|

시장보고서

상품코드

1913369

뇌졸중 관리 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2026-2035년)Stroke Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

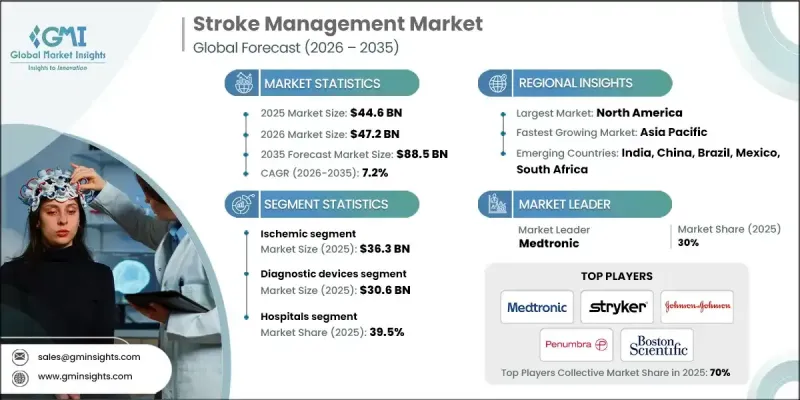

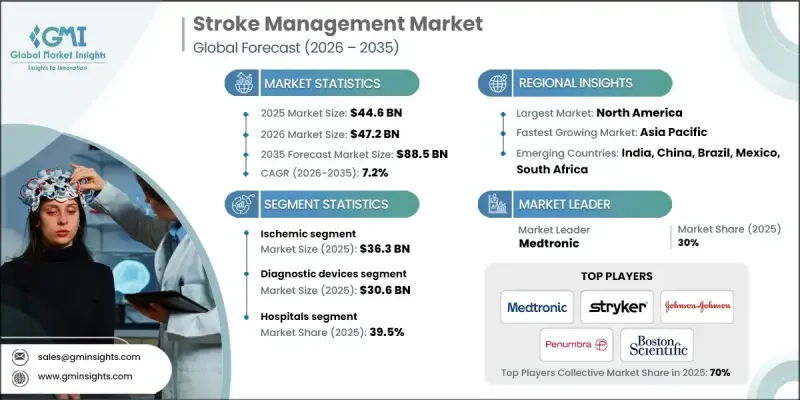

세계의 뇌졸중 관리 시장은 2025년에 446억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 7.2%로 성장할 전망이며, 885억 달러에 이를 것으로 예측됩니다.

시장 성장은 저침습 치료 접근법으로의 전환 증가, 세계 뇌졸중 관련 질병의 발생률 상승, 진단, 치료 및 뇌졸중 후 관리의 지속적인 기술 진보에 의해 지원됩니다. 세계의 의료 시스템은 장기적인 장애 및 사망률을 줄이기 위해 조기 발견, 신속한 대응 시간 및 연계된 케어 경로를 더욱 중시하고 있습니다. 원격 의료 플랫폼과 모바일 의료 제공 모델에 대한 투자 확대는 의료 서비스가 닿기 어려운 지역과 농촌 지역에서 뇌졸중 치료에 대한 접근성 향상에 기여합니다. 예방 전략 및 시기적절한 임상 개입이 공중보건 당국에게 보다 중요한 우선순위가 되고 있는 가운데, 선진적인 솔루션과 통합된 뇌졸중 케어 체제에 대한 수요는 계속 증가하고 있으며, 시장 전체에 지속적인 성장 기회를 창출하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 당초 시장 규모 | 446억 달러 |

| 시장 규모 예측 | 885억 달러 |

| CAGR | 7.2% |

세계적으로 증가하는 심혈관 질환의 유병률은 시장 확대의 주요 요인으로 계속되고 있습니다. 심장 관련 질환 및 뇌졸중 위험의 밀접한 관련성은 신속한 진단과 시기 적절한 개입을 돕는 첨단 뇌졸중 관리 솔루션의 필요성을 높이고 있습니다. 의료 시스템은 이러한 중복 질환을 다루기 위해 협력적인 질병 관리 접근법을 점점 더 우선시하고 있으며 조기 개입과 최적화된 치료 워크플로우를 통해 생존율과 장기적인 환자 결과 개선을 목표로 하고 있습니다.

허혈성 뇌졸중 부문은 2025년 363억 달러를 차지했으며 81.4%의 점유율을 차지했습니다. 이 부문은 즉시 진단, 신속한 치료 대응, 체계화된 재활 경로의 긴급성에서 뇌졸중 관리의 핵심입니다. 이 뇌졸중 유형과 관련된 높은 시간적 제약은 전문적인 치료 솔루션과 첨단 임상 인프라에 대한 투자를 지속적으로 촉진합니다.

진단 장비 부문은 2025년에 306억 달러 시장 규모를 기록했으며, 뇌졸중의 유형 및 중증도를 조기 단계에서 확인하는 데 필수적인 역할을 반영합니다. 정확하고 신속한 진단은 임상 판단을 이끌고 치료 효과에 직접적인 영향을 미치기 때문에 이 부문은 뇌졸중 관리 생태계 전체에서 중요한 구성 요소가 되었습니다.

미국의 뇌졸중 관리 시장은 2025년 374억 달러로 평가되었습니다. 시장 성장은 심장 관련 질환 증가율과 신속한 개입, 치료 성과 향상, 합병증의 감소를 가능하게 하는 선진 의료 기술에 대한 지속적인 투자와 강하게 연관되어 있습니다.

자주 묻는 질문

목차

제1장 분석 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 저침습 수술에 대한 선호 증가

- 세계의 뇌졸중 및 심혈관 질환의 유병률 증가

- 뇌졸중 관리에 있어서 기술적 진보

- 고령화 인구 증가

- 업계의 잠재적 위험 및 과제

- 엄격한 규제 프레임워크

- 치료비 상승

- 시장 기회

- 원격 의료 및 원격 뇌졸중 서비스

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술 진보

- 현재 기술 동향

- 신흥 기술

- 가격 분석(2024년)

- 장래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 매트릭스 분석

- 기업별 시장 점유율 분석

- 주요 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 동향

- 기업 합병 및 인수(M&A)

- 제휴 및 공동 사업

- 신제품 발매

- 확대 계획

제5장 시장의 추정 및 예측 : 유형별(2022-2035년)

- 허혈성

- 출혈성

- 일과성 뇌허혈 발작(TIA)

- 기타 유형

제6장 시장의 추정 및 예측 : 제품별(2022-2035년)

- 진단 장치

- 자기 공명 영상법(MRI)

- 컴퓨터 단층 촬영(CT 스캔)

- 심전도 검사

- 경동맥 초음파 검사

- 뇌혈관 조영

- 기타

- 치료 장치

- 자기 공명 영상법(MRI)

- 컴퓨터 단층 촬영(CT 스캔)

- 심전도 검사

- 경동맥 초음파 검사

- 뇌혈관 조영

- 기타

제7장 시장의 추정 및 예측 : 최종 용도별(2022-2035년)

- 병원

- 외래수술센터(ASC)

- 진단센터

- 기타 최종 용도

제8장 시장의 추정 및 예측 : 지역별(2021-2034년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Medtronic

- Abbott laboratories

- GE HealthCare

- Siemens Healthineers

- Philips Healthcare

- Stryker Corporation

- Johnson &Johnson

- Penumbra

- Boston Scientific

- Imperative Care

- NeuroVasc Technologies

- Kaneka Medix Corp

The Global Stroke Management Market was valued at USD 44.6 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 88.5 billion by 2035.

Market growth is supported by a rising shift toward less invasive treatment approaches, the increasing global incidence of stroke-related conditions, and continuous technological progress across diagnosis, treatment, and post-stroke care. Health systems worldwide are placing stronger emphasis on early detection, faster response times, and coordinated care pathways to reduce long-term disability and mortality. Growing investments in remote care platforms and mobile healthcare delivery models are helping improve access to stroke services in underserved and rural regions. As prevention strategies and timely clinical intervention become higher priorities for public health authorities, demand for advanced solutions and integrated stroke care frameworks continues to increase, creating sustained growth opportunities across the market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $44.6 Billion |

| Forecast Value | $88.5 Billion |

| CAGR | 7.2% |

The rising global prevalence of cardiovascular conditions remains a major contributor to market expansion. The close relationship between heart-related disorders and stroke risk has intensified the need for advanced stroke care solutions that support rapid diagnosis and timely intervention. Health systems are increasingly prioritizing coordinated disease management approaches to address these overlapping conditions, aiming to improve survival rates and long-term patient outcomes through early intervention and optimized treatment workflows.

The ischemic stroke segment accounted for USD 36.3 billion in 2025 and represented 81.4% share. This segment remains central to stroke management due to the urgent need for immediate diagnosis, fast therapeutic response, and structured rehabilitation pathways. The high time sensitivity associated with this stroke type continues to drive investment in specialized care solutions and advanced clinical infrastructure.

The diagnostic devices segment generated USD 30.6 billion in 2025, reflecting their essential role in identifying stroke type and severity at early stages. Accurate and rapid diagnostics guide clinical decision-making and directly influence treatment effectiveness, making this segment a critical component of the overall stroke management ecosystem.

U.S. Stroke Management Market was valued at USD 37.4 billion in 2025. Market growth is strongly linked to increasing rates of cardiac-related conditions and continued investment in advanced care technologies that enable faster intervention, improved outcomes, and reduced complications.

Key companies active in the Global Stroke Management Market include Medtronic, Siemens Healthineers, Abbott Laboratories, GE HealthCare, Philips Healthcare, Stryker Corporation, Boston Scientific, Penumbra, Johnson & Johnson, Imperative Care, Kaneka Medix Corp, and NeuroVasc Technologies. Companies in the Global Stroke Management Market are strengthening their market position through continuous innovation, strategic collaborations, and expansion of comprehensive care portfolios. Many players are investing heavily in research and development to enhance diagnostic accuracy, treatment efficiency, and post-stroke recovery solutions. Partnerships with healthcare providers and academic institutions are helping accelerate technology adoption and clinical validation. Firms are also expanding geographically to tap into underserved markets while aligning products with evolving regulatory requirements. Integration of digital health platforms and data-driven decision support tools is being prioritized to improve care coordination.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Product trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing preference for minimally invasive procedures

- 3.2.1.2 Increasing prevalence of stroke and cardiovascular diseases worldwide

- 3.2.1.3 Technological advancement in stroke management

- 3.2.1.4 Rising geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory framework

- 3.2.2.2 High cost of procedures

- 3.2.3 Market opportunities

- 3.2.3.1 Telemedicine and telestroke services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2024

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Ischemic

- 5.3 Hemorrhagic

- 5.4 Transient Ischemic Attack (TIA)

- 5.5 Other types

Chapter 6 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Diagnostic devices

- 6.2.1 Magnetic Resonance Imaging (MRI)

- 6.2.2 Computed Tomography Scan (CT scan)

- 6.2.3 Electrocardiography

- 6.2.4 Carotid Ultrasound

- 6.2.5 Cerebral Angiography

- 6.2.6 Other

- 6.3 Therapeutic devices

- 6.3.1 Magnetic Resonance Imaging (MRI)

- 6.3.2 Computed Tomography Scan (CT scan)

- 6.3.3 Electrocardiography

- 6.3.4 Carotid Ultrasound

- 6.3.5 Cerebral Angiography

- 6.3.6 Other

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory Surgery Centers

- 7.4 Diagnostic Centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Medtronic

- 9.2 Abbott laboratories

- 9.3 GE HealthCare

- 9.4 Siemens Healthineers

- 9.5 Philips Healthcare

- 9.6 Stryker Corporation

- 9.7 Johnson & Johnson

- 9.8 Penumbra

- 9.9 Boston Scientific

- 9.10 Imperative Care

- 9.11 NeuroVasc Technologies

- 9.12 Kaneka Medix Corp