|

시장보고서

상품코드

1913344

텅스텐 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Tungsten Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

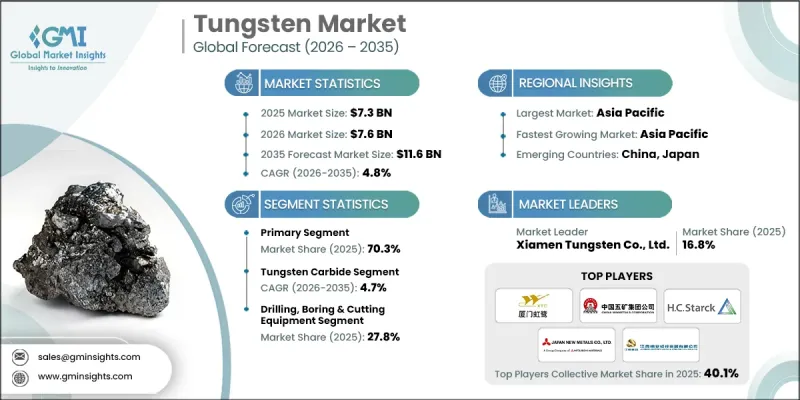

세계의 텅스텐 시장은 2025년에 73억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.8%로 성장할 전망이며, 116억 달러에 이를 것으로 예측됩니다.

비용 효율성, 규제 압력 및 장기적인 재료 안보의 필요성으로 인해 순환 경제의 실천이 공급망 전체에 침투함에 따라 시장은 구조적 변화를 겪고 있습니다. 회수 기술의 발전에 의해 2차 텅스텐이 1차 원료와 동등한 화학적 순도, 결정 구조, 성능 안정성을 달성할 수 있게 됨으로써, 재활용은 전략적 중요성을 늘리고 있습니다. 현대의 열적 및 화학적 재활용 공정은 기존의 채굴 및 정련에 비해 에너지 사용량과 배출량을 대폭 삭감하면서 높은 회수율을 실현합니다. 이러한 개선은 특히 에너지 가격과 탄소 관련 비용이 높은 지역에서 재생 텅스텐의 경제적 합리성을 강화하고 있습니다. 동시에 1차 자원의 지정학적 집중은 시장 동향에 계속 영향을 미치며 대체 조달 경로의 다양화와 투자를 촉진하고 있습니다. 첨단 제조, 산업용 공구, 고성능 재료 용도에서의 수요 증가가 지속적으로 시장 확대를 지원하는 한편, 지속가능성을 중시한 조달 방침은 세계의 최종 이용 산업 전체에서 장기적인 성장 가능성을 더욱 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 시 가치 | 73억 달러 |

| 예측 금액 | 116억 달러 |

| CAGR | 4.8% |

2025년에는 주로 울프라마이트 광석 및 실라이트 광석으로부터 채굴 및 정광 생산에 지원되었으며, 1차 텅스텐 부문이 70.3%의 점유율을 차지했습니다. 생산은 지리적으로 고도로 집중된 상태가 계속되고 있으며 공급 리스크를 창출하고 있습니다. 이를 위해 무역 조치 및 공급망의 다양화 이니셔티브를 통해 단일 공급 지역에 대한 의존도를 줄이기 위한 정책 조치가 추진되고 있습니다.

텅스텐 카바이드 부문은 2025년에 60%의 점유율을 차지했으며, 2035년까지 연평균 복합 성장률(CAGR) 4.7%로 성장할 것으로 예측됩니다. 이점은 비교할 수 없는 경도, 구조적 안정성 및 가혹한 작동 조건에 대한 내성을 반영하며, 높은 마모성 및 정밀성이 요구되는 산업 분야에서 필수적인 소재입니다.

미국의 텅스텐 시장은 2025년에 12억 달러로 평가되었고, 2035년까지 30억 달러에 이를 것으로 예측됩니다. 북미는 2025년에 18.9%의 점유율을 차지했으며, 강력한 하류 가공 능력 및 수입 원료에 대한 높은 의존도가 특징적인 지역입니다. 국내 능력의 강화 및 외부 의존의 저감을 목적으로 한 정책 조치가 계속해서 지역 시장 역학에 계속 영향을 미치고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 원산국별(2022-2035년)

- 1차

- 2차

제6장 시장 추계 및 예측 : 제품별(2022-2035년)

- 육불화 텅스텐

- 텅스텐 카바이드

- 금속 합금

- 압연 제품

- 기타

- 전기 및 전자 기기

- 기타(촉매, 화학, 방위 장비 등)

제7장 시장 추계 및 예측 : 최종 용도별(2022-2035년)

- 자동차 부품

- 항공우주 부품

- 시추, 천공 및 절삭 기기

- 벌채 기기

- 전기 및 전자 기기

- 반도체

- 기타(촉매, 화학, 방위 장비 등)

제8장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Chongyi ZhangYuan Tungsten Co., Ltd

- Kennametal Inc.

- Sumitomo Electric Industries, Ltd

- China Minmetals Corporation

- Global Tungsten &Powders

- HC Starck Tungsten GmbH

- Japan New Metals Co., Ltd

- Soloro SLU

- WOLFRAM Company JSC

- Buffalo Tungsten Inc.

- Elmet Technologies

- Betek GmbH & Co. KG

- Accumet Materials Co.

- Xiamen Tungsten Co., Ltd

- Cleveland Tungsten, Inc.

The Global Tungsten Market was valued at USD 7.3 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 11.6 billion by 2035.

The market is undergoing a structural shift as circular economy practices become increasingly embedded across supply chains, driven by cost efficiency, regulatory pressure, and the need for long-term material security. Recycling is gaining strategic importance as recovery technologies now allow secondary tungsten to achieve the same chemical purity, crystalline structure, and performance consistency as primary material. Modern thermal and chemical recycling processes enable high recovery yields while significantly lowering energy use and emissions compared to conventional mining and refining. These improvements strengthen the economic rationale for recycled tungsten, particularly in regions facing high energy prices or carbon-related costs. At the same time, geopolitical concentration of primary resources continues to influence market behavior, encouraging diversification and investment in alternative sourcing routes. Growing demand from advanced manufacturing, industrial tooling, and high-performance materials applications continues to underpin steady market expansion, while sustainability-driven procurement policies further reinforce long-term growth potential across global end-use industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.3 Billion |

| Forecast Value | $11.6 Billion |

| CAGR | 4.8% |

The primary tungsten segment accounted for 70.3% share in 2025, supported by mining and concentrate production derived mainly from wolframite and scheelite ores. Production remains highly concentrated geographically, creating supply risk and driving policy actions aimed at reducing dependence on a single source region through trade measures and supply chain diversification initiatives.

The tungsten carbide segment held 60% share in 2025 and is projected to grow at a CAGR of 4.7% through 2035. Its dominance reflects unmatched hardness, structural stability, and resistance to extreme operating conditions, making it indispensable for high-wear and precision-critical industrial applications.

U.S. Tungsten Market was valued at USD 1.2 billion in 2025 and is forecast to reach USD 3 billion by 2035. North America held 18.9% share in 2025, with the region characterized by strong downstream processing capacity and heavy reliance on imported raw materials. Policy measures aimed at strengthening domestic capabilities and reducing external dependence continue to influence regional market dynamics.

Key participants in the Global Tungsten Market include Kennametal Inc., Xiamen Tungsten Co., Ltd., H.C. Starck Tungsten GmbH, China Minmetals Corporation, Global Tungsten & Powders, Sumitomo Electric Industries, Ltd., Buffalo Tungsten Inc., Elmet Technologies, Japan New Metals Co., Ltd., Chongyi ZhangYuan Tungsten Co., Ltd., Betek GmbH & Co. KG, Soloro S.L.U, Accumet Materials Co., WOLFRAM Company JSC, and Cleveland Tungsten, Inc. Companies operating in the Global Tungsten Market are strengthening their competitive position through a combination of vertical integration, recycling investments, and technology-driven process optimization. Many players are expanding secondary material recovery capabilities to improve supply security and reduce exposure to raw material volatility. Strategic partnerships with industrial end users support customized product development and long-term contracts. Firms are also prioritizing geographic diversification of sourcing and processing assets to mitigate geopolitical risks. Continuous investment in high-purity powders and advanced carbide solutions enables differentiation in premium applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Origin

- 2.2.3 Product

- 2.2.4 End-use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Origin, 2022-2035 (USD Billion & Tons)

- 5.1 Key trends

- 5.2 Primary

- 5.3 Secondary

Chapter 6 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion & Tons)

- 6.1 Key trends

- 6.2 Tungsten Hexafluoride

- 6.3 Tungsten carbide

- 6.4 Metal alloys

- 6.5 Mill Products

- 6.6 Others

- 6.6.1 Electrical & electronics appliances

- 6.6.2 Others (catalyst, chemical, defense equipment, etc.)

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion & Tons)

- 7.1 Key trends

- 7.2 Automotive parts

- 7.3 Aerospace components

- 7.4 Drilling, boring & cutting equipment

- 7.5 Logging equipment

- 7.6 Electrical & electronic appliances

- 7.7 Semiconductor

- 7.8 Others (catalyst, chemical, defense equipment, etc.)

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion & Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Chongyi ZhangYuan Tungsten Co., Ltd

- 9.2 Kennametal Inc.

- 9.3 Sumitomo Electric Industries, Ltd

- 9.4 China Minmetals Corporation

- 9.5 Global Tungsten & Powders

- 9.6 H.C. Starck Tungsten GmbH

- 9.7 Japan New Metals Co., Ltd

- 9.8 Soloro S.L.U

- 9.9 WOLFRAM Company JSC

- 9.10 Buffalo Tungsten Inc.

- 9.11 Elmet Technologies

- 9.12 Betek GmbH & Co. KG

- 9.13 Accumet Materials Co.

- 9.14 Xiamen Tungsten Co., Ltd

- 9.15 Cleveland Tungsten, Inc.