|

시장보고서

상품코드

1892901

산업용 트럭 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Industrial Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

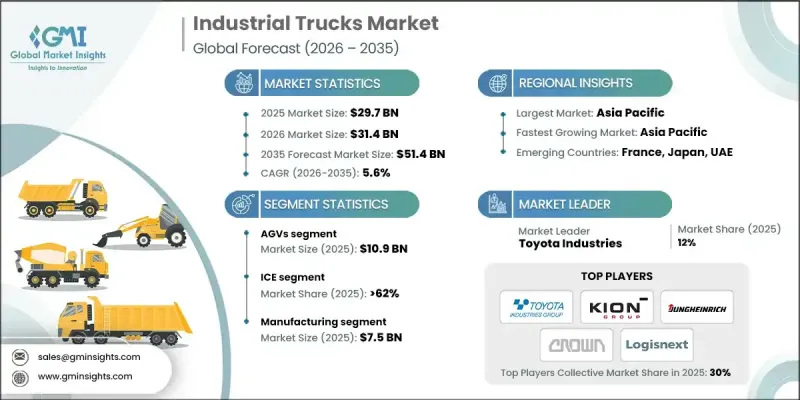

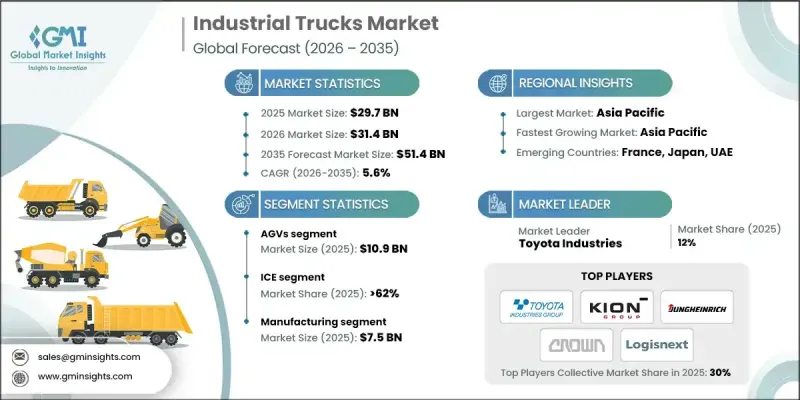

세계의 산업용 트럭 시장은 2025년에 297억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 5.6%를 나타내 514억 달러에 이를 것으로 예측됩니다.

전자상거래의 급속한 확대는 공급망의 재구축을 지속적으로 촉진하고 기업은 보다 빠르고 효율적인 자재 운반 솔루션의 도입을 강요받고 있습니다. 온라인 주문량이 증가함에 따라 기업은 신속한 배송 요구에 대응하기 위해 대규모 유통 거점과 소규모 완성 거점에 대한 투자를 추진하고 있습니다. 이러한 활동 증가는 창고 작업 전반에 걸쳐 제품의 고속 이동을 지원하는 지게차, 팔레트 트럭 및 자율 주행 차량 수요를 증가시키고 있습니다. 조직이 신속한 내부 운송 및 처리 능력 향상을 선호하는 동안 산업용 트럭은 물류 환경에서 중요한 경쟁 우위가 되고 있습니다. 로봇공학, 센서 기반 시스템, 통합형 보관 기술을 포함한 창고 자동화의 진보는 기업이 노동력 최적화, 정밀도 극대화, 귀중한 창고 공간의 유효 활용을 추구함에 따라 수요를 더욱 가속화하고 있습니다. 이러한 변화는 자동화 프로세스가 워크플로우를 개선하고 높은 생산성 수준을 지원하는 밀집된 도시 시장에서 특히 두드러집니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 가치 | 297억 달러 |

| 예측 금액 | 514억 달러 |

| CAGR | 5.6% |

AGV 부문은 2025년에 109억 달러 시장 규모를 창출했습니다. 자동 유도 차량(AGV)은 레이저 기반 내비게이션, 유도 시스템, 이미지 인식 도구 등의 기술을 사용하여 자율적으로 작동합니다. 이러한 차량은 미리 설정된 경로를 주행하고 실시간으로 경로를 변경할 수 있습니다. 이를 통해 창고 내에서의 자재의 안전하고 효율적인 운송이 수동 조작 없이도 실현됩니다. 팔레트, 컨테이너, 기타 화물을 일관성과 정밀도로 이동시키는 능력에 의해 현대의 자재 운반 환경에 있어서 필수적인 존재가 되고 있습니다.

내연기관(ICE) 부문은 2025년 62%의 점유율을 차지했습니다. 디젤, 가솔린, LPG를 동력원으로 하는 내연기관 트럭은 실내·옥외를 불문하고 가혹한 자재 운반 작업에 있어서 여전히 높은 신뢰성을 유지하고 있습니다. 높은 토크와 내구성을 특징으로 하는 이러한 차량은 어려운 조건 하에서 중량물을 들어 올리고 운반해야 하는 산업에 적합합니다. 그 성능은 광업, 대규모 제조업, 건설업 등의 분야에서 매우 중요합니다.

미국의 산업용 트럭 시장은 2025년에 75%의 점유율을 차지하고 63억 달러 규모에 이르렀습니다. 창고의 확장과 자동화 기술의 급속한 보급이 결합되어 제조, 물류, 전자상거래 운영 전반에 걸쳐 견조한 수요를 계속 견인하고 있습니다. 전동식 장비와 고급 취급 솔루션에 대한 관심 증가는 기업의 지속가능성 목표와 안전 기준 준수의 지속적인 노력을 반영합니다. 주요 세계 OEM의 존재와 차세대 자재관리 기술에 대한 엄청난 투자로 미국은 산업용 트럭 분야에서 혁신의 중심지로 자리잡고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 이익률

- 각 단계별 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전자상거래 확대와 창고 자동화

- Industry 4.0 기술의 채용

- 제조업, 건설업, 물류업의 성장

- 선진국 시장에서의 노동력 부족

- 업계의 잠재적 위험 및 과제

- 초기 비용과 유지 관리비의 높이

- 공급망의 혼란과 부품 부족

- 기회

- 전기·제로 에미션 트럭

- 자동 반송차(AGV) 및 자율 주행 트럭

- 성장 촉진요인

- 성장 가능성 분석

- 향후 시장 동향

- 기술 및 혁신 현황

- 현재 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 유형별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 파트너십 및 협력

- 신제품 출시

- 확대 계획

제5장 시장 추계·예측 : 유형별(2021-2034년)

- 무인 반송차(AGV)

- 핸드, 플랫폼 및 팔레트 트럭

- 오더 피커

- 팔레트 잭

- 사이드 로더

- 워키 스태커

제6장 시장 추계·예측 : 추진력별(2021-2034년)

- 내연기관(ICE)

- 전기식

제7장 시장 추계·예측 : 사업자별(2021-2034년)

- 수동식

- 반자동식

- 완전 자동식

제8장 시장 추계·예측 : 최종 이용 산업별(2021-2034년)

- 식품 및 음료

- 자동차

- 소매 및 전자상거래

- 건설 및 광업

- 제조업

- 제약

- 물류 및 창고업

- 기타

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Anhui Heli

- BYD Company

- Clark Material Handling Company

- Combilift

- Crown Equipment

- Doosan Corporation Industrial Vehicle

- Hangcha Group

- Hyster-Yale Materials Handling

- Hyundai Heavy Industries

- Jungheinrich AG

- KION Group AG

- Komatsu

- Manitou Group

- Mitsubishi Logisnext

- Toyota Industries

The Global Industrial Trucks Market was valued at USD 29.7 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 51.4 billion by 2035.

The rapid acceleration of e-commerce continues to reshape supply chains, pushing businesses to adopt faster and more efficient material-handling solutions. Rising online order volumes are driving companies to invest in large distribution hubs and smaller fulfillment sites to keep pace with expectations for rapid delivery. This increasing activity is elevating the need for forklifts, pallet trucks, and autonomous vehicles that support high-speed movement of goods throughout warehouse operations. As organizations prioritize quick internal transport and improved throughput, industrial trucks are becoming a vital competitive advantage in logistics environments. Advancements in warehouse automation including robotics, sensor-based systems, and integrated storage technologies are further propelling demand, as companies seek to optimize labor, maximize accuracy, and better utilize valuable warehouse space. This shift is particularly evident in dense urban markets, where automated processes are improving workflows and supporting higher productivity levels.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $29.7 Billion |

| Forecast Value | $51.4 Billion |

| CAGR | 5.6% |

The AGVs segment generated USD 10.9 billion in 2025. Automated guided vehicles operate independently using technologies such as laser-based navigation, induction systems, and imaging tools. These vehicles follow mapped routes and can modify their paths in real time, enabling safe and efficient transportation of materials throughout warehouses without the need for manual operation. Their ability to move pallets, containers, and other goods with consistency and precision has made them an integral part of modern material-handling environments.

The ICE segment held a 62% share in 2025. Internal combustion engine trucks remain heavily relied upon for demanding material-handling activities both indoors and outdoors. These vehicles, powered by diesel, gasoline, or LPG, are known for high torque and durability, making them suitable for industries that require lifting and transporting heavy loads under challenging conditions. Their performance capabilities are crucial in sectors including mining, large-scale manufacturing, and construction.

U.S. Industrial Trucks Market accounted for a 75% share and generated USD 6.3 billion in 2025. The expansion of warehouses, paired with the accelerated adoption of automation technologies, continues to drive strong demand across manufacturing, logistics, and e-commerce operations. Growing interest in electric-powered equipment and enhanced handling solutions reflects ongoing corporate sustainability goals and safety compliance requirements. The presence of major global original equipment manufacturers and significant investment in next-generation material-handling technologies positions the U.S. as a key center for innovation within the industrial trucks sector.

Major companies in the Industrial Trucks Market include Anhui Heli, BYD Company, Clark Material Handling Company, Combilift, Crown Equipment, Doosan Corporation Industrial Vehicle, Hangcha Group, Hyster-Yale Materials Handling, Hyundai Heavy Industries, Jungheinrich AG, KION Group AG, Komatsu, Manitou Group, Mitsubishi Logisnext, and Toyota Industries. Companies in the Industrial Trucks Market are strengthening their competitive position by expanding electric and automated product lines that support sustainability goals and reduce operating costs. Many manufacturers are integrating advanced telematics and fleet management systems to provide real-time data on performance, maintenance, and utilization. Continuous investment in autonomous technologies such as AGVs and semi-automated forklifts helps improve productivity and minimize reliance on manual labor. Firms are also diversifying their global production bases to improve supply stability and reduce lead times.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Propulsion

- 2.2.4 Operator type

- 2.2.5 End use industry

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 E-commerce expansion & warehouse automation

- 3.2.1.2 Adoption of Industry 4.0 technologies

- 3.2.1.3 Growth in manufacturing, construction, and logistics sectors

- 3.2.1.4 Labour shortages in developed markets

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High upfront costs & maintenance expenses

- 3.2.2.2 Supply chain disruptions & component shortages

- 3.2.3 Opportunities

- 3.2.3.1 Electric & zero-emission trucks

- 3.2.3.2 Automated guided vehicles (AGVs) & autonomous trucks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 AGVs

- 5.3 Hand, platform and pallet trucks

- 5.4 Order pickers

- 5.5 Pallet jacks

- 5.6 Side-loaders

- 5.7 Walkie stackers

Chapter 6 Market Estimates and Forecast, By Propulsion, 2021 - 2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric

Chapter 7 Market Estimates and Forecast, By Operator, 2021 - 2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Manual

- 7.3 Semi-automated

- 7.4 Fully automated

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.3 Automotive

- 8.4 Retail & e-commerce

- 8.5 Construction & mining

- 8.6 Manufacturing

- 8.7 Pharmaceuticals

- 8.8 Logistics & warehousing

- 8.9 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Anhui Heli

- 10.2 BYD Company

- 10.3 Clark Material Handling Company

- 10.4 Combilift

- 10.5 Crown Equipment

- 10.6 Doosan Corporation Industrial Vehicle

- 10.7 Hangcha Group

- 10.8 Hyster-Yale Materials Handling

- 10.9 Hyundai Heavy Industries

- 10.10 Jungheinrich AG

- 10.11 KION Group AG

- 10.12 Komatsu

- 10.13 Manitou Group

- 10.14 Mitsubishi Logisnext

- 10.15 Toyota Industries