|

시장보고서

상품코드

1913450

자율형 농업 장비 시장 : 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Autonomous Farm Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

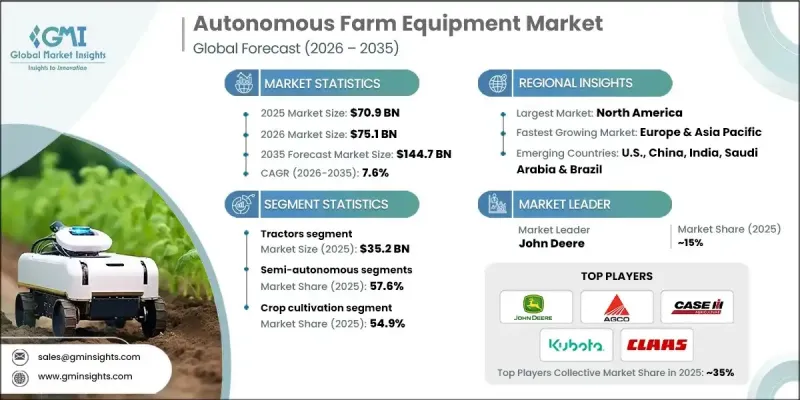

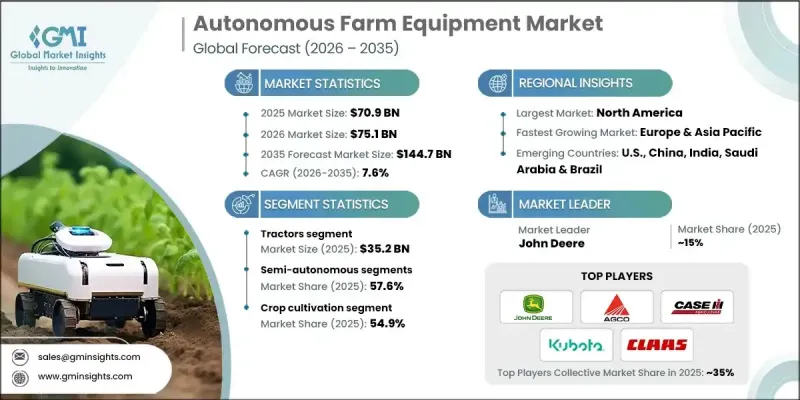

세계의 자율형 농업 장비 시장은 2025년 709억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 7.6%로 성장하여 1,447억 달러에 이를 것으로 예측됩니다.

이 분야의 성장은 정밀 농업 기술의 보급 확대에 의해 추진되고 있습니다. 이러한 접근법은 농부들이 투입 자재의 사용을 최적화하고, 자원 낭비를 최소화하고, 작물 생산량을 극대화하는 것을 가능하게 합니다. 트랙터, 수확기, 드런 등의 자율 기계를 사용하면 농부가 가장 효과적인 시기에 투입물을 적용할 수 있어 수익성을 향상시키면서 환경에 미치는 영향을 줄일 수 있습니다. AI, IoT, 로보틱스, 머신 비전의 융합은 농업에 혁명을 가져오고, 작물 모니터링, 토양 평가, 최소한의 인위적 개입에 의한 자동 수확 등 고급 작업을 가능하게 하고 있습니다. 5G 및 클라우드 플랫폼을 포함한 고급 통신 네트워크를 통해 실시간 모니터링 및 원격 조작이 가능해 효율성과 보급이 더욱 촉진되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 규모 | 709억 달러 |

| 예측 금액 | 1,447억 달러 |

| CAGR | 7.6% |

트랙터 부문은 2025년 352억 달러를 차지했으며 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 7.4%를 보일 것으로 예측됩니다. 트랙터는 농업의 중요한 작업에 필수적이며 AI, GPS 네비게이션 및 IoT 연결의 통합으로 고효율 반자율 또는 완전 자율 기계로 진화하고 있습니다. 노동력 부족과 운영 비용 상승은 수요를 견인하고 있으며, 이러한 트랙터는 수작업 의존도를 줄이면서 정확성과 생산성을 향상시킵니다.

반자율 기기 부문은 57.6%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 7.1%를 보일 것으로 예측됩니다. 이 장비는 자동화와 인적 감시의 균형을 제공하여 자동 조타 및 정밀 제어와 같은 기능을 제공하면서 농부가 운영상의 유연성을 유지할 수 있도록 합니다. 이 하이브리드 접근법은 투자 비용과 기술적 복잡성에 대한 우려에 대응하고 자동화 시스템의 원활한 도입을 가능하게 하며 반복 작업의 효율성을 실현합니다.

미국의 자율형 농업 장비 시장은 2025년에 185억 달러로 평가되었고 2026년부터 2035년까지 CAGR 8.5%를 보일 것으로 예측됩니다. 대규모 농장과 기술적으로 진행된 농업 부문이 자율 솔루션의 도입을 추진하고 있습니다. 기존 제조업체와 신흥기업에 의한 AI, 로보틱스, IoT에 대한 다액의 투자가 도입을 가속시키고 있습니다. 스마트 농업 기술과 지속 가능한 실천에 대한 정부의 우대 조치가 시장의 추가 확대를 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 요인

- 정밀농업 도입 확대

- 기술적 진보

- 정부의 시책과 보조금

- 노동력 부족과 비용 상승

- 업계의 잠재적 위험 및 과제

- 높은 초기 투자와 비용 장벽

- 접속성과 인프라의 제약

- 성장 요인

- 성장 가능성 분석

- 미래 시장 동향

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 제품별, 2022-2035년

- 트랙터

- 수확기

- 파종기

- 분무기

- 무인 항공기(UAV)

- 기타(경작기, 관개 설비)

제6장 시장 추계 및 예측 : 기술별, 2022-2035년

- 안내 및 네비게이션 시스템

- 센서 기술

- 인공지능(AI) 및 머신러닝

- 로보틱스 및 자동화

- 접속성 및 통신 시스템

제7장 시장 추계 및 예측 : 작동별, 2022-2035년

- 완전 자율형

- 준자율형

제8장 시장 추계 및 예측 : 출력별, 2022-2035년

- 30마력 미만

- 31-100마력

- 100마력 초과

제9장 시장 추계 및 예측 : 용도별, 2022-2035년

- 작물 재배

- 원예 및 묘목

- 낙농 및 축산 관리

- 임업 및 목재 관리

제10장 시장 추계 및 예측 : 유통 채널별, 2022-2035년

- 직접 판매

- 간접 판매

제11장 시장 추계 및 예측 : 지역별, 2022-2035년

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 인도네시아

- 말레이시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

제12장 기업 프로파일

- AGCO Corporation

- Agrobot

- Autonomous Solutions Inc.

- Case IH

- Claas

- Dot Technology Corp

- DroneDeploy

- Fendt

- Harvest Automation

- John Deere

- Kinze Manufacturing

- Kubota Corporation

- New Holland Agriculture

- Precision Planting

- Raven Industries

The Global Autonomous Farm Equipment Market was valued at USD 70.9 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 144.7 billion by 2035.

Growth in this sector is fueled by the increasing adoption of precision farming techniques. These methods allow farmers to optimize input use, minimize resource wastage, and maximize crop output. Autonomous machines such as tractors, harvesters, and drones enable farmers to apply inputs at the most effective times, improving profitability while reducing environmental impact. The convergence of AI, IoT, robotics, and machine vision is revolutionizing agriculture, enabling sophisticated operations like crop monitoring, soil assessment, and automated harvesting with minimal human intervention. Advanced communication networks, including 5G and cloud platforms, allow real-time monitoring and remote operation, further enhancing efficiency and adoption.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $70.9 Billion |

| Forecast Value | $144.7 Billion |

| CAGR | 7.6% |

The tractors segment accounted for USD 35.2 billion in 2025 and is expected to grow at a CAGR of 7.4% from 2026 to 2035. They remain critical for essential farm operations, and the integration of AI, GPS navigation, and IoT connectivity has transformed them into highly efficient, semi- or fully-autonomous machines. Labor shortages and rising operational costs drive demand, as these tractors reduce reliance on manual work while boosting precision and productivity.

The semi-autonomous equipment segment held a 57.6% share and is projected to grow at a CAGR of 7.1% from 2026 to 2035. This equipment offers a balance between automation and human oversight, providing features like auto-steering and precision controls while allowing farmers to retain operational flexibility. This hybrid approach addresses concerns over investment costs and technical complexity, enabling smoother adoption of automated systems and improving efficiency for repetitive tasks.

U.S. Autonomous Farm Equipment Market was valued at USD 18.5 billion in 2025 and is forecasted to grow at a CAGR of 8.5% from 2026 to 2035. Large-scale farms and a technologically advanced agricultural sector drive the adoption of autonomous solutions. Substantial investments in AI, robotics, and IoT by both established manufacturers and startups accelerate deployment. Government incentives for smart farming technologies and sustainable practices further stimulate market expansion.

Key players in the Global Autonomous Farm Equipment Market include Case IH, John Deere, Kinze Manufacturing, Kubota Corporation, AGCO Corporation, Claas, Dot Technology Corp, DroneDeploy, Precision Planting, New Holland Agriculture, Fendt, Harvest Automation, Autonomous Solutions Inc., and Agrobot. Companies in the Autonomous Farm Equipment Market are focusing on multiple strategies to strengthen their foothold. They are investing heavily in research and development to enhance the capabilities of autonomous machines, including AI-driven navigation and advanced sensor integration. Strategic partnerships and collaborations with tech startups and agri-tech firms help expand product portfolios and enter new markets. Firms are also emphasizing after-sales services, training, and support programs to boost customer adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Technology

- 2.2.4 Operation

- 2.2.5 Power output

- 2.2.6 Application

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of precision agriculture

- 3.2.1.2 Technological advancements

- 3.2.1.3 Government initiatives and subsidies

- 3.2.1.4 Labor shortages and rising costs

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment and cost barriers

- 3.2.2.2 Connectivity and infrastructure limitations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Tractor

- 5.3 Harvesters

- 5.4 Planters

- 5.5 Sprayers

- 5.6 UAVs

- 5.7 Others (cultivators, irrigation equipment)

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Guidance & navigation systems

- 6.3 Sensor technologies

- 6.4 Artificial intelligence & machine learning

- 6.5 Robotics & automation

- 6.6 Connectivity and communication systems

Chapter 7 Market Estimates & Forecast, By Operation, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Fully autonomous

- 7.3 Semi-autonomous

Chapter 8 Market Estimates & Forecast, By Power Output, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Below 30 HP

- 8.3 31-100 HP

- 8.4 Above 100 HP

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Crop cultivation

- 9.3 Horticulture & nursery

- 9.4 Dairy & livestock management

- 9.5 Forestry & timber management

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 AGCO Corporation

- 12.2 Agrobot

- 12.3 Autonomous Solutions Inc.

- 12.4 Case IH

- 12.5 Claas

- 12.6 Dot Technology Corp

- 12.7 DroneDeploy

- 12.8 Fendt

- 12.9 Harvest Automation

- 12.10 John Deere

- 12.11 Kinze Manufacturing

- 12.12 Kubota Corporation

- 12.13 New Holland Agriculture

- 12.14 Precision Planting

- 12.15 Raven Industries