|

시장보고서

상품코드

1913453

자전거 롤러 브레이크 시장 : 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Bicycle Roller Brake Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

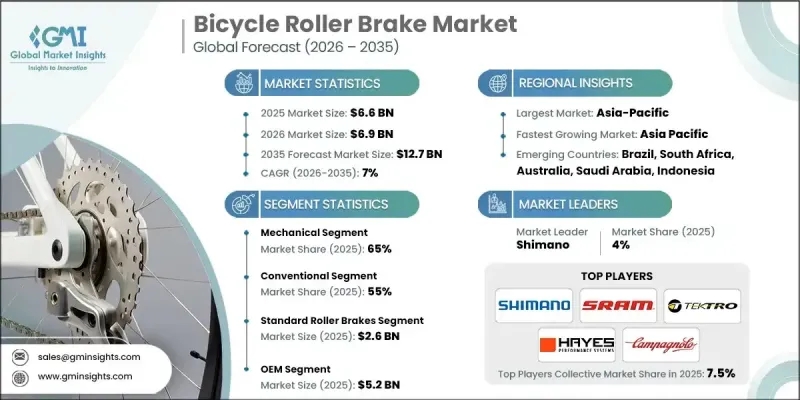

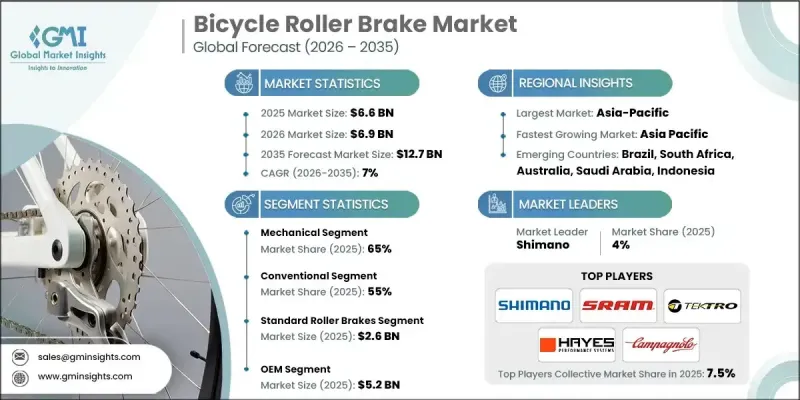

세계의 자전거 롤러 브레이크 시장은 2025년 66억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 7%로 성장하여 127억 달러에 이를 것으로 예측됩니다.

본 시장은 라이더의 기대 변화, 브레이크 기술의 꾸준한 진보, 도시 교통 행동의 장기적인 변화에 의해 현저한 변화기에 있다고 설명하고 있습니다. 이러한 요인은 경쟁 환경을 재정의하고 진화하는 고객의 요구에 신속하게 대응하는 브랜드에 대한 새로운 수익 경로를 개척하고 있다고 말합니다. 롤러 브레이크는 일관된 성능과 긴 수명을 위해 설계된 밀폐형 제동 솔루션으로 자리매김하며, 특히 다양한 기상 조건 하에서 신뢰성이 필수적인 도시와 실용적인 사이클링 환경에서 높은 평가를 받고 있습니다. 유지보수가 최소화되는 자전거 수요가 높아지고 있는 것이, 특히 기술적인 유지 관리를 필요로 하지 않고 신뢰성이 높은 교통 수단을 요구하는 도시 통근자층을 중심으로, 수요를 크게 지지하고 있는 점이 강조되고 있습니다. 시장 동향에서는 통합형으로 유지보수가 낮은 자전거 플랫폼의 보급 확대가 채용 증가에 기여하고 있다는 점이 강조되고 있습니다. 게다가 대규모 공유 모빌리티 사업자가 다운타임 삭감을 위해 내구성이 높은 제동 시스템을 선호하는 경향이 강해져, 이것이 보급을 가속시키고 있다고 말해지고 있습니다. 전반적으로 편리성, 내구성, 소유의 용이성을 중시하는 유저층에 의해 수요가 형성되고 있으며, 성숙한 고이용률의 자전거 시장에서 롤러 브레이크는 실용적인 해결책으로 자리매김하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 규모 | 66억 달러 |

| 예측 금액 | 127억 달러 |

| CAGR | 7% |

기계식 부문은 2025년 65%의 점유율을 차지했으며, 2026년부터 2035년까지 CAGR 6%를 보일 것으로 예측됩니다. 기계식 롤러 브레이크는 안정적인 제동력을 제공하면서 비용 효율성을 유지하는 케이블 작동 시스템으로 설명되어 있습니다. 이러한 솔루션은 확립된 기계적 지렛대 원리에 의존하며 장기간 안정적인 성능을 보장한다고 합니다. 이 부문은 표준 부품과의 광범위한 호환성, 성숙한 유통 네트워크 및 간편한 유지 보수 프로세스의 이점을 가지고 있습니다. 게다가 전문기기를 필요로 하지 않고 진단 및 정비가 가능한 점이, 세계 시장에서의 높은 보급률을 계속 지지하고 있다고 설명되고 있습니다.

기존 자전거 부문은 2025년에 55%의 점유율을 차지했고, 2035년까지 연평균 복합 성장률(CAGR) 6.3%를 보일 것으로 예측됩니다. 이 이점은 일상적인 이동 수단으로 자전거와 관련된 높은 판매 수량 때문입니다. 이러한 제품은 일관된 제동 성능이 필수적인 저렴한 이동 수단으로 자리매김하는 것으로 설명되어 있습니다. 제조업체는 기존 카테고리의 내구성과 제품 매력을 향상시키기 위해 롤러 브레이크 시스템에 대한 의존도를 높이고 있다고 합니다. 특히, 기존 자전거 설계에서 혁신의 기회가 한정되어 있는 상황하에서는 이 경향이 현저합니다.

아시아태평양의 자전거 롤러 브레이크 시장은 2025년 21억 달러 규모에 이르렀습니다. 이 지역의 주도적 지위는 광범위한 제조 인프라와 대규모 자전거 이용자층에 기인하고 있습니다. 중국, 일본, 인도는 생산 능력과 소비자 수요의 주요 공헌국으로 꼽힙니다. 중국은 주요 제조 기지로 인식되고 있으며 세계 자전거 생산량의 약 68%를 차지합니다. 이 나라의 연간 생산 대수는 4,600만대로, 월간 약 130만대에 상당하고, 중국은 롤러 브레이크 시스템의 최대의 소비국 및 공급국으로서의 지위를 확립하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 컴포넌트 제조업체

- 브레이크 제조업체 및 인티그레이터

- 자전거 제조업체

- 애프터마켓 유통 채널

- 최종 사용자 및 서비스 네트워크

- 비용 구조

- 이익률

- 각 단계에서의 부가가치

- 수직 통합의 동향

- 디스랩터(시장 변혁자)

- 공급자의 상황

- 영향요인

- 성장 요인

- 도시화와 자전거 통근 확대

- 전기자전거 및 실용 자전거의 확대

- 림 브레이크에 대한 안전성 및 신뢰성의 우선도

- 도시형 및 쾌적성 중시 자전거 부문에서의 OEM 통합

- 업계의 잠재적 위험 및 과제

- 디스크 브레이크와의 경쟁 구도

- 급경사 및 고속 주행시의 발열 문제

- 시장 기회

- 낮은 유지 보수 필요성을 가진 자전거 플랫폼의 성장

- 내부 변속 허브와의 통합

- 자전거 공유 플릿의 새로운 수요 동향

- 제품 개량(방열성 및 변조 성능)

- 성장 요인

- 기술 동향과 혁신 및 에코시스템

- 현행 기술

- 신흥기술

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국 소비자 제품 안전 위원회(CPSC) 기준

- ASTM 국제규격(F2043, F1898)

- 캐나다의 자전거 안전 규제

- 유럽

- EN 15194(전기 자전거 규격)

- 유럽에서의 페달 구동식 자전거 규제

- 저배출 가스 및 도시 모빌리티 정책

- 아시아태평양

- 중국의 자전거 및 전기자전거용 국가 규격(GB)

- 인의도 자동차 산업 규격(전기자전거용 AIS 052)

- 일본의 JIS 규격

- ASEAN 자전거 기준

- 라틴아메리카

- 브라질 ABNT NBR 규격

- 아르헨티나 INTA/IRAM 규격

- 멕시코 NOM 규격

- 중동 및 아프리카

- UAE GSO/ESMA 자전거 규제

- 사우디아라비아 SASO 자전거 규격

- 남아프리카공화국 SABS 자전거 안전 규제

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 비용 내역 분석

- 가격 동향

- 지역별

- 제품별

- 특허 분석

- 생산 통계

- 생산 거점

- 소비 허브

- 수출과 수입

- 지속가능성과 환경면

- 지속가능한 실천

- 폐기물 감축 전략

- 제조에서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고찰

- 기술 비교 : 롤러 브레이크 및 대체 기술

- 롤러 브레이크와 림 브레이크의 비교

- 롤러 브레이크와 기계식 디스크 브레이크의 비교

- 롤러 브레이크와 유압식 디스크 브레이크의 비교

- 성능, 비용, 유지 보수성, 안전성의 트레이드 오프

- OEM 사양과 채용 전략

- 자전거 카테고리별 롤러 브레이크의 채용 상황

- 엔트리 모델과 미드레인지 모델의 OEM 포지셔닝

- 지역별 OEM의 선호 패턴

- 비용 중시 설계와 내구성 중시 설계의 트레이드 오프

- 시스템 호환성 및 통합 고려 사항

- 애프터마켓 수요의 동향

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 제품별, 2022-2035년

- 표준 롤러 브레이크

- 고성능 롤러 브레이크

- 통합형 허브 기어 롤러 브레이크

- 코스터 브레이크

제6장 시장 추계 및 예측 : 구분별, 2022-2035년

- 기계식

- 유압

제7장 시장 추계 및 예측 : 자전거별, 2022-2035년

- 기존

- 전기자전거

제8장 시장 추계 및 예측 : 용도별, 2022-2035년

- 도시용 자전거

- 산악 자전거

- 레이싱 자전거

- 하이브리드 자전거

제9장 시장 추계 및 예측 : 판매 채널별, 2022-2035년

- OEM

- 애프터마켓

제10장 시장 추계 및 예측 : 지역별, 2022-2035년

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 글로벌 기업

- Campagnolo

- Hayes Performance Systems

- Magura

- Promax Components

- Shimano

- SRAM

- SunRace Sturmey-Archer

- Tektro Technology

- Region players

- Alhonga

- Avid

- Cane Creek

- Clarks Cycle Systems

- Dia-Compe

- Hope Technology

- Jagwire

- KCNC

- Paul Component Engineering

- 신흥 제조업체

- TRP Cycling Components

- Weinmann

- XLC Components

The Global Bicycle Roller Brake Market was valued at USD 6.6 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 12.7 billion by 2035.

The market is described as undergoing notable transformation due to shifting rider expectations, steady advancements in braking technologies, and long-term changes in urban transportation behavior. It is explained that these forces are redefining competition and opening new revenue pathways for brands that respond quickly to evolving customer needs. Roller brakes are identified as enclosed braking solutions designed for consistent performance and long service life, particularly valued in urban and utility cycling environments where reliability in varied weather conditions is essential. It is emphasized that the rising preference for bicycles requiring minimal servicing has significantly supported demand, especially among city commuters seeking dependable transportation without technical upkeep. The market narrative highlights that the growing presence of integrated, low-maintenance bicycle platforms has contributed to increased adoption. It is further stated that large-scale shared mobility operators increasingly favor durable braking systems to limit downtime, which has accelerated acceptance. Overall, demand is said to be shaped by users prioritizing convenience, longevity, and ease of ownership, positioning roller brakes as a practical solution in mature and high-usage cycling markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.6 Billion |

| Forecast Value | $12.7 Billion |

| CAGR | 7% |

The mechanical segment accounted for 65% share in 2025 and is forecast to grow at a CAGR of 6% from 2026 to 2035. Mechanical roller brakes are described as cable-actuated systems that deliver dependable stopping power while remaining cost-efficient. These solutions are said to rely on established mechanical leverage principles that ensure stable performance over long periods. The segment benefits from widespread compatibility with standard components, mature distribution networks, and straightforward maintenance processes. It is further noted that the ability to diagnose and service these systems without specialized equipment continues to support their strong adoption across global markets.

The conventional bicycle segment held a 55% share in 2025 and is projected to grow at a CAGR of 6.3% through 2035. This dominance is attributed to high sales volumes associated with everyday transportation bicycles. It is explained that these products are positioned as affordable mobility options where consistent braking performance is essential. Manufacturers are said to increasingly rely on roller brake systems to enhance durability and product appeal within established categories, particularly as innovation opportunities remain limited in traditional bicycle designs.

Asia-Pacific Bicycle Roller Brake Market generated USD 2.1 billion in 2025. The region's leadership is linked to its extensive manufacturing infrastructure and large cycling population. China, Japan, and India are referenced as major contributors to production capacity and consumer demand. China is identified as the primary manufacturing hub, accounting for nearly 68% of worldwide bicycle output. Annual production in the country is stated at 46 million units, equal to approximately 1,300,000 bicycles per month, positioning China as both the largest consumer and supplier of roller brake systems.

Key companies operating in the Bicycle Roller Brake Market include Shimano, SRAM, Tektro Technology, Campagnolo, Magura, Hayes Performance Systems, Promax Components, Clarks Cycle Systems, Alhonga, and Hope Technology (IPCO). Companies in the Bicycle Roller Brake Market are said to be strengthening their positions through a combination of product innovation, manufacturing optimization, and strategic partnerships. Leading players are focusing on improving durability, heat management, and system efficiency to meet evolving performance expectations. Many manufacturers are investing in automation and localized production to reduce costs and ensure consistent quality. Strategic collaborations with bicycle manufacturers and fleet operators are also emphasized as a key approach to securing long-term supply agreements. In addition, companies are expanding their presence in high-growth regions by strengthening distribution networks and offering tailored solutions aligned with regional riding.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Break

- 2.2.4 Bicycle

- 2.2.5 Application

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Component manufacturers

- 3.1.1.2 Break manufacturers & integrators

- 3.1.1.3 Bicycle manufacturers

- 3.1.1.4 Aftermarket distribution channels

- 3.1.1.5 End-user & service networks

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Urbanization & growth of commuter cycling

- 3.2.1.2 Expansion of e-bikes & utility bikes

- 3.2.1.3 Safety & reliability preference over rim brakes

- 3.2.1.4 OEM integration in city/comfort bicycle segments

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Competition from disc brakes

- 3.2.2.2 Heat buildup under steep/high-speed use

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of low-maintenance bicycle platforms

- 3.2.3.2 Integration with internal gear hubs

- 3.2.3.3 Emerging demand in bike-sharing fleets

- 3.2.3.4 Product improvements (heat dissipation & modulation)

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 U.S. Consumer Product Safety Commission (CPSC) standards

- 3.5.1.2 ASTM international standards (F2043, F1898)

- 3.5.1.3 Canada bicycle safety regulations

- 3.5.2 Europe

- 3.5.2.1 EN 15194 (E-Bike Standard)

- 3.5.2.2 European pedal-powered bicycle regulations

- 3.5.2.3 Low-Emission / Urban mobility policies

- 3.5.3 Asia-Pacific

- 3.5.3.1 China GB standards for bicycles and e-bikes

- 3.5.3.2 India Automotive Industry Standards (AIS 052 for E-Bikes)

- 3.5.3.3 Japan JIS standards

- 3.5.3.4 ASEAN bicycle standards

- 3.5.4 Latin America

- 3.5.4.1 Brazil ABNT NBR standards

- 3.5.4.2 Argentina INTA / IRAM standards

- 3.5.4.3 Mexico NOM standards

- 3.5.5 Middle East & Africa

- 3.5.5.1 UAE GSO / ESMA bicycle regulations

- 3.5.5.2 Saudi Arabia SASO bicycle standards

- 3.5.5.3 South Africa SABS bicycle safety regulations

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Cost breakdown analysis

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Patent analysis

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Technology benchmarking: roller brakes vs alternatives

- 3.13.1 Roller brakes vs rim brakes

- 3.13.2 Roller brakes vs mechanical disc brakes

- 3.13.3 Roller brakes vs hydraulic disc brakes

- 3.13.4 Performance, cost, maintenance & safety trade-offs

- 3.14 OEM specification & adoption strategy

- 3.14.1 Roller brake fitment by bicycle category

- 3.14.2 Entry-level vs mid-range OEM positioning

- 3.14.3 Regional OEM preference patterns

- 3.14.4 Design-for-cost vs design-for-durability trade-offs

- 3.15 System compatibility & integration considerations

- 3.16 Aftermarket demand dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Standard roller brakes

- 5.3 High-performance roller brakes

- 5.4 Integrated hub-gear roller brakes

- 5.5 Coaster brakes

Chapter 6 Market Estimates & Forecast, By Break, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Mechanical

- 6.3 Hydraulic

Chapter 7 Market Estimates & Forecast, By Bicycle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Conventional

- 7.3 E-bike

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 City/Urban bicycles

- 8.3 Mountain bicycles

- 8.4 Racing bicycles

- 8.5 Hybrid bicycles

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Campagnolo

- 11.1.2 Hayes Performance Systems

- 11.1.3 Magura

- 11.1.4 Promax Components

- 11.1.5 Shimano

- 11.1.6 SRAM

- 11.1.7 SunRace Sturmey-Archer

- 11.1.8 Tektro Technology

- 11.2 Region players

- 11.2.1 Alhonga

- 11.2.2 Avid

- 11.2.3 Cane Creek

- 11.2.4 Clarks Cycle Systems

- 11.2.5 Dia-Compe

- 11.2.6 Hope Technology

- 11.2.7 Jagwire

- 11.2.8 KCNC

- 11.2.9 Paul Component Engineering

- 11.3 Emerging players

- 11.3.1 TRP Cycling Components

- 11.3.2 Weinmann

- 11.3.3 XLC Components