|

시장보고서

상품코드

1913285

포장 기계 시장 : 기회, 성장요인, 업계동향 분석 예측(2026-2035년)Packaging Machinery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

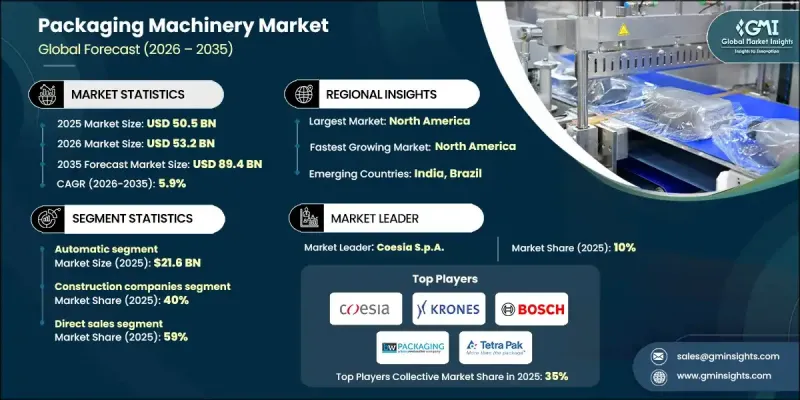

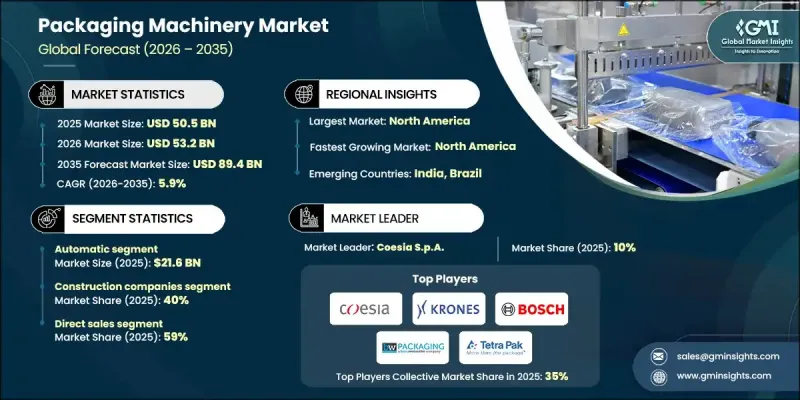

세계 포장 기계 시장은 2025년에 505억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 5.9%로 성장하여 894억 달러에 이를 것으로 예측됩니다.

포장 기계는 현재 생산 속도 향상, 제품 품질 유지, 규제 준수, 환경 부하 저감을 지원하는 중요한 역할을 담당하고 있습니다. 제조업자는 지속가능성 목표와 업무 효율화 목표를 달성하면서 대규모 일관된 품질 제공을 요구하는 압력이 높아지고 있습니다. 자동 포장 솔루션은 높은 정밀도, 위생 관리 개선 및 국제 표준 준수를 보장하기 위해 이러한 노력의 핵심입니다. 생산량이 증가하고 공급망이 복잡해짐에 따라 기업은 안전한 밀봉과 효율적인 처리를 보장하기 위해 첨단 포장 시스템에 대한 의존도를 높이고 있습니다. 생산성과 환경 책임을 양립시키는 혁신으로 업계는 변화를 계속하고 있습니다. 자동화, 디지털화 및 재료 최적화에 대한 투자는 여러 산업 워크플로우에서 포장 기계의 중요성을 더욱 강화하고 있습니다. 시장의 성장 궤도는 현대의 제조 요구를 지원하는 신뢰할 수 있고 확장 가능하며 미래를 향한 포장 솔루션에 대한 수요 증가를 반영합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 금액 | 505억 달러 |

| 예측 금액 | 894억 달러 |

| CAGR | 5.9% |

포장 기계 제조업체는 디지털 제어 및 센서 기반 모니터링을 통해 지능형 기능을 통합하고 가동 시간과 작동 속도를 향상시키기 위해 적극적으로 장비 재 설계를 진행하고 있습니다. 지속가능성은 옵션기능이 아니라 기본적 가치가 되어 폐기물 발생을 삭감하면서 환경에 배려한 소재를 처리할 수 있도록 기계가 설계되어 있습니다. 이러한 발전은 환경 친화적인 생산 방법에 대한 수요 증가에 직접적으로 대응합니다.

2025년 자동화 시스템 분야는 216억 달러 시장 규모를 창출했습니다. 자동화는 일관성을 높이고 인적 개입을 제한하며 오류율을 크게 줄입니다. 이러한 시스템은 대규모 생산을 가능하게 하는 동시에 연포장 형식을 실현하여 신속한 납기 대응과 운영 신뢰성의 향상을 지원합니다. 연결 기술의 채택은 예지 보전, 실시간 시각화, 데이터 구동형의 효율 개선을 가능하게 하고, 장기 비용 절감으로 이어져 수요를 더욱 가속화하고 있습니다.

2025년 직접 판매 부문의 점유율은 59%를 차지하며 제조업체와 고객의 직접 거래가 강하게 선호되는 경향을 반영합니다. 이 접근법은 특히 대량 생산 작업에서 맞춤형 시스템 구성, 신속한 배포 및 강력한 서비스 모니터링을 지원합니다. 직접 채널은 가격 설정의 자유도 향상과 판매 후 지원 강화도 실현합니다.

미국 포장 기계 시장은 2025년에 71%의 점유율을 차지했고, 126억 달러의 규모가 되었습니다. 이 지역은 첨단 인프라, 광범위한 자동화 도입 및 스마트 제조에 대한 강력한 투자의 혜택을 누리고 있습니다. 온라인 소매 활동의 확대와 소비재·음료 제조업체로부터의 안정된 수요가, 고속 시스템의 도입을 계속적으로 견인하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 수익률

- 단계별 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 자동화 및 효율성에 대한 수요 증가

- 전자상거래(E커머스)와 소비재(CPG)의 성장

- 기술 진보와 스마트 포장의 통합

- 업계의 잠재적 위험 및 과제

- 높은 초기 자본 투자 비용

- 보수의 복잡성과 숙련 노동력의 부족

- 기회

- 지속가능성과 친환경 포장 솔루션

- 신흥국 시장에서의 확대

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술과 혁신 동향

- 현재의 기술 동향

- 신규 기술

- 가격 동향

- 지역별

- 기기별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 기기유형별, 2022-2025

- 충전 및 정량 주입 설비

- 용적식 충전기

- 중량식 충전기

- 액체 충전기

- 분말 충전기

- 백 포장 및 연포장 설비

- 수직형 포장기(VFFS)

- 수평형 포장기(HFFS)

- 기성백 충전 및 실링 설비

- 파우치 성형 및 충전 설비

- 제품 포장 장비

- 카토닝, 케이스 패킹 및 멀티패킹 설비

- 수평 카토너

- 수직 카토너

- 랩어라운드 케이스 패커

- 트레이 성형기

- 수축 번들러 및 멀티팩 포장기

- 라벨링, 코딩 및 마킹 기기

- 점착 라벨러

- 핫멜트 및 냉풀 라벨러

- 슬리브 라벨러

- 잉크젯 및 레이저 코더

- 열전사 프린터

- 팔레타이징 및 엔드오브라인 설비

- 로봇 팔레타이저

- 일반 팔레타이저

- 팔레트 스트레치 래퍼

- 팔레트 수축 래퍼

- 결속기

- 케이스 실러

- 이송, 공급 및 핸들링 설비

- 벨트 컨베이어 및 롤러 컨베이어

- 집적 테이블

- 제품 공급기 및 선별기

- 로봇 픽앤플레이스 시스템

- 검사 및 품질 관리 기기

- 중량 검사기

- 금속 감지기 및 X선 검사 장비

- 비전 검사 시스템

- 누설 검사기

- 캡핑 및 밀봉 설비

- 스크류 캐퍼

- 스냅캡과 크림퍼

- 시머 및 유도 씰링 기계

- 벌크백 및 FIBC 취급 기기

- 벌크백 충전기

- Fibc 배출기

- 기타 기기 유형

- 블리스터 포장기

- 용기 성형 및 블로우 몰딩

- 무균 포장 시스템

제6장 시장 추정 및 예측 : 자동화 레벨별, 2022-2025

- 수동

- 반자동

- 전자동

제7장 시장 추정 및 예측 : 최종 용도별, 2022-2025

- 식음료

- 신선식품 및 냉동식품

- 드라이 푸드 스낵

- 음료

- 유제품

- 의약품 및 의료기기

- 정제 및 캡슐

- 주사제 및 바이오의약품

- 의료기기 및 진단기기

- 뉴트라슈티컬

- 퍼스널케어 및 화장품

- 스킨케어 및 헤어케어

- 화장품 및 색조

- 위생용품 및 생활위생 제품

- 가정용, 공업용 및 농업용 화학제품

- 세제 및 클리너

- 비료 및 농약

- 산업용 화학제품

- 반려동물 식품 및 동물 영양

- 건식 반려동물 식품

- 습식 반려동물 식품

- 간식 및 보충제

- 가축 사료

- 기타

제8장 시장추정 및 예측 : 유통채널별, 2022-2025

- 직접 판매

- 간접 판매

제9장 시장 추정 및 예측 : 지역별, 2022-2025

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- ARBURG GmbH Co KG

- Barry-Wehmiller(BW Packaging)

- Coesia SpA

- ENGEL Holding GmbH

- Fres-co System USA, Inc.

- Ilapak International SA

- Ishida Co., Ltd.

- KraussMaffei Group GmbH

- Krones AG

- MULTIVAC Sepp Haggenmuller SE &Co. KG

- Robert Bosch Packaging Technology

- Rovema GmbH

- Sumitomo Heavy Industries, Ltd.

- Tetra Pak International SA

- Yamato Scale Co., Ltd

The Global Packaging Machinery Market is valued at USD 50.5 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 89.4 billion by 2035.

Packaging machinery now plays a critical role in supporting faster output, improved product integrity, regulatory adherence, and lower environmental impact. Manufacturers face increasing pressure to deliver consistent quality at scale while meeting sustainability targets and operational efficiency goals. Automated packaging solutions remain central to these efforts, as they deliver high precision, improved sanitation, and reliable compliance with global standards. As manufacturing volumes rise and supply chains become more complex, companies increasingly rely on advanced packaging systems to ensure secure sealing and efficient processing. The industry continues to transform through innovation that aligns productivity with environmental responsibility. Investments in automation, digitalization, and material optimization reinforce the importance of packaging machinery across multiple industrial workflows. The market's growth trajectory reflects rising demand for dependable, scalable, and future-ready packaging solutions that support modern manufacturing needs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $50.5 Billion |

| Forecast Value | $89.4 Billion |

| CAGR | 5.9% |

Packaging machinery producers are actively redesigning equipment to integrate intelligent functionality through digital controls and sensor-based monitoring, improving uptime and operational speed. Sustainability has become a foundational value rather than an optional feature, with machines engineered to handle eco-conscious materials while reducing waste generation. These advancements respond directly to rising demand for environmentally responsible production methods.

In 2025, the automatic systems segment generated USD 21.6 billion. Automation enhances consistency, limits human intervention, and significantly lowers error rates. These systems enable large-scale production while allowing flexible packaging formats, supporting faster turnaround times and improved operational reliability. The adoption of connected technologies further accelerates demand by enabling predictive servicing, real-time visibility, and data-driven efficiency improvements that lower long-term costs.

The direct sales segment accounted for a 59% share in 2025, reflecting a strong preference for manufacturer-to-client engagement. This approach supports tailored system configurations, faster implementation, and stronger service oversight, particularly for high-volume operations. Direct channels also enable greater pricing control and enhanced post-sale support.

United States Packaging Machinery Market held a 71% share in 2025, generating USD 12.6 billion. The region benefits from advanced infrastructure, widespread automation adoption, and strong investment in smart manufacturing. Expanding online retail activity and steady demand from consumer goods and beverage producers continue to drive high-speed system adoption.

Leading companies active in the Global Packaging Machinery Market include Tetra Pak International S.A., Krones AG, Coesia S.p.A., MULTIVAC Sepp Haggenmuller SE & Co. KG, Barry-Wehmiller, Ishida Co., Ltd., Yamato Scale Co., Ltd., Robert Bosch Packaging Technology, Ilapak International SA, Rovema GmbH, Fres-co System USA, Inc., ENGEL Holding GmbH, KraussMaffei Group GmbH, ARBURG GmbH + Co KG, Sumitomo Heavy Industries Ltd., and JSW Plastics Machinery Co., Ltd. Companies operating in the Global Packaging Machinery Market reinforce their competitive position through continuous innovation, automation expansion, and sustainability-driven design. Strategic investments in digital technologies improve machine intelligence, predictive maintenance, and system efficiency. Manufacturers focus on modular designs to enable customization while reducing deployment time. Global players strengthen distribution networks and after-sales services to enhance customer retention. Sustainability initiatives, including waste reduction and material compatibility, support compliance with environmental regulations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Automation

- 2.2.4 End-user industry

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for automation and efficiency

- 3.2.1.2 Growth of e-commerce and consumer packaged goods (CPG)

- 3.2.1.3 Technological advancements and smart packaging integration

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital investment

- 3.2.2.2 Complexity in maintenance and skilled workforce shortage

- 3.2.3 Opportunities

- 3.2.3.1 Sustainability and eco-friendly packaging solutions

- 3.2.3.2 Expansion in developing economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By Region

- 3.6.2 By Equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2022 - 2025 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Filling & dosing equipment

- 5.2.1 Volumetric fillers

- 5.2.2 Gravimetric fillers

- 5.2.3 Liquid fillers

- 5.2.4 Powder fillers

- 5.3 Bagging & flexible packaging equipment

- 5.3.1 Vertical form-fill-seal (vffs)

- 5.3.2 Horizontal form-fill-seal (hffs)

- 5.3.3 Pre-made bag filling & sealing

- 5.3.4 Pouch making & filling

- 5.3.5 Product wrapping equipment

- 5.4 Cartoning, case packing & multipacking equipment

- 5.4.1 Horizontal cartoners

- 5.4.2 Vertical cartoners

- 5.4.3 Wraparound case packers

- 5.4.4 Tray formers

- 5.4.5 Shrink bundlers and multipack wrappers

- 5.5 Labeling, coding & marking equipment

- 5.5.1 Pressure-sensitive labelers

- 5.5.2 Hot-melt and cold-glue labelers

- 5.5.3 Sleeve labelers

- 5.5.4 Inkjet and laser coders

- 5.5.5 Thermal transfer printers

- 5.6 Palletizing & end-of-line equipment

- 5.6.1 Robotic palletizers

- 5.6.2 Conventional palletizers

- 5.6.3 Pallet stretch wrappers

- 5.6.4 Pallet shrink wrappers

- 5.6.5 Strapping machines

- 5.6.6 Case sealers

- 5.7 Conveying, feeding & handling equipment

- 5.7.1 Belt and roller conveyors

- 5.7.2 Accumulation tables

- 5.7.3 Product feeders and sorters

- 5.7.4 Robotic pick-and-place

- 5.8 Inspection & quality control equipment

- 5.8.1 Checkweighers

- 5.8.2 Metal detectors and x-ray inspection

- 5.8.3 Vision inspection systems

- 5.8.4 Leak testers

- 5.9 Capping & closing equipment

- 5.9.1 Screw cappers

- 5.9.2 Snap cappers and crimpers

- 5.9.3 Seamers and induction sealers

- 5.10 Bulk bag & fibc handling equipment

- 5.10.1 Bulk bag fillers

- 5.10.2 Fibc dischargers

- 5.11 Other equipment types

- 5.11.1 Blister packaging machines

- 5.11.2 Bottle blowing and molding

- 5.11.3 Aseptic packaging systems

Chapter 6 Market Estimates and Forecast, By Automation, 2022 - 2025 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automatic

- 6.4 Fully automatic

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2025 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.2.1 Fresh & frozen foods

- 7.2.2 Dry foods & snacks

- 7.2.3 Beverages

- 7.2.4 Dairy

- 7.3 Pharmaceuticals & medical devices

- 7.3.1 Tablets and capsules

- 7.3.2 Injectables and biologics

- 7.3.3 Medical devices and diagnostics

- 7.3.4 Nutraceuticals

- 7.3.5 Personal care & cosmetics

- 7.3.6 Skincare and haircare

- 7.3.7 Cosmetics and color

- 7.3.8 Toiletries and hygiene products

- 7.4 Household, industrial & agricultural chemicals

- 7.4.1 Detergents and cleaners

- 7.4.2 Fertilizers and pesticides

- 7.4.3 Industrial chemicals

- 7.5 Pet food & animal nutrition

- 7.5.1 Dry pet food

- 7.5.2 Wet pet food

- 7.5.3 Treats and supplements

- 7.5.4 Animal feed

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2025 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2025 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ARBURG GmbH + Co KG

- 10.2 Barry-Wehmiller (BW Packaging)

- 10.3 Coesia S.p.A.

- 10.4 ENGEL Holding GmbH

- 10.5 Fres-co System USA, Inc.

- 10.6 Ilapak International SA

- 10.7 Ishida Co., Ltd.

- 10.8 KraussMaffei Group GmbH

- 10.9 Krones AG

- 10.10 MULTIVAC Sepp Haggenmuller SE & Co. KG

- 10.11 Robert Bosch Packaging Technology

- 10.12 Rovema GmbH

- 10.13 Sumitomo Heavy Industries, Ltd.

- 10.14 Tetra Pak International S.A.

- 10.15 Yamato Scale Co., Ltd