서비스별, 2021-2034

- 주요 동향

- 기기

- 탁상형 OCT 장비

- 카테터 기반 OCT 장비

- 핸드헬드 OCT 장비

- 도플러 OCT 장비

- 부품 교환 서비스 및 소프트웨어 라이선싱·업그레이드

- 기타 서비스

제7장 시장 추산 및 예측 : 용도별, 2021-2034

- 주요 동향

- 안과

- 순환기학

- 피부과

- 종양학

- 기타 용도

제8장 시장 추산 및 예측 : 최종 용도별, 2021-2034

- 주요 동향

- 병원

- 진단영상센터

- 외래수술센터(ASC)

- 기타 용도

제9장 시장 추산 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

제10장 기업 개요

- Abbott Laboratories

- Agfa-Gevaert

- Canon

- Carl Zeiss Meditec

- Gentuity

- Heidelberg Engineering

- Huvitz

- Metall Zug AG(Haag-Streit Group)

- Moptim(Shenzhen Certainn Technology)

- NIDEK

- Nikon Corporation(Optos plc)

- NinePoint Medical

- Notal Vision

- Novacam Technologies

- OPTOPOL Technology

- Philophos

- Tomey

- Topcon Corporation

- TowardPi(Beijing) Medical Technology

- Visionx

- Vivolight

- YSENMED

- ZD medical

The Global Optical Coherence Tomography Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 10.2% to reach USD 4.8 billion by 2034.

OCT is a non-invasive imaging method that uses low-coherence light to produce highly detailed cross-sectional visuals of biological tissues. The market continues to grow as research and development efforts accelerate the launch of technologies aimed at improving diagnostic clarity, increasing tissue-depth reach, and speeding image acquisition. These advancements support the introduction of next-generation diagnostic tools and therapy-monitoring systems across various clinical environments. Rising demand for compact and portable OCT devices is also influencing development trends, especially as healthcare providers seek accessible solutions for point-of-care testing across rural practices, traveling clinics, home care facilities, and outpatient centers. The growing shift toward mobility and workflow efficiency is encouraging manufacturers to introduce more streamlined and user-friendly imaging systems designed for broader clinical use. Increasing adoption of early-detection strategies for major eye diseases further strengthens the reliance on OCT technology in modern ophthalmic care.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $4.8 Billion |

| CAGR | 10.2% |

The spectral domain OCT segment accounted for a 76% share in 2024. This segment holds a leading position due to rising incidences of chronic eye disorders that impact retinal health and drive the need for precise, fast, and high-resolution imaging. SD-OCT devices are frequently used not only for retinal interpretation but also for assessing the anterior segment, corneal conditions, and the optic nerve. Their adaptability for various clinical tasks, from disease staging to post-treatment evaluations, makes them integral to comprehensive vision assessment.

The tabletop OCT equipment segment held a 74.6% share in 2024. These systems remain the preferred choice for ophthalmic professionals because they offer stable, highly accurate imaging and compatibility with multiple scanning techniques. Their widespread use in eye centers, specialty facilities, and hospital departments is supported by their ability to assist in analyzing glaucoma progression, retinal disorders, and anterior segment health. Modern tabletop devices often combine multiple imaging technologies into a single platform, creating efficient diagnostic workstations.

United States Optical Coherence Tomography Market is projected to reach USD 631 million in 2024 and reach USD 1.6 billion by 2034. Substantial coverage from Medicare and private payers for OCT-related procedures enhances market adoption by lowering costs for both patients and providers. Reimbursement applies to several applications, including optic nerve analysis, retinal scanning, and OCT angiography, which encourages eye care practices to integrate OCT more routinely into clinical workflows.

Key companies participating in the Optical Coherence Tomography Market include Abbott Laboratories, Canon, Agfa-Gevaert, Gentuity, Huvitz, Heidelberg Engineering, Carl Zeiss Meditec, NIDEK, Metall Zug AG (Haag-Streit Group), Moptim (Shenzhen Certainn Technology), Nikon Corporation (Optos plc), Philophos, NotaLVision, NinePoint Medical, Novacam Technologies, OPTOPOL Technology, Topcon Corporation, Tomey, TowardPi (Beijing) Medical Technology, Visionx, Vivolight, YSENMED, and ZD Medical. Key strategies employed by major companies in the Optical Coherence Tomography Market focus on enhancing imaging performance, broadening clinical applications, and expanding product accessibility. Firms continue to invest in advanced light-source technologies and upgraded scanning algorithms to deliver sharper resolution and faster image capture. Many players are integrating multimodal imaging into unified systems to streamline diagnostic processes for clinicians. Collaborations with healthcare providers and academic research centers help refine device accuracy and support clinical validation.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Technology trends

- 2.2.3 Product and services trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Original equipment manufacturers (OEMs) of OCT components

- 3.1.2 Manufacturer

- 3.1.3 Regulatory authorities

- 3.1.4 Distributors and suppliers

- 3.1.5 End use

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of eye disorders

- 3.2.1.2 Advancements in OCT technology

- 3.2.1.3 Rising adoption of non-invasive diagnostic techniques

- 3.2.1.4 Increasing healthcare investments and awareness in emerging economies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of therapies

- 3.2.2.2 Shortage of skilled professionals trained to operate and interpret OCT systems

- 3.2.3 Market opportunities

- 3.2.3.1 AI-powered diagnostic algorithms and automated analysis

- 3.2.3.2 Increasing applications of OTC in pediatric and critical care

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Swept source OCT for deep tissue visualization

- 3.5.1.2 OCT angiography for non-invasive vascular mapping

- 3.5.1.3 Portable and multimodal oct devices for point-of-care diagnostics

- 3.5.2 Emerging technologies

- 3.5.2.1 Quantum-enhanced OCT for ultra-sensitive imaging

- 3.5.2.2 Adaptive optics integration for real-time aberration correction

- 3.5.2. 3. Ultra-high-speed OCT for dynamic 3D tissue visualization

- 3.5.1 Current technological trends

- 3.6 Patent analysis

- 3.6.1 Key patent holders and technology leaders

- 3.6.2 Patent expiration analysis and impact

- 3.6.3 Patent litigation and disputes

- 3.6.4 Geographic patent protection strategies

- 3.7 Pricing analysis, 2024

- 3.8 Future market trends

- 3.8.1 AI-driven OCT platforms for predictive diagnostics

- 3.8.2 Cloud-based OCT data management and telemedicine integration

- 3.8.3 Expansion of OCT applications beyond ophthalmology

- 3.9 Supply chain and distribution analysis

- 3.9.1 Raw material sourcing

- 3.9.2 Manufacturing hub analysis

- 3.9.3 Distribution channel mapping and partner networks

- 3.9.4 Supply chain vulnerabilities and risk mitigation

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key development

Chapter 5 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Spectral domain OCT

- 5.3 Swept-source OCT

- 5.4 Time domain OCT

Chapter 6 Market Estimates and Forecast, By Product and Services, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Instruments

- 6.2.1 Tabletop OCT devices

- 6.2.2 Catheter based OCT devices

- 6.2.3 Handheld OCT devices

- 6.2.4 Doppler OCT devices

- 6.3 Component replacement services and software licensing and upgrade

- 6.4 Other services

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Ophthalmology

- 7.3 Cardiology

- 7.4 Dermatology

- 7.5 Oncology

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Diagnostic imaging centers

- 8.4 Ambulatory surgical centers

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 Agfa-Gevaert

- 10.3 Canon

- 10.4 Carl Zeiss Meditec

- 10.5 Gentuity

- 10.6 Heidelberg Engineering

- 10.7 Huvitz

- 10.8 Metall Zug AG (Haag-Streit Group)

- 10.9 Moptim (Shenzhen Certainn Technology)

- 10.10 NIDEK

- 10.11 Nikon Corporation (Optos plc)

- 10.12 NinePoint Medical

- 10.13 Notal Vision

- 10.14 Novacam Technologies

- 10.15 OPTOPOL Technology

- 10.16 Philophos

- 10.17 Tomey

- 10.18 Topcon Corporation

- 10.19 TowardPi (Beijing) Medical Technology

- 10.20 Visionx

- 10.21 Vivolight

- 10.22 YSENMED

- 10.23 ZD medical