|

시장보고서

상품코드

1892869

원격 환자 모니터링 기기 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Remote Patient Monitoring (RPM) Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

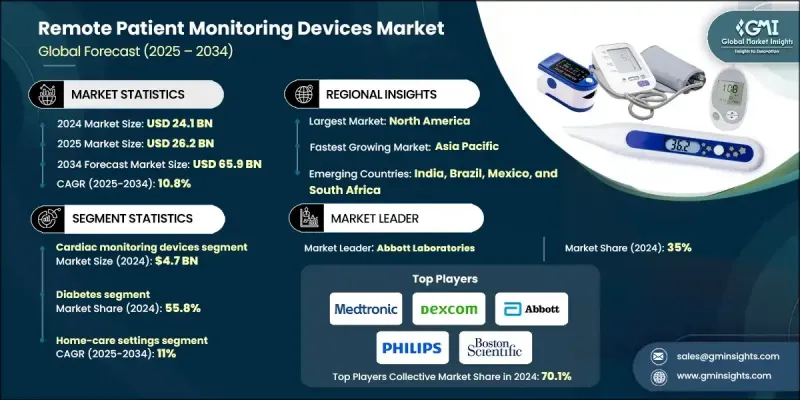

세계의 원격 환자 모니터링 기기 시장은 2024년에 241억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 10.8%로 성장하여 659억 달러에 이를 것으로 예측됩니다.

시장 성장은 만성 질환 증가, 의료 분야의 급속한 디지털화, 재입원율 및 전체 의료비 절감에 대한 요구가 증가함에 따라 주도되고 있습니다. 원격 환자 모니터링(RPM)은 기존 임상 환경 밖에서도 환자의 활력 징후와 건강 상태를 지속적으로 추적할 수 있어 의사가 데이터에 기반한 의사결정을 보다 신속하게 내릴 수 있도록 돕고, 환자의 치료 계획 준수율을 높이는 데 기여합니다. 스마트폰의 보급, 커넥티드 의료기기, 클라우드 기반 플랫폼의 채택 확대로 RPM 솔루션의 편의성, 정확성, 확장성이 크게 향상되었습니다. 이러한 기술들은 종합적으로 보다 적극적이고 예방적인 치료 모델을 지원하고, 응급실 방문을 줄이며, 의료 인프라에 대한 부담을 줄일 수 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 개시 연도 시장 규모 | 241억 달러 |

| 예측 금액 | 659억 달러 |

| CAGR | 10.8% |

세계적으로 가치 기반 의료(Value-Based Care)와 재택치료로의 전환은 원격 환자 모니터링(RPM) 기기에 대한 수요를 더욱 가속화시키고 있습니다. 보험사 및 의료 서비스 제공업체들은 입원일수 감소, 재입원 페널티 감소, 고위험군 환자 관리 개선 등 원격 모니터링의 경제적 이점을 점점 더 많이 인식하고 있습니다. 또한, 전 세계적으로 고령화 및 당뇨병, 심혈관질환, 호흡기질환 등의 유병률 증가로 RPM의 대상 환자층이 확대되고 있습니다. 디지털 건강 증진, 원격 의료 보험 적용, 표준 치료 경로에 원격 모니터링 통합과 같은 정부 정책도 예측 기간 동안 시장 침투율 향상에 중요한 역할을 할 것으로 보입니다.

심장 모니터링 기기 부문은 2024년 47억 달러 시장 규모를 창출했습니다. 이 부문에는 부정맥, 심부전 악화, 기타 심장 이상을 실시간으로 감지하는 데 사용되는 심전도 장치, 이식형 심장 모니터, 웨어러블 심장 모니터, 이벤트 레코더가 포함됩니다. 전 세계 심혈관 질환의 높은 부담과 고위험 심장 환자들에 대한 지속적인 모니터링의 중요성이 이 부문의 주요 촉진요인입니다. 원격 심장 모니터링은 잦은 대면 진료의 필요성을 줄이고, 생명을 위협하는 사건을 조기에 발견할 수 있으며, 보다 적절한 약물 조정을 돕습니다.

재택의료 환경 부문은 편의성 향상, 비용 절감, 재입원 최소화 등을 목적으로 의료서비스가 병원에서 환자의 집으로 이동함에 따라 2024년 11%의 점유율을 차지할 것으로 예상했습니다. 이 부문에서는 활력징후 모니터, 혈당 측정기, 심장용 웨어러블 기기, 커넥티드 산소포화도 측정기 등 원격 모니터링 기기가 만성질환자, 수술 후 환자, 노인을 지속적으로 또는 계획적으로 추적하는 데 사용됩니다. 재택 모니터링을 통해 환자는 익숙한 환경에서 지내면서도 의료 전문가의 가상 감독을 받을 수 있어 치료 순응도와 삶의 질을 향상시킬 수 있습니다.

북미 원격 환자 모니터링 기기 시장은 2024년 42.3%의 점유율을 차지하며 지역별로 가장 큰 비중을 차지했습니다. 이 지역의 선도적 지위는 탄탄한 의료 인프라, 높은 의료비 지출, 디지털 헬스 기술에 대한 적극적인 도입으로 뒷받침되고 있습니다. 특히 미국에서는 원격 모니터링 서비스에 대한 유리한 상환 프레임워크가 의료 서비스 제공업체들이 만성질환 관리 프로그램에 RPM(원격 환자 모니터링)을 통합하는 데 큰 도움이 되고 있습니다. 또한, 높은 생활습관병 유병률, 고령 인구, 인터넷 및 스마트 기기에 대한 광범위한 접근성은 원격 모니터링 솔루션 도입에 이상적인 환경을 조성하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 기술 동향

- 향후 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추산 및 예측 : 제품별, 2021-2034

- 주요 동향

- 심전도 모니터링 기기

- 혈압 측정 기기

- 신경 모니터링 기기

- 호흡 모니터링 기기

- 다기능 모니터링 기기

- 혈당 측정 기기

- 태아 및 신생아 모니터링 기기

- 수면 모니터링 기기

- 기타 제품

제6장 시장 추산 및 예측 : 용도별, 2021-2034

- 주요 동향

- 심혈관 질환

- 암

- 당뇨병

- 신경 질환

- 감염증

- 호흡기 질환

- 기타 용도

제7장 시장 추산 및 예측 : 최종 용도별, 2021-2034

- 주요 동향

- 홈케어 환경

- 장기 요양

- 기타 용도

제8장 시장 추산 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 폴란드

- 스위스

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 태국

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 칠레

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

- 이스라엘

제9장 기업 개요

- Abbott Laboratories

- Baxter International

- BIOTRONIK

- Boston Scientific

- Dexcom

- F. Hoffmann-La Roche

- GE Healthcare

- Johnson &Johnson

- Koninklijke Philips N.V.

- Medtronic

- OMRON

- Sotera Wireless

- Vital Connect

The Global Remote Patient Monitoring Devices Market was valued at USD 24.1 billion in 2024 and is estimated to grow at a CAGR of 10.8% to reach USD 65.9 billion by 2034.

Market growth is driven by the rising prevalence of chronic diseases, rapid digitalization of healthcare, and the growing need to reduce hospital readmissions and overall care costs. Remote patient monitoring (RPM) enables continuous tracking of patients' vital signs and health status outside traditional clinical settings, empowering physicians to make faster, data-driven decisions and improving patient adherence to treatment plans. Rising adoption of smartphones, connected medical devices, and cloud-based platforms has significantly enhanced the usability, accuracy, and scalability of RPM solutions. These technologies collectively support more proactive and preventive care models, reducing emergency visits and easing the burden on healthcare infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $24.1 Billion |

| Forecast Value | $65.9 Billion |

| CAGR | 10.8% |

The global shift towards value-based care and home-based healthcare is further accelerating the demand for RPM devices. Payers and providers are increasingly recognizing the economic benefits of remote monitoring, such as reduced inpatient days, lower readmission penalties, and better management of high-risk patient cohorts. Additionally, aging populations worldwide and the rising incidence of conditions like diabetes, cardiovascular diseases, and respiratory disorders are expanding the addressable patient pool for RPM. Government initiatives promoting digital health, telehealth reimbursement, and integration of remote monitoring into standard care pathways are also playing a critical role in enhancing market penetration over the forecast period.

The cardiac monitoring devices segment generated USD 4.7 billion in 2024. This segment includes ECG devices, implantable cardiac monitors, wearable heart monitors, and event recorders used to detect arrhythmias, heart failure exacerbations, and other cardiac abnormalities in real time. The high burden of cardiovascular diseases globally, combined with the critical need for continuous surveillance of high-risk cardiac patients, is a core driver for this segment. Remote cardiac monitoring reduces the need for frequent in-person consultations, enables early identification of life-threatening events, and supports better medication titration.

The home care settings segment held 11% share in 2024 as healthcare delivery shifted from hospitals to patients' homes to improve comfort, reduce costs, and minimize hospital readmissions. In this segment, remote monitoring devices such as vital signs monitors, glucose meters, cardiac wearables, and connected oximeters are used to track patients with chronic conditions, post-operative cases, and elderly individuals on a continuous or scheduled basis. Home-based monitoring enables patients to remain in a familiar environment while still being under the virtual supervision of healthcare professionals, which enhances treatment adherence and quality of life.

North America Remote Patient Monitoring Devices Market held 42.3% share in 2024, accounting for the largest regional share. The region's leadership is supported by a well-established healthcare infrastructure, high healthcare expenditure, and strong adoption of digital health technologies. Favorable reimbursement frameworks for remote monitoring services, particularly in the United States, have significantly encouraged providers to incorporate RPM into chronic disease management programs. Additionally, a high prevalence of lifestyle-related disorders, a large elderly population, and widespread access to the internet and smart devices create an ideal environment for the deployment of remote monitoring solutions.

Key players operating in the Global Remote Patient Monitoring Devices Market include Philips Healthcare, Medtronic plc, GE HealthCare, Abbott Laboratories, Boston Scientific Corporation, Nihon Kohden Corporation, ResMed Inc., Dexcom, Inc., and Masimo Corporation. These companies focus on continuous product innovation, integrating advanced sensors, wireless connectivity, and data analytics into their device portfolios. They are also actively involved in strategic partnerships with hospitals, telehealth platforms, and payers to expand their installed base and enhance recurring revenue streams via monitoring services and software subscriptions. Many of these players are investing in AI-enabled platforms that can automatically flag abnormal readings, support predictive risk scoring, and simplify clinical workflows, making remote monitoring more scalable and effective for large patient populations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360º synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of chronic diseases across the globe

- 3.2.1.2 Growing disposable income and healthcare expenditure in emerging countries

- 3.2.1.3 Technological advancement in developed nations

- 3.2.1.4 Growing adoption of remote patient monitoring devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices

- 3.2.2.2 Stringent regulatory framework

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of AI-powered predictive monitoring tools

- 3.2.3.2 Emergence of wearable biosensors for continuous, real-time health tracking

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Cardiac monitoring devices

- 5.3 Blood pressure monitoring devices

- 5.4 Neurological monitoring devices

- 5.5 Respiratory monitoring devices

- 5.6 Multiparameter monitoring devices

- 5.7 Blood glucose monitoring devices

- 5.8 Fetal and neonatal monitoring devices

- 5.9 Sleep monitoring devices

- 5.10 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cardiovascular diseases

- 6.3 Cancer

- 6.4 Diabetes

- 6.5 Neurological disorders

- 6.6 Infectious diseases

- 6.7 Respiratory diseases

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Home-care settings

- 7.3 Long-term care

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Poland

- 8.3.8 Switzerland

- 8.3.9 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Thailand

- 8.4.7 Indonesia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Colombia

- 8.5.5 Chile

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Israel

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Baxter International

- 9.3 BIOTRONIK

- 9.4 Boston Scientific

- 9.5 Dexcom

- 9.6 F. Hoffmann-La Roche

- 9.7 GE Healthcare

- 9.8 Johnson & Johnson

- 9.9 Koninklijke Philips N.V.

- 9.10 Medtronic

- 9.11 OMRON

- 9.12 Sotera Wireless

- 9.13 Vital Connect