|

시장보고서

상품코드

1892913

자전거 컴퓨터 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Bike Computer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

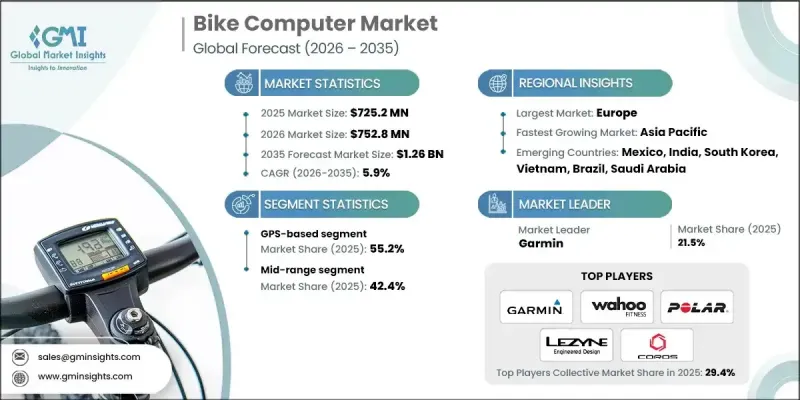

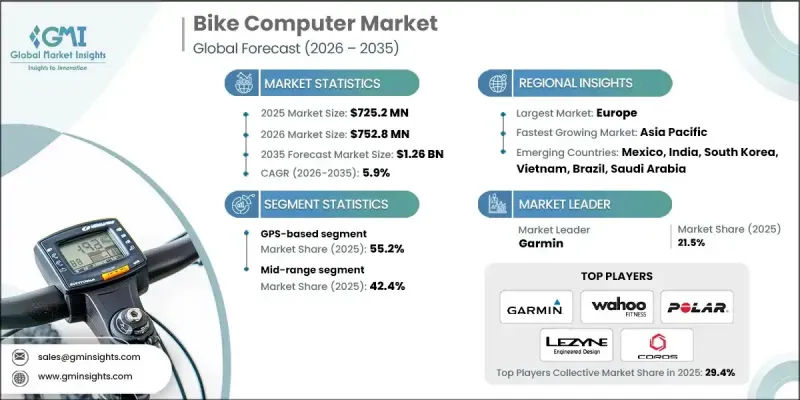

세계의 자전거 컴퓨터 시장은 2025년에 7억 2,520만 달러로 평가되었으며, 2035년까지 CAGR 5.9%로 성장하여 12억 6,000만 달러에 달할 것으로 예측됩니다.

개인의 건강 증진에 대한 관심이 높아지고 일상 생활에 기술이 통합되면서 속도, 케이던스, 심박수 및 기타 성능 지표를 추적하는 기기에 대한 수요는 계속 증가하고 있습니다. 자전거 타기는 전 세계 건강 지향적인 사람들 사이에서 선호되는 활동으로 자리 잡았습니다. 특히 당뇨병, 심장병, 체중 관리 등 생활습관병과 관련된 우려로 인해 사람들이 더 활동적인 습관을 가지게 되었기 때문입니다. 또한, 여러 지역 정부에서 탄소배출량 감소와 교통체증 완화를 목적으로 자전거 타기를 장려하고 있는 만큼, 환경에 대한 배려도 큰 역할을 하고 있습니다. 디지털 시스템의 발전과 모빌리티 애플리케이션에서 AI와 머신러닝의 역할이 확대됨에 따라 보다 스마트하고 직관적인 자전거 컴퓨터가 시장에 등장하고 그 매력은 더욱 커질 것으로 예상됩니다. 사이클링 이벤트와 공공 건강 증진 프로그램의 확산은 훈련 및 성능 모니터링을 강화하는 기기의 사용을 더욱 촉진하고 있습니다. 피트니스 기술에 대한 전 세계의 관심이 지속적으로 증가함에 따라, 연결성과 지능을 갖춘 자전거 컴퓨터에 대한 전반적인 수요는 가속화될 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 시작 가치 | 7억 2,520만 달러 |

| 예측 금액 | 12억 6,000만 달러 |

| CAGR | 5.9% |

GPS 탑재 부문은 2024년 55.2%의 점유율을 차지했습니다. 이 장치들은 기존의 내비게이션 도구를 훨씬 뛰어넘어 사이클리스트가 원하는 상세한 주행 데이터를 실시간으로 제공합니다. 뛰어난 지도 기능으로 GPS가 탑재되지 않은 제품에 비해 우선적으로 선택되고 있으며, 레크리에이션, 출퇴근, 운동 목적으로 전 세계적으로 자전거를 타는 인구가 증가하고 있는 추세와 일치합니다. 소비자의 기대가 높아지면서 라이더들은 거리, 속도 및 관련 지표에 대한 보다 정확한 추적을 지속적으로 요구하고 있습니다.

고가형 자전거 컴퓨터 부문은 AI 강화 분석 기능, 고급 건강 관리 기능, 스마트 배터리 최적화 기능 등의 특징으로 인해 2034년까지 CAGR 7.1%로 성장할 것으로 예상됩니다. 각 브랜드는 사용자 선호 트렌드에 초점을 맞추고, 제품 라인의 정교화와 통합 기능의 확장을 추진하고 있습니다. 이 부문은 가처분 소득 증가로 인해 기능이 향상된 고급 모델을 선택하는 구매자가 증가함에 따라 혜택을 누리고 있습니다.

미국 자전거 컴퓨터 시장은 커넥티드 사이클링 기술의 급속한 성장과 자전거 이용자 증가에 힘입어 2025년 1억 8,520만 달러 규모에 달했습니다. 여러 기업들이 차세대 기능 도입과 제품 혁신의 기준 설정을 통해 국내 트렌드 형성에 지속적으로 영향을 미치고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 비용 구조

- 각 단계의 부가가치

- 밸류체인에 영향을 미치는 요인

- 디스럽션

- 업계에 대한 영향요인

- 성장 촉진요인

- 세계의 사이클링 참여율 증가와 건강 의식 동향

- 전동 어시스트 자전거 시장 확대와 통합 디스플레이 수요

- 프로 사이클링의 영향력과 UCI 월드 투어의 기술 채용

- 스마트 시티 인프라 개발과 자전거 이용의 통합

- 업계의 잠재적 리스크와 과제

- 스마트폰 대체의 위협과 무료 앱 대체안

- 도시 시장의 도난 리스크와 디바이스 보안에 대한 우려

- 시장 기회

- 신흥 시장에 대한 침투

- 전동 어시스트 자전거의 통합과 OEM 파트너십 확대

- 그래블 & 어드벤처 사이클링 부문 확대

- 스마트 시티 및 자치체용 자전거 데이터 플랫폼 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porters 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 기술 로드맵과 진화

- 기술 도입 수명주기 분석

- 가격 동향

- 지역별

- 제품별

- 특허 분석

- 스마트 시티·인프라 통합

- 교통 관리를 위한 자전거 감지 기술

- 자전거 컴퓨터와 교통 인프라 제휴

- 자치체용 자전거 데이터 플랫폼

- 제조업체 님용 스마트 시티 제휴 기회

- 센서 생태계와 액세서리 시장

- 센서 시장 개요와 매출 기여도

- 속도 및 주행 속도 센서

- 심박수 모니터

- 파워 미터

- 신흥 센서 카테고리

- 소비자 행동과 구매 의사결정 분석

- 구입 결정요인과 기능 우선순위 지정

- 브랜드 로열티와 환승 행동 패턴

- 프로 사이클링 및 운동선수 기용 광고의 영향

- 온라인 구입과 점포 구입 기호 비교

- 소비자 동향과 기호의 변화

- 터치스크린과 버튼식 인터페이스 전환 동향

- 내비게이션 기능의 중요성 증가

- 스마트폰 제휴에 대한 기대

- 구입의 중요한 결정요인으로서의 배터리 수명

- 소매 채널 동향과 유통 전략

- 전문 자전거 소매 시장 점유율과 동향

- 온라인 직접 소비자용 판매(DTC) 성장

- 대중 시장 소매로의 침투

- 자전거 구입시 OEM 번들링

- 제품수명주기와 사용 패턴 분석

- 제품 평균수명과 내구성

- 펌웨어 업데이트 빈도와 장기 서포트

- 사용자 부문별 사용 빈도

- 계절에 의한 사용 상황의 변화와 기후의 영향

- 향후 전망과 기회

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병

- 제휴·협업

- 신제품 발매

- 확대 계획과 자금 조달

- 벤더 선정 기준

제5장 시장 추정 및 예측 : 제품별, 2022-2035

- 유선

- 무선

- GPS 기반

- 태양광발전

- 기타

제6장 시장 추정 및 예측 : 가격대별, 2022-2035

- 기본

- 중가격대

- 프리미엄

제7장 시장 추정 및 예측 : 센서별, 2022-2035

- 리어 휠 센서

- 속도/케이던스 센서

- 구배 센서

- 심박수 센서

제8장 시장 추정 및 예측 : 접속 방식별, 2022-2035

- Bluetooth

- Wi-Fi

- ANT+

- 기타

제9장 시장 추정 및 예측 : 자전거별, 2022-2035

- 산악 자전거

- 로드 자전거

- 도시형 자전거

- 전기자전거

- 그래블 자전거

제10장 시장 추정 및 예측 : 유통 채널별, 2022-2035

- 온라인

- 오프라인

제11장 시장 추정 및 예측 : 용도별, 2022-2035

- 육상 경기 및 스포츠

- 피트니스 및 통근

- 레크리에이션/레저

제12장 시장 추정 및 예측 : 최종 용도별, 2022-2035

- 개인소비자

- 자전거 렌탈/플릿 사업자

- 프로페셔널 팀/클럽

제13장 시장 추정 및 예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 베네룩스

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ANZ

- 싱가포르

- 말레이시아

- 인도네시아

- 베트남

- 태국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

제14장 기업 개요

- 세계 기업

- Garmin

- Wahoo Fitness

- Polar Electro Oy

- Hammerhead

- Stages Cycling

- Lezyne

- 지역 기업

- SIGMA

- Bryton

- CatEye

- Giant Manufacturing

- Specialized Bicycle Components

- Bosch eBike Systems

- Shimano

- Mio Technology

- 신흥 기업

- Coospo

- iGPSPORT

- Magene

- Coros

- Suunto

- Omata

- Beeline

- Xplova

- Cycplus

- Trek Bicycle Corporation

- Cannondale

The Global Bike Computer Market was valued at USD 725.2 million in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 1.26 billion by 2035.

Growing interest in personal fitness and increasing integration of technology into everyday routines continue to elevate demand for devices that track speed, cadence, heart rate, and other performance indicators. Cycling has become a preferred activity for health-conscious individuals around the world, especially as concerns linked to lifestyle-related conditions, including diabetes, heart complications, and weight management, drive people toward more active habits. Environmental priorities also play a major role, as governments across multiple regions promote cycling to help lower carbon emissions and ease traffic congestion. Advancements in digital systems and the expanding role of AI and machine learning across mobility applications are expected to bring smarter, more intuitive bike computers to the market, strengthening their appeal. The growing adoption of cycling events and public wellness programs further supports the use of devices that enhance training and performance monitoring. As global awareness around fitness technology continues to rise, the overall demand for connected and intelligent bike computers is expected to accelerate.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $725.2 Million |

| Forecast Value | $1.26 Billion |

| CAGR | 5.9% |

The GPS-based segment held a 55.2% share in 2024. These devices have evolved far beyond earlier navigation tools and now provide detailed ride metrics that cyclists expect in real time. Their superior mapping capabilities make them the preferred choice compared with non-GPS alternatives, aligning with the worldwide growth of cycling for recreation, commuting, and exercise. As consumer expectations increase, riders consistently seek more accurate tracking of distance, speed, and related metrics.

The premium-priced bike computers segment will grow at a CAGR of 7.1% by 2034, owing to features such as AI-enhanced analytics, advanced health tracking, and smart battery optimization. Brands are concentrating on user preference trends to refine their offerings and introduce more integrated functions. This segment benefits from rising disposable incomes as buyers increasingly choose higher-end devices with extended capabilities.

U.S Bike Computer Market reached USD 185.2 million in 2025, supported by rapid growth in connected cycling technologies and an expanding population of bicycle users. Several companies continue to influence trends in the country by introducing next-generation features and setting benchmarks in product innovation.

Leading companies in the Bike Computer Market include Bryton, CatEye, COROS Wearables, Garmin, Hammerhead, Lezyne, Magene, Polar, Sigma, and Wahoo Fitness. Manufacturers in the bike computer industry are strengthening their market foothold by emphasizing innovation in data analytics, connectivity, and sensor technology. Many companies are deepening the integration of AI-driven insights to offer more accurate performance tracking and personalized ride analysis. Expanding product ecosystems through companion apps and wireless accessories helps brands build long-term engagement with cyclists. Firms are also focusing on lightweight designs, improved battery efficiency, and enhanced durability to appeal to both recreational and performance-oriented users. Strategic partnerships with cycling communities and professional teams help boost brand visibility, while targeted investments in premium product lines cater to consumers shifting toward high-end devices.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Price Range

- 2.2.4 Sensor

- 2.2.5 Connectivity

- 2.2.6 Bike

- 2.2.7 Distribution Channel

- 2.2.8 Application

- 2.2.9 End Use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Global cycling participation growth & health consciousness trends

- 3.2.1.2 E-bike market expansion & integrated display demand

- 3.2.1.3 Professional cycling influence & UCI worldtour technology adoption

- 3.2.1.4 Smart city infrastructure development & cycling integration

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Smartphone substitution threat & free app alternatives

- 3.2.2.2 Theft risk & device security concerns in urban markets

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging market penetration

- 3.2.3.2 E-bike integration & OEM partnership expansion

- 3.2.3.3 Gravel & adventure cycling segment expansion

- 3.2.3.4 Smart city & municipal cycling data platform integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.7.3 Technology roadmaps & evolution

- 3.7.4 Technology adoption lifecycle analysis

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Patent analysis

- 3.10 Smart city & infrastructure integration

- 3.10.1 Bicycle detection technologies for traffic management

- 3.10.2 Bike computer integration with traffic infrastructure

- 3.10.3 Municipal cycling data platforms

- 3.10.4 Smart city partnership opportunities for manufacturers

- 3.11 Sensor ecosystem & accessory market

- 3.11.1 Sensor market overview & revenue contribution

- 3.11.2 Speed & cadence sensors

- 3.11.3 Heart rate monitors

- 3.11.4 Power meters

- 3.11.5 Emerging sensor categories

- 3.12 Consumer behavior & purchase decision analysis

- 3.12.1 Purchase decision factors & feature prioritization

- 3.12.2 Brand loyalty & switching behavior patterns

- 3.12.3 Influence of professional cycling & athlete endorsements

- 3.12.4 Online vs in-store purchase preferences

- 3.13 Consumer trends & preference evolution

- 3.13.1 Shift toward touchscreen vs button interfaces

- 3.13.2 Navigation feature importance growth

- 3.13.3 Smartphone integration expectations

- 3.13.4 Battery life as critical purchase factor

- 3.14 Retail channel dynamics & distribution strategies

- 3.14.1 Specialty cycling retail market share & trends

- 3.14.2 Online direct-to-consumer (DTC) growth

- 3.14.3 Mass market retail penetration

- 3.14.4 OEM bundling with bicycle purchases

- 3.15 Product lifecycle & usage pattern analysis

- 3.15.1 Average product lifespan & durability

- 3.15.2 Firmware update frequency & long-term support

- 3.15.3 Usage intensity by user segment

- 3.15.4 Seasonal usage variations & weather impact

- 3.16 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Vendor selection criteria

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Wired

- 5.3 Wireless

- 5.4 GPS-based

- 5.4.1 Solar-powered

- 5.4.2 Others

Chapter 6 Market Estimates & Forecast, By Price Range, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Basic

- 6.3 Mid-range

- 6.4 Premium

Chapter 7 Market Estimates & Forecast, By Sensor, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Rear Wheel Sensor

- 7.3 Speed/Cadence Sensor

- 7.4 Gradient Sensor

- 7.5 Heart Rate Sensor

Chapter 8 Market Estimates & Forecast, By Connectivity, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Bluetooth

- 8.3 Wi-Fi

- 8.4 ANT+

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Bike, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Mountain bike

- 9.3 Road bike

- 9.4 Urban bike

- 9.5 E-bike

- 9.6 Gravel bike

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 Online

- 10.3 Offline

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 Athletics & sports

- 11.3 Fitness & commuting

- 11.4 Recreational/leisure

Chapter 12 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn, Units)

- 12.1 Key trends

- 12.2 Individual consumers

- 12.3 Bike rental/fleet operators

- 12.4 Professional teams/clubs

Chapter 13 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 US

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.3.6 Russia

- 13.3.7 Nordics

- 13.3.8 Benelux

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 South Korea

- 13.4.5 ANZ

- 13.4.6 Singapore

- 13.4.7 Malaysia

- 13.4.8 Indonesia

- 13.4.9 Vietnam

- 13.4.10 Thailand

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.5.4 Colombia

- 13.6 MEA

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Global companies

- 14.1.1 Garmin

- 14.1.2 Wahoo Fitness

- 14.1.3 Polar Electro Oy

- 14.1.4 Hammerhead

- 14.1.5 Stages Cycling

- 14.1.6 Lezyne

- 14.2 Regional companies

- 14.2.1 SIGMA

- 14.2.2 Bryton

- 14.2.3 CatEye

- 14.2.4 Giant Manufacturing

- 14.2.5 Specialized Bicycle Components

- 14.2.6 Bosch eBike Systems

- 14.2.7 Shimano

- 14.2.8 Mio Technology

- 14.3 Emerging companies

- 14.3.1 Coospo

- 14.3.2 iGPSPORT

- 14.3.3 Magene

- 14.3.4 Coros

- 14.3.5 Suunto

- 14.3.6 Omata

- 14.3.7 Beeline

- 14.3.8 Xplova

- 14.3.9 Cycplus

- 14.3.10 Trek Bicycle Corporation

- 14.3.11 Cannondale