|

시장보고서

상품코드

1892910

레이저 기술 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Laser Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

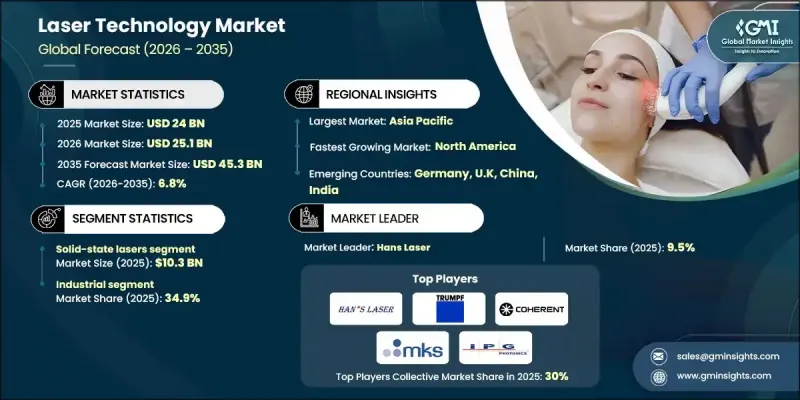

세계의 레이저 기술 시장은 2025년에 240억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 6.8%를 나타내 453억 달러에 이를 것으로 예측됩니다.

레이저가 제조, 통신, 방어, 의료, 자동차, 소비자용 전자기기 등 폭넓은 분야에서 필수적인 툴이 됨에 따라 이 업계의 성장은 가속화되고 있습니다. 정확성, 속도 및 자동화를 강화하는 능력은 특히 일관성과 정확성이 중요한 생산 환경에서보다 광범위한 채택을 지원했습니다. 산업 분야에서의 작업 부하 확대와 첨단 제조 공정에 대한 관심 증가가 레이저 기반 시스템 수요를 계속 견인하고 있습니다. 동시에 의료, 통신, 보안 관련 용도는 모두 큰 디지털 변혁을 경험하고 있으며, 고성능 레이저 플랫폼의 필요성을 더욱 향상시키고 있습니다. 레이저 설계의 진보와 조사 투자가 함께 산업 가공, 진단, 특수 용도에 새로운 가능성을 실현하고 있습니다. 이러한 첨단 광학 기술에 대한 의존도 증가는 향후 10년간 시장 전망이 견조하다는 것을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 가치 | 240억 달러 |

| 예측 금액 | 453억 달러 |

| CAGR | 6.8% |

고체 레이저 부문은 2025년에 103억 달러 시장 규모를 기록했으며 2035년까지 199억 달러에 이를 것으로 예측됩니다. 이러한 레이저는 높은 전력 효율, 내구성 및 의료 치료에서 과학 분석, 방어 기술에 이르기까지 다양한 용도에 대한 적응성을 통해 가장 널리 사용되는 솔루션 중 하나입니다. 정밀성이 필요한 작업을 지원하는 능력은 신뢰성과 정확성이 요구되는 광학 성능이 필수적인 환경에서 고체 레이저를 필수적인 존재로 하고 있습니다.

산업 분야는 2025년에 34.9%의 점유율을 차지하고, 절단, 마킹, 용접, 표면 처리, 드릴링 및 적층 성형에서 레이저의 광범위한 역할을 반영했습니다. 섬유, 자동차, 금속가공, 항공우주 등의 산업은 고도로 제어되고 재현성 있는 효율적인 작업을 위해 레이저 시스템에 크게 의존하고 있으며 산업용도가 레이저 기술 최대 소비 분야가 되고 있습니다.

미국의 레이저 기술 시장은 2024년에 74.9%의 점유율을 차지하며, 선진적인 제조 기술과 방어 분야에 초점을 맞춘 혁신에 대한 많은 투자를 지원했습니다. 연방 정부의 이니셔티브와 연구 프로그램은 정밀 가공, 제조 및 에너지 시스템 분야에서의 도입을 가속화하고 있습니다. 의료·미용 의료 분야의 성장도 시장에 공헌하고 있으며, 저침습 수술 수요 증가나 의료용 레이저 기기의 승인 확대가 배경에 있습니다. 병원 및 클리닉에서는 최신 진단 기술, 수술 치료 및 피부과 서비스를 지원하기 위해 레이저 플랫폼의 도입이 꾸준히 진행되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 이익률

- 각 단계별 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 산업 횡단적인 응용 분야의 확대

- 정밀도와 효율성에 대한 수요

- 통신 기술의 이용 확대

- 업계의 잠재적 위험 및 과제

- 기술적 복잡성

- 인지도와 보급도가 낮은

- 기회

- 의료·미용 분야에 있어서 응용 확대

- 산업 자동화 및 스마트 제조 분야에서의 확대

- 성장 촉진요인

- 성장 가능성 분석

- 향후 시장 동향

- 기술 및 혁신 현황

- 현재 기술 동향

- 신흥 기술

- 가격 동향

- 유형별

- 지역별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증기준

- 무역 통계

- 주요 수입국

- 주요 수출국

- 갭 분석

- 리스크 평가 및 경감책

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 파트너십 및 협력

- 신제품 출시

- 확대 계획

제5장 시장 추계·예측 : 유형별(2022-2035년)

- 고체 레이저

- 가스 레이저

- 액체 레이저

- 기타

제6장 시장 추계·예측 : 구성별(2022-2035년)

- 고정형

- 이동형

- 하이브리드

- 랙 통합 시스템

제7장 시장 추계·예측 : 출력 범위별(2022-2035년)

- 저전력(1kW 미만)

- 중출력(1-10 kW)

- 고출력(10kW 초과)

제8장 시장 추계·예측 : 파장별(2022-2035년)

- 적외선

- 가시광선

- 자외선

제9장 시장 추계·예측 : 용도별(2022-2035년)

- 레이저 가공

- 광통신

- 광전자 소자

- 기타

제10장 시장 추계·예측 : 최종 용도별(2022-2035년)

- 통신

- 산업용

- 반도체 및 전자

- 상업용

- 항공우주

- 기타

제11장 시장 추계·예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 프로파일

- AIDA

- Amada Press System

- Beckwood Press

- Bliss-Bret

- Bruderer

- Isgec Heavy Engineering

- Komatsu

- Macrodyne Technologies

- Nidec Minster

- Schuler Group

- Shieh Yih Machinery Industry

- SMS Group

- Stamtec

- Sutherland Presses

- Yangli Group

The Global Laser Technology Market was valued at USD 24 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 45.3 billion by 2035.

Growth in this industry is accelerating as lasers become essential tools across manufacturing, telecommunications, defense, healthcare, automotive, and consumer electronics. Their precision, speed, and ability to enhance automation have supported wider adoption, particularly in production environments where consistency and accuracy are critical. Expanding industrial workloads and rising interest in advanced fabrication processes continue to drive demand for laser-based systems. At the same time, healthcare, communications, and security-related applications are all experiencing significant digital transformation, further boosting the need for high-performance laser platforms. Advancements in laser design, combined with investments in research, are enabling new capabilities for industrial processing, diagnostics, and specialized applications. This increasing reliance on sophisticated optical technologies underscores the market's strong outlook over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $24 Billion |

| Forecast Value | $45.3 Billion |

| CAGR | 6.8% |

The solid-state lasers segment generated USD 10.3 billion in 2025 and is forecast to reach USD 19.9 billion by 2035. These lasers remain among the most widely used solutions due to their high power efficiency, durability, and suitability for diverse applications ranging from medical treatments to scientific analysis and defense technologies. Their ability to support precision-driven tasks makes them indispensable in environments that require reliable and accurate optical performance.

The industrial sector held a 34.9% share in 2025, reflecting the extensive role of lasers in cutting, marking, welding, surface treatment, drilling, and additive manufacturing. Industries such as textiles, automotive, metalworking, and aerospace depend heavily on laser systems for highly controlled, repeatable, and efficient operations, making industrial applications the largest consumer group for laser-based technologies.

U.S. Laser Technology Market held 74.9% share in 2024, supported by substantial investment in advanced manufacturing and defense-focused innovation. Federal initiatives and research programs have accelerated adoption across precision machining, fabrication, and energy systems. Growth in healthcare and aesthetic medicine also contributes to the market, with rising demand for minimally invasive procedures and expanded approvals for medical laser devices. Hospitals and clinics are consistently incorporating laser platforms to support modern diagnostics, surgical treatment, and dermatology services.

Key companies participating in the Global Laser Technology Market include AIDA, Beckwood Press, Bliss-Bret, Amada Press System, Bruderer, Komatsu, Nidec Minster, Macrodyne Technologies, Schuler Group, Shieh Yih Machinery Industry, SMS Group, Stamtec, Sutherland Presses, Yangli Group, and Isgec Heavy Engineering. Companies in the Global Laser Technology Market are adopting targeted strategies to reinforce their market position and expand global reach. Many are focusing on product innovation by developing lasers with higher power efficiency, improved beam quality, and compact architectures suitable for emerging industrial and medical applications. Strategic partnerships with manufacturing firms, research institutions, and technology integrators help accelerate the commercialization of next-generation laser systems. Firms are also investing in automation-ready platforms to support Industry 4.0 initiatives, enhancing compatibility with robotics, AI-driven monitoring, and smart factory environments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Configuration

- 2.2.4 Application

- 2.2.5 Power Range

- 2.2.6 Wavelength

- 2.2.7 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing applications across industries

- 3.2.1.2 Demand for precision and efficiency

- 3.2.1.3 Rising use in communication technology

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Technical complexity

- 3.2.2.2 Limited awareness and adoption

- 3.2.3 Opportunities

- 3.2.3.1 Growth in medical & aesthetic applications

- 3.2.3.2 Expansion in industrial automation & smart manufacturing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By Type

- 3.6.2 By Region

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Gap analysis

- 3.10 Risk assessment and mitigation

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022-2035 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Solid-state lasers

- 5.3 Gas lasers

- 5.4 Liquid lasers

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Configuration, 2022-2035 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Fixed

- 6.3 Moving

- 6.4 Hybrid

- 6.5 Rack-integrated systems

Chapter 7 Market Estimates & Forecast, By Power range, 2022-2035 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Low Power (<1 kW)

- 7.3 Medium Power (1-10 kW)

- 7.4 High Power (>10 kW)

Chapter 8 Market Estimates & Forecast, By Wavelength, 2022-2035 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Infrared

- 8.3 Visible

- 8.4 Ultraviolet

Chapter 9 Market Estimates & Forecast, By Application, 2022-2035 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Laser processing

- 9.3 Optical communication

- 9.4 Optoelectronic devices

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By End Use, 2022-2035 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 Telecommunication

- 10.3 Industrial

- 10.4 Semiconductor & Electronics

- 10.5 Commercial

- 10.6 Aerospace

- 10.7 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022-2035 (USD Million) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 France

- 11.3.3 UK

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 AIDA

- 12.2 Amada Press System

- 12.3 Beckwood Press

- 12.4 Bliss-Bret

- 12.5 Bruderer

- 12.6 Isgec Heavy Engineering

- 12.7 Komatsu

- 12.8 Macrodyne Technologies

- 12.9 Nidec Minster

- 12.10 Schuler Group

- 12.11 Shieh Yih Machinery Industry

- 12.12 SMS Group

- 12.13 Stamtec

- 12.14 Sutherland Presses

- 12.15 Yangli Group