|

시장보고서

상품코드

1913391

컨베이어 시스템 시장 : 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Conveyor System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

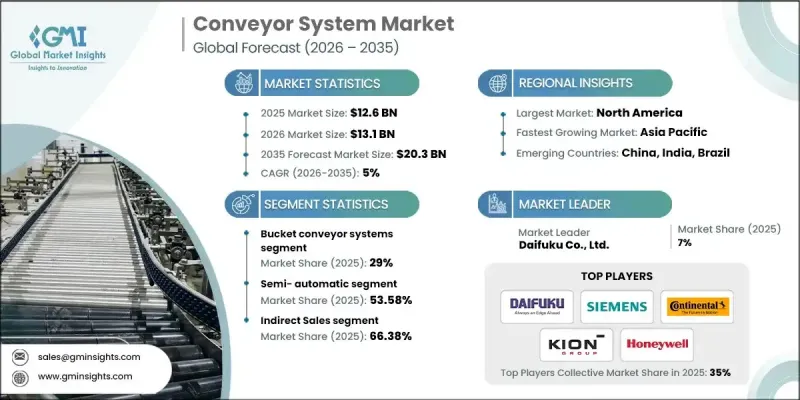

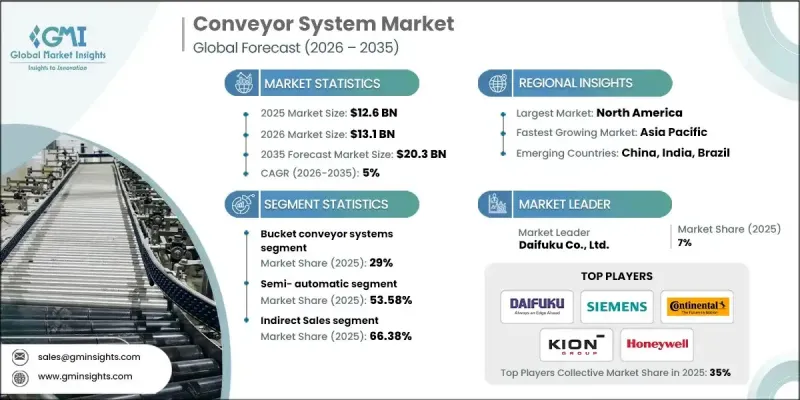

세계의 컨베이어 시스템 시장은 2025년 126억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 5%로 성장하여 203억 달러에 이를 것으로 예측됩니다.

시장 성장은 산업 공급망 전반에 걸친 업무 생산성, 비용 최적화, 장기 지속가능성에 대한 관심 증가에 의해 지원되고 있습니다. 합병과 인수를 통한 업계 재편은 기술 진보를 가속화하고 경쟁 우위를 강화하여 시스템의 광범위한 채용에 기여하고 있습니다. 조직이 노동 집약적인 자재 이동에서 자동화되고 에너지 효율을 고려한 솔루션으로 이동함에 따라 컨베이어 시스템이 점점 선호되고 있습니다. 현대적인 시스템 설계는 전력 소비를 줄이고 운영시 배출량을 줄이는 것이 우선되며 세계의 지속가능성 목표를 준수합니다. 환경에 배려한 제조 및 물류 관행에 대한 대처 강화가 투자 판단에 계속 영향을 주고 있습니다. 산업 운영 전반으로 일관된 처리량, 신뢰성 및 확장성에 대한 요구가 증가함에 따라 수요가 더욱 향상되고 있습니다. 기업이 진화하는 유통 및 풀필먼트 요건에 대응하기 위해 시설을 현대화하는 가운데, 컨베이어 시스템은 효율적인 자재 흐름 전략의 핵심 요소가 되고 있습니다. 이러한 동향이 더해져, 예측기간 중 시장은 꾸준한 확대가 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 규모 | 126억 달러 |

| 시장 규모 예측 | 203억 달러 |

| CAGR | 5% |

북미 전역에서 첨단 창고 및 물류 인프라에 대한 수요가 꾸준히 증가하고 있습니다. 동시에, 유럽 및 아시아태평양의 산업용 및 디지털 상거래 시설에 대한 투자 확대가 상업 분야에서의 도입을 강력하게 추진하고 있습니다. 기업은 처리 능력 요구 사항을 충족하기 위해 자동화된 고효율 시스템을 점점 더 중시하고 속도가 느리고 노동력에 의존하는 프로세스에서 전환을 추진하고 있습니다.

버킷 컨베이어 시스템 부문은 2025년에 29%의 점유율을 차지했습니다. 이 부문은 제한된 공간 레이아웃 내에서 대량의 운송을 효율적으로 수행할 수 있는 능력으로 인해 지속적인 성능을 유지하고 있습니다. 일관된 운영 및 하역 능력은 벌크 재료 응용 분야에서 지속적인 채택을 지원합니다.

간접 판매 부문은 2025년에 66.38%의 점유율을 차지했으며 2035년까지 견조한 성장을 유지할 것으로 예측됩니다. 시스템 통합 사업자와 전문 유통업체는 맞춤형 설치, 기술적 전문 지식 및 지속적인 서비스 지원을 제공하는 데 중요한 역할을 합니다. 구매자는 유지 보수 대응의 신속성과 지역 밀접한 지원을 얻기 위해 이러한 채널에 대한 의존도를 높이고 있습니다.

미국 컨베이어 시스템 시장은 자동화 시설에 대한 지속적인 투자와 유통 네트워크의 확대를 배경으로 2034년까지 연평균 복합 성장률(CAGR) 5.4%를 유지했습니다. 직장 안전, 운영 일관성, 효율성 향상에 중점을 둔 노력이 전국적인 수요를 지속적으로 지원하고 있습니다.

자주 묻는 질문

목차

제1장 분석 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계의 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 요인

- 전자상거래와 풀필먼트의 급속한 성장

- Industry 4.0과 스마트 제조

- 지속가능성과 에너지 효율

- 업계의 잠재적 위험과 과제

- 고액의 초기 설비 투자액과 긴 투자 회수기간

- 기존 현장 개수의 복잡성

- 시장 기회

- IoT와 예지보전의 통합

- 모듈식 및 플렉서블 컨베이어 설계

- 성장 요인

- 성장 가능성 분석

- 미래 시장 동향

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 유형별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업별 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 동향

- 기업 인수합병(M&A)

- 사업 제휴 및 협력

- 신제품 발매

- 확대 계획

제5장 시장의 추정 및 예측 : 제품 유형별(2022-2035년)

- 버킷 컨베이어 시스템

- 벨트 컨베이어 시스템

- 중력식 롤러 컨베이어

- 스크류(나선) 컨베이어

- 체인 컨베이어

- 기타(천장식, 바닥식, 팔레트식 등)

제6장 시장의 추정 및 예측 : 조작별(2022-2035년)

- 반자동

- 자동

제7장 시장의 추정 및 예측 : 최종 용도 분야별(2022-2035년)

- 공항

- 소매업

- 자동차

- 식품 및 음료

- 기타

제8장 시장의 추정 및 예측 : 유통 채널별(2022-2035년)

- 직접

- 간접

제9장 시장의 추정 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Beumer Group

- Continental AG

- Daifuku Co., Ltd.

- FlexLink AB(Coesia Group)

- Fives Group

- KION Group

- Honeywell Intelligrated

- Interroll Holding AG

- Hytrol Conveyor Company, Inc.

- Siemens Logistics

- Intralox, LLC(part of Laitram, LLC)

- Rexnord Corporation

- Shuttleworth, LLC(ProMach)

- Viastore Systems GmbH

- Swisslog Holding AG(KUKA AG)

- WAMGROUP SpA

The Global Conveyor System Market was valued at USD 12.6 billion in 2025 and is estimated to grow at a CAGR of 5% to reach USD 20.3 billion by 2035.

Market growth is supported by increasing focus on operational productivity, cost optimization, and long-term sustainability across industrial supply chains. Industry consolidation through mergers and acquisitions is accelerating technological advancement and strengthening competitive positioning, which is contributing to broader system adoption. Conveyor systems are increasingly preferred as organizations transition away from labor-intensive material movement toward automated and energy-conscious solutions. Modern system designs prioritize reduced power consumption and lower operational emissions, aligning with global sustainability objectives. Growing commitment to environmentally responsible manufacturing and logistics practices continues to influence investment decisions. The rising need for consistent throughput, reliability, and scalability across industrial operations further supports demand. As companies modernize facilities to meet evolving distribution and fulfillment requirements, conveyor systems are becoming a core component of efficient material flow strategies. These trends collectively position the market for steady expansion over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.6 Billion |

| Forecast Value | $20.3 Billion |

| CAGR | 5% |

Demand for advanced warehousing and logistics infrastructure is increasing steadily across North America. At the same time, rising investment in industrial and digital commerce facilities across Europe and the Asia-Pacific region is supporting strong commercial adoption. Businesses are increasingly favoring automated, high-efficiency systems to meet throughput requirements, moving away from slower and labor-dependent processes.

The bucket conveyor systems segment held 29% share in 2025. This segment continues to perform strongly due to its ability to transport high volumes efficiently within limited spatial layouts. Consistent operational performance and load-handling capability support continued adoption across bulk material applications.

The indirect sales segment held 66.38% share in 2025 and is expected to maintain strong growth through 2035. System integrators and specialized distributors play a key role by delivering customized installations, technical expertise, and ongoing service support. Buyers increasingly rely on these channels for maintenance responsiveness and localized assistance.

U.S. Conveyor System Market held a CAGR of 5.4% through 2034, driven by sustained investment in automated facilities and expanding distribution networks. Emphasis on workplace safety, operational consistency, and efficiency improvement continues to support demand nationwide.

Key companies active in the Global Conveyor System Market include Daifuku Co., Ltd., Interroll Holding AG, Honeywell Intelligrated, KION Group, Beumer Group, Swisslog Holding AG (KUKA AG), Hytrol Conveyor Company, Inc., Siemens Logistics, Continental AG, Intralox, L.L.C., Fives Group, Rexnord Corporation, Viastore Systems GmbH, FlexLink AB (Coesia Group), Shuttleworth, LLC, and WAMGROUP S.p.A. Companies operating in the Global Conveyor System Market are reinforcing their market position through product innovation, automation integration, and strategic expansion. Manufacturers are investing in modular and scalable system designs to meet diverse customer requirements. Partnerships with logistics providers and system integrators are helping expand market reach and improve solution customization. Firms are also enhancing digital capabilities, including smart monitoring and predictive maintenance features, to increase system reliability and lifecycle value.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Operation

- 2.2.4 End- Use Vertical

- 2.2.5 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid E-commerce & Fulfillment Growth

- 3.2.1.2 Industry 4.0 & Smart Manufacturing

- 3.2.1.3 Sustainability & Energy Efficiency

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Initial CAPEX & Long ROI

- 3.2.2.2 Complexity of Retrofitting Legacy Sites

- 3.2.3 Opportunities

- 3.2.3.1 IoT & Predictive Maintenance Integration

- 3.2.3.2 Modular & Flexible Conveyor Design

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Bucket Conveyor Systems

- 5.3 Belt Conveyor System

- 5.4 Gravity Roller Conveyor

- 5.5 Screw (Auger) Conveyors

- 5.6 Chain Conveyors

- 5.7 Others (Overhead, Floor, Pallet, etc)

Chapter 6 Market Estimates and Forecast, By Operation, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Semi-automatic

- 6.3 Automatic

Chapter 7 Market Estimates and Forecast, By End Use Vertical, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Airport

- 7.3 Retail

- 7.4 Automotive

- 7.5 Food & Beverages

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Beumer Group

- 10.2 Continental AG

- 10.3 Daifuku Co., Ltd.

- 10.4 FlexLink AB (Coesia Group)

- 10.5 Fives Group

- 10.6 KION Group

- 10.7 Honeywell Intelligrated

- 10.8 Interroll Holding AG

- 10.9 Hytrol Conveyor Company, Inc.

- 10.10 Siemens Logistics

- 10.11 Intralox, L.L.C. (part of Laitram, L.L.C.)

- 10.12 Rexnord Corporation

- 10.13 Shuttleworth, LLC (ProMach)

- 10.14 Viastore Systems GmbH

- 10.15 Swisslog Holding AG (KUKA AG)

- 10.16 WAMGROUP S.p.A.