|

시장보고서

상품코드

1892886

전기강판 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Electrical Steel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

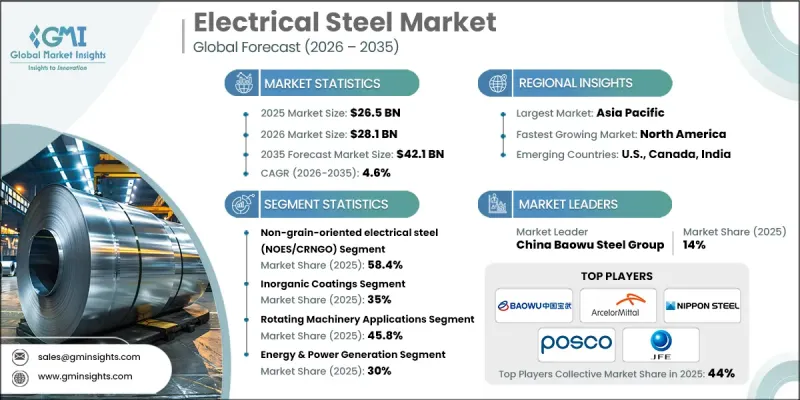

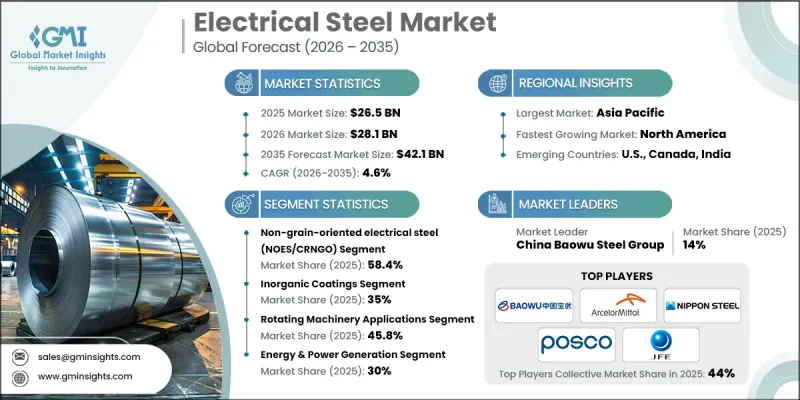

세계의 전기강판 시장은 2025년에 265억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.6%를 나타내 421억 달러에 이를 것으로 예측되고 있습니다.

전기강판은 모터, 변압기, 발전기의 효율 향상에 중요한 역할을 하며, 세계의 전기 및 산업 시스템의 핵심 부품으로서 기능하고 있습니다. 구조용 강재를 공급할 뿐만 아니라 자동차, 전력 인프라, 산업 자동화 등의 분야에 있어서 중요한 하류 가치를 창출해 현대경제에 있어서 전략적 소재로서의 지위를 확립하고 있습니다. 전기자동차의 급속한 보급, 송전망 근대화 프로젝트, 산업 자동화의 진전으로 시장은 더욱 성장할 것으로 전망되고 있습니다. 고성능 급료는 원재료 비용의 변동에도 불구하고 성능 요구에 따라 강한 가격 유지가 예상됩니다. 아시아는 제조업의 중심지와 인프라 확장에 힘입어 주요한 수요 거점으로 계속되고 있는 한편, 유럽과 북미는 전기 추진책과 에너지 절약 규제를 통해 성장을 견인합니다. 시장은 얇은 제품과 고도 등급 제품이 경쟁적 중요성을 늘리고 동시에 틈새 전자 부품에 대한 주목이 높아지는 가운데 성능 주도의 생태계로 진화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 가치 | 265억 달러 |

| 예측 금액 | 421억 달러 |

| CAGR | 4.6% |

비방향성 전기강판(NOES/CRNGO) 부문은 2025년에 58.4%의 점유율을 차지했고 2035년까지 연평균 복합 성장률(CAGR) 4.9%를 나타낼 것으로 예측됩니다. NOES는 모든 방향에서 균일한 자기 성능을 발휘하기 때문에 모터나 발전기 등의 회전 기계에 최적이며, 에너지 효율과 동작 속도가 중요한 전기자동차 및 산업 자동화에 필수적입니다.

무기 코팅 부문은 2025년에 35%의 점유율을 차지했고 2026년부터 2035년에 걸쳐 CAGR 4.6%를 나타낼 것으로 예상됩니다. 무기 코팅은 변압기 코어나 중전 설비 등 고온 절연 용도에 매우 적합하며, 가혹한 조건 하에서의 층간 손실을 저감하여 송전의 신뢰성을 확보합니다.

북미의 전기강판 시장은 2025년에 12.4%의 점유율을 차지했으며, 선진적인 제조 능력, 견고한 규제 프레임워크, 전자 인프라에 대한 대규모 투자로 전략적 거점으로 급속히 대두했습니다. 이 지역에서는 엄격한 기술적 및 환경적 요건을 충족하기 위해 에너지 절약성과 고성능을 겸비한 등급이 중시되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 이익률

- 각 단계별 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 효율성 규제에 의해 고품위 원료의 채용이 촉진됩니다.

- 전기자동차의 보급이 초박형 NOES 수요를 촉진하고 있습니다.

- 송전망의 근대화에 의해 정부 기관용 에너지 시스템(GOES) 수요가 확대되고 있습니다.

- 업계의 잠재적 위험 및 과제

- 원재료 가격의 변동성

- 얇은/고강도(HiB) 제품의 생산 능력 제약

- 시장 기회

- 자기 접착 코팅은 조립 공정을 효율화하고 수율을 향상시킵니다.

- 데이터센터용 UPS·변압기 업그레이드로 고품질 GOES 수요가 높아지고 있습니다.

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 유형별

- 향후 시장 동향

- 기술 및 혁신 현황

- 현재 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 파트너십 및 협력

- 신제품 출시

- 사업 확대 계획

제5장 시장 추계·예측 : 제품 유형별(2022-2035년)

- 비결정립 방향성 전기강판(NOES/CRNGO)

- 결정립 방향성 전기강판(GOES/CRGO)

- 첨단 연자성 재료

- 비정질 전기강판

- 나노결정 전기강판

- 다층 및 복합 전기강판

제6장 시장 추계·예측 : 코팅 유형별(2022-2035년)

- 무기 코팅

- C-2/EC-2(밀유리 - 마그네슘 실리케이트)

- C-4/EC-4(인산염 또는 화학 처리)

- C-5/EC-5(무기질/세라믹 충전)

- 유기 코팅

- C-3/EC-3(유기 바니시/에나멜)

- C-6/EC-6(무기질 충전제가 포함된 유기 코팅)

- 자연 산화물 코팅

- 자가 접착 코팅

제7장 시장 추계·예측 : 용도별(2022-2035년)

- 회전 기계 용도

- 변압기 용도

- 전력 변압기

- 배전 변압기

- 특수 변압기

- 재생에너지 변압기

- 전자기 부품

- 인덕터 및 리액터

- 안정기 및 조명

- 무선 전력 전송

제8장 시장 추계·예측 : 최종 용도별(2022-2035년)

- 에너지 및 발전

- 전력 회사

- 신재생에너지

- 기존 발전 방식

- 에너지 저장 시스템

- 자동차 및 운송

- 전기자동차(배터리식 전기자동차 - BEV)

- 하이브리드 전기자동차(HEV/PHEV)

- 자동차 보조 시스템

- EV 충전 인프라

- 철도 및 대중교통

- 항공우주

- 산업 제조

- 산업 기계 및 설비

- 로봇 공학 및 자동화

- 석유 및 가스 설비

- 가전제품 및 전자기기

- 가전제품

- 전동 공구

- 소비자 전자제품

- 데이터센터 및 IT 인프라

- UPS 시스템

- 데이터센터 변압기

- 서버 냉각 시스템

- HVAC 및 건물 시스템

- 상업용 HVAC 시스템

- 주거용 HVAC

- 엘리베이터 및 에스컬레이터

제9장 시장 추계·예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Nippon Steel Corporation

- JFE Steel Corporation

- ArcelorMittal SA

- POSCO(Pohang Iron & Steel Co.)

- China Baowu Steel Group

- thyssenkrupp Electrical Steel GmbH

- Cleveland-Cliffs Inc.(AK Steel)

- Tata Steel Limited

- Aperam SA

- Waelzholz Group

- Ansteel Group Corporation

- HBIS Group(Hebei Iron & Steel)

- Nucor Corporation

- Metglas Inc.(Hitachi Metals Group)

- Advanced Technology &Materials Co. Ltd.(AT&M)

The Global Electrical Steel Market was valued at USD 26.5 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 42.1 billion by 2035.

Electrical steel plays a vital role in enhancing the efficiency of motors, transformers, and generators, acting as a core component of electrification and industrial systems worldwide. It not only supplies structural steel but also drives significant downstream value in sectors such as automotive, power infrastructure, and industrial automation, positioning it as a strategic material for modern economies. The market is expected to gain momentum due to the rapid adoption of electric vehicles, grid modernization projects, and industrial automation. Premium grades are expected to maintain strong pricing due to performance demands, despite raw material cost fluctuations. Asia remains the primary demand hub, supported by manufacturing centers and infrastructure expansion, while Europe and North America drive growth through electrification initiatives and energy-efficiency regulations. The market is evolving into a performance-driven ecosystem with thin-gauge and advanced-grade products gaining competitive importance, alongside a rising focus on niche electromagnetic components.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $26.5 Billion |

| Forecast Value | $42.1 Billion |

| CAGR | 4.6% |

The non-grain-oriented electrical steel (NOES/CRNGO) segment held 58.4% share in 2025 and is expected to grow at a CAGR of 4.9% through 2035. NOES is ideal for rotating machinery, including motors and generators, as it offers uniform magnetic performance in all directions, making it essential for electric vehicles and industrial automation where energy efficiency and operational speed are critical.

The inorganic coatings segment accounted for a 35% share in 2025 and is expected to grow at a CAGR of 4.6% from 2026 to 2035. Inorganic coatings are highly suitable for high-temperature insulation applications, including transformer cores and heavy-duty electrical equipment, reducing interlaminar losses under extreme conditions and ensuring reliability in power transmission.

North America Electrical Steel Market accounted for a 12.4% share in 2025 and is rapidly emerging as a strategic hub due to advanced manufacturing capabilities, strong regulatory frameworks, and significant investments in electrification infrastructure. The region emphasizes energy-efficient, high-performance grades to meet increasingly stringent technical and environmental requirements.

Major players in the Global Electrical Steel Market include Nippon Steel Corporation, JFE Steel Corporation, ArcelorMittal S.A., POSCO (Pohang Iron & Steel Co.), China Baowu Steel Group, Thyssenkrupp Electrical Steel GmbH, Cleveland-Cliffs Inc. (AK Steel), Tata Steel Limited, Aperam S.A., Waelzholz Group, Ansteel Group Corporation, HBIS Group (Hebei Iron & Steel), Nucor Corporation, Metglas Inc. (Hitachi Metals Group), and Advanced Technology & Materials Co. Ltd. (AT&M). Companies in the Global Electrical Steel Market are strengthening their foothold by investing in R&D for advanced-grade and thin-gauge products, enabling higher efficiency and performance. Strategic partnerships with automotive and industrial manufacturers enhance integration into critical applications. Expanding production capacities in high-demand regions, adopting sustainable manufacturing practices, and leveraging digital technologies for process optimization improve operational efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Coating type

- 2.2.4 Application

- 2.2.5 End use

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Efficiency regulations lift high-grade adoption.

- 3.2.1.2 EV proliferation boosts ultra-thin NOES demand.

- 3.2.1.3 Grid modernization expands GOES demand.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw material volatility.

- 3.2.2.2 Thin gauge/HiB capacity constraints.

- 3.2.3 Market opportunities

- 3.2.3.1 Self-bonding coatings streamline assembly and improve yields.

- 3.2.3.2 Data center UPS/transformer upgrades raise premium GOES pull.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Non-grain-oriented electrical steel (NOES/CRNGO)

- 5.3 Grain-oriented electrical steel (GOES/CRGO)

- 5.4 Advanced soft magnetic materials

- 5.4.1 Amorphous electrical steel

- 5.4.2 Nanocrystalline electrical steel

- 5.4.3 Multilayer & composite electrical steel

Chapter 6 Market Estimates and Forecast, By Coating Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Inorganic coatings

- 6.2.1 C-2 / EC-2 (mill glass - magnesium silicate)

- 6.2.2 C-4 / EC-4 (phosphate or chemical treatment)

- 6.2.3 C-5 / EC-5 (inorganic/ceramic filled)

- 6.3 Organic coatings

- 6.3.1 C-3 / EC-3 (organic varnish/enamel)

- 6.3.2 C-6 / EC-6 (organic with inorganic fillers)

- 6.4 Natural oxide coatings

- 6.5 Self-bonding coatings

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Rotating machinery applications

- 7.3 Transformer applications

- 7.3.1 Power transformers

- 7.3.2 Distribution transformers

- 7.3.3 Specialty transformers

- 7.3.4 Renewable energy transformers

- 7.4 Electromagnetic components

- 7.4.1 Inductors & reactors

- 7.4.2 Ballasts & lighting

- 7.4.3 Wireless power transfer

Chapter 8 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Energy & power generation

- 8.2.1 Electric utilities

- 8.2.2 Renewable energy

- 8.2.3 Conventional power generation

- 8.2.4 Energy storage systems

- 8.3 Automotive & transportation

- 8.3.1 Electric vehicles (battery electric vehicles - BEV)

- 8.3.2 Hybrid electric vehicles (HEV/PHEV)

- 8.3.3 Automotive auxiliary systems

- 8.3.4 EV charging infrastructure

- 8.3.5 Rail & mass transit

- 8.3.6 Aerospace

- 8.4 Industrial manufacturing

- 8.4.1 Industrial machinery & equipment

- 8.4.2 Robotics & automation

- 8.4.3 Oil & gas equipment

- 8.5 Consumer appliances & electronics

- 8.5.1 Home appliances

- 8.5.2 Power tools

- 8.5.3 Consumer electronics

- 8.6 Data centers & IT infrastructure

- 8.6.1 UPS systems

- 8.6.2 Data center transformers

- 8.6.3 Server cooling systems

- 8.7 HVAC & building systems

- 8.7.1 Commercial HVAC systems

- 8.7.2 Residential HVAC

- 8.7.3 Elevators & escalators

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Nippon Steel Corporation

- 10.2 JFE Steel Corporation

- 10.3 ArcelorMittal S.A.

- 10.4 POSCO (Pohang Iron & Steel Co.)

- 10.5 China Baowu Steel Group

- 10.6 thyssenkrupp Electrical Steel GmbH

- 10.7 Cleveland-Cliffs Inc. (AK Steel)

- 10.8 Tata Steel Limited

- 10.9 Aperam S.A.

- 10.10 Waelzholz Group

- 10.11 Ansteel Group Corporation

- 10.12 HBIS Group (Hebei Iron & Steel)

- 10.13 Nucor Corporation

- 10.14 Metglas Inc. (Hitachi Metals Group)

- 10.15 Advanced Technology & Materials Co. Ltd. (AT&M)