|

시장보고서

상품코드

1913427

감압 접착제 시장 : 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Pressure Sensitive Adhesives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

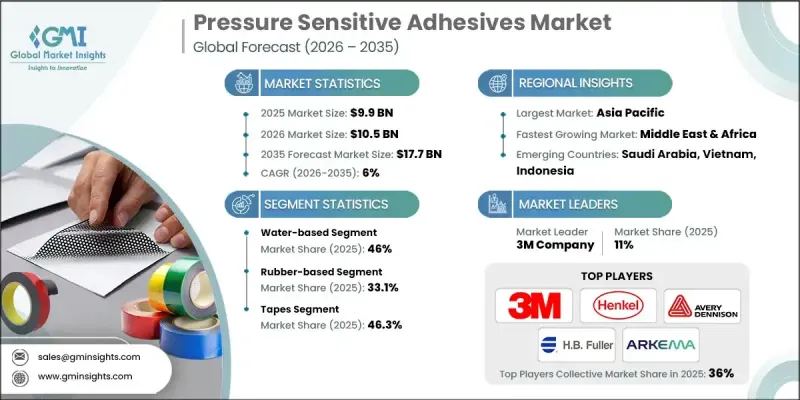

세계의 감압 접착제 시장은 2025년 99억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 6%로 성장하여 177억 달러에 이를 것으로 예측됩니다.

포장, 전자상거래, 자동차, 전자기기, 의료 분야 수요가 증가함에 따라 시장은 꾸준히 성장하고 있습니다. 감압 접착제는 경화, 가열, 추가 가공 시간을 필요로 하지 않고 신속하고 청결하고 효율적인 접착을 실현하기 위해 경량 설계, 자동화, 운영상의 유연성을 중시하는 현대의 제조 및 물류 동향에 최적입니다. 2021년부터 2024년까지의 성장은 특히 전자상거래 확대와 세계 공급망 수요에 힘입어 소포량의 급증에 의해 견인되어 택배용 테이프 및 라벨은 아시아, 북미, 유럽 전역에서 높은 채용률을 유지하고 있습니다. 유럽 및 북미의 규제 변화(VOC 및 용제 제한 등)는 지속가능성과 재활용성을 지원하는 수성, 핫멜트, 아크릴 및 바이오 화학물질로의 전환을 가속화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측연도 | 2026-2035년 |

| 시작 규모 | 99억 달러 |

| 예측 금액 | 177억 달러 |

| CAGR | 6% |

수성 압착 접착제(PSA) 부문은 2025년 46%의 점유율을 차지했며 2035년까지 연평균 복합 성장률(CAGR) 5.7%를 보일 것으로 예측됩니다. 컨버터와 브랜드 소유자가 보다 깨끗한 솔루션, 고속 가공, 에너지 효율을 우선시하면서 수성 및 핫멜트 기술의 채용이 증가하고 있습니다. 북미 및 유럽의 규제 압력은 기존의 솔벤트 시스템에서 전환을 계속 추진하고 있습니다. 또한 고온 조건 하에서 신속한 경화와 정밀한 코팅이 필요한 특수 용도를 위해 UV 경화형 화학제품도 보급되고 있습니다.

테이프 부문은 2025년 46.3%의 점유율을 차지했으며, 2035년까지 연평균 복합 성장률(CAGR) 4.6%를 보일 것으로 예측됩니다. 테이프 및 라벨은 주로 포장, 물류, 자동차, 건설 분야에서 사용되며, 그래픽, 필름, 라미네이트 등의 고부가가치 부문은 프리미엄 수요를 충족합니다. 브랜드 소유자는 점점 더 낮은 에너지 플라스틱, 코팅 필름 및 재생 재료에 접착할 수 있는 감압 접착제(PSA)를 필요로 하며 특수 테이프, 보안 라벨, 보호 필름, 표면 보호 라미네이트에 대한 수요를 견인하고 있습니다.

북미 감압 접착제 시장은 2024년 24억 달러의 규모를 기록했으며, 2034년까지 44억 달러에 이르고 CAGR 6.1%로 성장할 것으로 예측되고 있습니다. 미국은 선진적인 제조, 전자상거래 물류, 의료용 소모품, 고성능 자동차 및 전자기기용 테이프에 지지되어 이 동지역의 핵심 시장으로 계속되고 있습니다. 세계의 주요 접착제 제조업체와 지역 컨버터 기업은 규제 및 소비자 요구에 부응하기 위해 지속 가능하고 낮은 VOC(휘발성 유기 화합물) 기술로 전환하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 요인

- 전자상거래에서 포장 및 라벨 부착량 증가

- 경량화 및 모듈화 제품 설계로의 이행

- 보다 엄격한 휘발성 유기 화합물(VOC) 규제가 저배출 화학물질 지지

- 업계의 잠재적 위험 및 과제

- 원재료 가격의 변동성과 공급 리스크

- 재활용, 라이너 폐기물 및 사용한 제품의 문제

- 시장 기회

- 의료, 위생 및 웨어러블 기기 확대

- 아시아태평양의 전기자동차(EV) 및 전자기기 소형화

- 성장 요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 향후 시장 동향

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)

(참고 : 무역 통계는 주요 국가에서만 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 기술별, 2022-2035년

- 수성 도료

- 아크릴 에멀젼

- 아세트산비닐계

- 기타

- 용제계

- 아크릴 용제형

- 고무 용제형

- 기타

- 핫멜트

- 스티렌계 블록 공중합체(SBC)

- 에틸렌 비닐 아세테이트 공중합체(EVA)

- 폴리올레핀계

- 기타

제6장 시장 추계 및 예측 : 제품별, 2022-2035년

- 고무

- 아크릴

- 실리콘

- 기타

제7장 시장 추계 및 예측 : 용도별, 2022-2035년

- 테이프류

- 포장용 테이프

- 마스킹 테이프

- 양면 테이프

- 의료용 테이프

- 전기용 테이프

- 기타

- 라벨

- 제품 라벨

- 바코드 라벨

- 보안 라벨

- 기타

- 그래픽

- 간판

- 차량 랩핑

- 벽 그래픽

- 바닥 그래픽

- 기타

- 필름 및 라미네이트

- 보호 필름

- 장식용 필름

- 창문 필름

- 기타

- 기타

제8장 시장 추계 및 예측 : 지역별, 2022-2035년

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Wacker Chemie AG

- Evonik Industries AG

- Franklin International, Inc.

- Momentive Performance Materials Inc.

- LG Chem Ltd.

- Beardow Adams(Adhesives) Limited

- 3M Company

- Henkel AG & Co. KGaA

- Avery Dennison Corporation

- HB Fuller Company

- Arkema SA(Bostik)

- Dow Inc.

- BASF SE

- Sika AG

- Ashland Inc.

- Mactac LLC

- Toyo Ink SC Holdings Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Illinois Tool Works Inc.(ITW)

- Sun Chemical Corporation

The Global Pressure Sensitive Adhesives Market was valued at USD 9.9 billion in 2025 and is estimated to grow at a CAGR of 6% to reach USD 17.7 billion by 2035.

The market has steadily grown alongside rising demand in packaging, e-commerce, automotive, electronics, and healthcare applications. Pressure-sensitive adhesives provide fast, clean, and efficient bonding without requiring curing, heat, or additional processing time, making them ideal for modern manufacturing and logistics trends emphasizing lightweight design, automation, and operational flexibility. Growth from 2021 to 2024 was particularly driven by surging parcel volumes fueled by e-commerce expansion and global supply chain demands, with courier tapes and labels maintaining high adoption across Asia, North America, and Europe. Regulatory shifts in Europe and North America, including VOC and solvent restrictions, have accelerated the transition from traditional solvent-based PSAs to water-based, hot-melt, acrylic, and bio-based chemistries that support sustainability and recyclability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.9 Billion |

| Forecast Value | $17.7 Billion |

| CAGR | 6% |

The water-based PSA segment accounted for 46% share in 2025 and is expected to grow at a CAGR of 5.7% through 2035. Adoption of water-based and hot-melt technologies is rising as converters and brand owners prioritize cleaner solutions, faster processing, and energy efficiency. Regulatory pressure in North America and Europe continues to encourage a shift away from traditional solvent-based systems. UV-cured chemistries are also gaining traction for specialized applications requiring rapid curing and precise coating under high-temperature conditions.

The tapes segment held a 46.3% in 2025 and is forecast to grow at a CAGR of 4.6% through 2035. Tapes and labels lead usage primarily in packaging, logistics, automotive, and construction, while high-value segments like graphics, films, and laminates cater to premium demands. Brand owners increasingly require PSAs capable of adhering to low-energy plastics, coated films, and recycled materials, driving the demand for specialty tapes, security labels, protective films, and surface-protectant laminates.

North America Pressure Sensitive Adhesives Market generated USD 2.4 billion in 2024 and is estimated to reach USD 4.4 billion by 2034, growing at a CAGR of 6.1%. The U.S. remains the central market in the region, supported by advanced manufacturing, e-commerce logistics, healthcare consumables, and high-performance automotive and electronics tapes. Both global adhesive majors and regional converters are transitioning toward sustainable, low-VOC technologies to meet growing regulatory and consumer demands.

Key players operating in the Global Pressure Sensitive Adhesives Market include Wacker Chemie AG, Evonik Industries AG, Franklin International, Inc., Momentive Performance Materials Inc., LG Chem Ltd., Beardow Adams (Adhesives) Limited, 3M Company, Henkel AG & Co. KGaA, Avery Dennison Corporation, H.B. Fuller Company, Arkema S.A. (Bostik), Dow Inc., BASF SE, Sika AG, Ashland Inc., Mactac LLC, Toyo Ink SC Holdings Co., Ltd., Nippon Paint Holdings Co., Ltd., Illinois Tool Works Inc. (ITW), and Sun Chemical Corporation. Companies in the Global Pressure Sensitive Adhesives Market are employing multiple strategies to strengthen their presence and market position. They focus heavily on research and development to introduce innovative, sustainable, and high-performance adhesive solutions. Geographic expansion into emerging markets allows firms to access growing industrial and e-commerce sectors. Strategic partnerships with converters, packaging companies, and industrial manufacturers enhance distribution channels and product adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Product

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in e-commerce packaging and labeling volumes

- 3.2.1.2 Shift toward lightweight, modular product designs

- 3.2.1.3 Stricter VOC rules favor low-emission chemistries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw material price volatility and supply risks

- 3.2.2.2 Recycling, liner waste and end-of-life issues

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of medical, hygiene and wearable devices

- 3.2.3.2 EVs and electronics miniaturization in Asia Pacific

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Technology, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Water-based

- 5.2.1 Acrylic emulsion

- 5.2.2 Vinyl acetate-based

- 5.2.3 Others

- 5.3 Solvent-based

- 5.3.1 Acrylic solvent-based

- 5.3.2 Rubber solvent-based

- 5.3.3 Others

- 5.4 Hot melt

- 5.4.1 Styrenic block copolymers (SBC)

- 5.4.2 Ethylene vinyl acetate (EVA)

- 5.4.3 Polyolefin-based

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Rubber-based

- 6.3 Acrylic

- 6.4 Silicone

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Tapes

- 7.2.1 Packaging tapes

- 7.2.2 Masking tapes

- 7.2.3 Double-sided tapes

- 7.2.4 Medical tapes

- 7.2.5 Electrical tapes

- 7.2.6 Others

- 7.3 Labels

- 7.3.1 Product labels

- 7.3.2 Barcode labels

- 7.3.3 Security labels

- 7.3.4 Others

- 7.4 Graphics

- 7.4.1 Signage

- 7.4.2 Vehicle wraps

- 7.4.3 Wall graphics

- 7.4.4 Floor graphics

- 7.4.5 Others

- 7.5 Films & laminates

- 7.5.1 Protective films

- 7.5.2 Decorative films

- 7.5.3 Window films

- 7.5.4 Others

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Wacker Chemie AG

- 9.2 Evonik Industries AG

- 9.3 Franklin International, Inc.

- 9.4 Momentive Performance Materials Inc.

- 9.5 LG Chem Ltd.

- 9.6 Beardow Adams (Adhesives) Limited

- 9.7 3M Company

- 9.8 Henkel AG & Co. KGaA

- 9.9 Avery Dennison Corporation

- 9.10 H.B. Fuller Company

- 9.11 Arkema S.A. (Bostik)

- 9.12 Dow Inc.

- 9.13 BASF SE

- 9.14 Sika AG

- 9.15 Ashland Inc.

- 9.16 Mactac LLC

- 9.17 Toyo Ink SC Holdings Co., Ltd.

- 9.18 Nippon Paint Holdings Co., Ltd.

- 9.19 Illinois Tool Works Inc. (ITW)

- 9.20 Sun Chemical Corporation