|

시장보고서

상품코드

1913479

궤도 부설 설비 시장 예측 : 기회, 성장 요인, 업계 동향 분석(2026-2035년)Track Laying Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

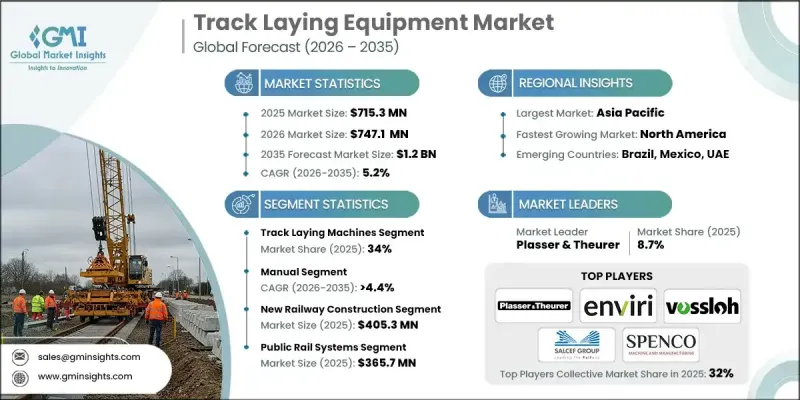

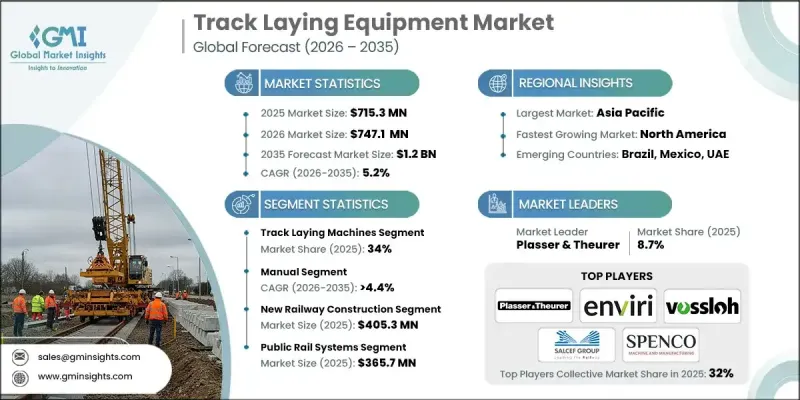

세계의 궤도 부설 설비 시장은 2025년에 7억 1,530만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.2%로 성장하고 12억 달러에 이를 것으로 예측되고 있습니다.

시장 확대의 배경에는 대규모 철도 네트워크 개발, 도시 인구 증가 가속화, 신규 철도선 투자 확대, 기존 철도 자산 개수 수요 증가 등이 있습니다. 철도 당국, 지하철 사업자, 화물 운송 서비스 제공업체는 시공 정밀도 향상, 수명주기 비용 절감, 엄격한 프로젝트 납기 준수에 주력하고 있습니다. 그 결과, 일관된 건설 품질 달성, 노동 생산성 향상, 장기적인 궤도 성능 강화를 위해 현대적인 궤도 부설 솔루션의 도입이 필수적입니다. 게다가 신규 철도 선로 및 개수 프로젝트에 있어서의 안전 기준의 준수와 정밀 설치에의 중시가 높아지고 있는 것도, 시장 전망은 더욱 밝아질 것으로 보입니다. 도시 교통, 화물 운송망, 장거리 철도선에 대한 지속적인 투자는 기술 기준을 유지하면서 신속한 배치를 지원하는 효율적인 장비에 대한 지속적인 수요를 창출하고 있습니다. 성숙지역과 신규지역 모두에서 철도 인프라가 경제 성장과 모빌리티 개발의 우선사항이 되고 있는 가운데, 궤도 부설 설비 시장은 지속적인 성장세를 보이고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 금액 | 7억 1,530만 달러 |

| 예측 금액 | 12억 달러 |

| CAGR | 5.2% |

설비 설계와 디지털 통합의 발전으로 철도 선로를 설치 및 유지 보수하는 방법이 재구성되었습니다. 반자동화 및 자동화 기계로의 전환은 지능형 제어 시스템 및 연결된 모니터링 플랫폼과 결합하여 보다 일관된 생산성을 실현하고 수작업에 대한 의존도를 줄여줍니다. 차세대 궤도 부설 솔루션을 채택하는 사업자에게는 정밀도 향상, 자산 활용률의 개선, 다운타임의 삭감이 중요한 이점이 되고 있습니다. 도시 철도 시스템과 장거리 노선의 도입 확대에 따라 프로젝트 라이프 사이클 전반에 걸쳐 효율성과 내구성을 지원하는 기술적으로 고도의 설비에 대한 수요가 높아지고 있습니다.

2025년 현재 궤도 부설 기계 부문은 34%의 점유율을 차지했습니다. 이 우위는 선로와 침목의 신속한 설치를 지원하면서, 위치 정밀도와 시공의 일관성을 유지하는 같은 부문의 능력에 기인합니다. 지하철 프로젝트, 화물선, 대규모 인프라 개발에서 높은 가동률로 궤도 부설 기계는 현대 철도 건설 워크플로우의 핵심 구성 요소로서의 지위를 확립하고 있습니다.

수동 부문은 2025년에 55%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 4.4%의 성장이 예상됩니다. 적당한 가격, 조작의 간편성, 표준적인 철도 건설 및 보수 작업에의 적응성에 의해 높은 채택율을 유지하고 있습니다. 특히 대규모 자동화가 미성숙한 지역에서는 유연성과 초기 투자가 낮기 때문에 많은 계약자와 철도 당국이 수동 설비에 대한 의존을 계속하고 있습니다.

중국 궤도 부설 장비 시장은 2025년에 42%의 점유율을 차지했습니다. 아시아태평양은 광범위한 철도망 확장, 높은 인프라 지출, 첨단 궤도 건설 솔루션의 도입 증가에 힘입어 주요 지역 시장으로 부상하고 있습니다. 철도 현대화와 기술 통합에 대한 지속적인 투자는 이 지역의 견고한 시장 지위를 더욱 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 수익률

- 비용 구조

- 단계별 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계의 철도 인프라의 급속한 확대

- 궤도 부설 및 보수 설비에 있어서의 기술적 진보

- 정부투자와 현대화 프로그램

- 도시화, 산업화 및 화물 수요 증가

- 업계의 잠재적 위험 및 과제

- 고액의 설비 투자와 장비 비용

- 숙련 노동자 부족과 연수 요건

- 시장 기회

- 철도건설 및 보수 자동화와 디지털화

- 신흥 시장 및 신규 철도 프로젝트

- 기존 철도 인프라 업그레이드 및 현대화

- 디지털 및 자동화된 궤도 부설 솔루션의 도입

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국 연방 철도국(FRA)의 규제

- 캐나다 운수 기준

- 유럽

- 독일 TUV 및 BaFin 준수

- 프랑스 DGITM 가이드라인

- 영국 철도 규제청(ORR)의 규제

- 이탈리아 인프라 및 교통부 규정 준수

- 아시아태평양

- 중국 MIIT 지침

- 일본 MLIT 표준

- 대한민국 국토교통부 규정

- 인도 철도 및 BIS 가이드라인

- 라틴아메리카

- 브라질 ANTT 및 DENIT 규제

- 멕시코 SCT & FERROCARRILS 가이드라인

- 중동 및 아프리카

- 아랍에미리트(UAE) 도로 교통국(RTA) 가이드라인

- 사우디아라비아 교통청(GAT) 규정

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 자동화 및 로봇 공학

- AI와 머신러닝

- 사물인터넷(IoT)

- 신규 기술

- 하이퍼커넥티드 철도 네트워크

- 궤도 부설 로보틱스 서비스(RaaS)

- AI에 의한 예지 보전과 동적 자원 배분

- 현재의 기술 동향

- 가격 동향

- 지역별

- 제품별

- 코스트 내역 분석

- 특허 분석

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 친환경 이니셔티브

- 탄소발자국에 관한 고려 사항

- 이용 사례 시나리오

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추정 및 예측 : 기기별, 2022-2035

- 궤도 부설기

- 탬핑 머신

- 밸러스트 레귤레이터

- 침목 포설 장비

- 레일 용접 장비

- 기타

제6장 시장 추정 및 예측 : 기술별, 2022-2035

- 수동

- 반자동

- 완전 자동

제7장 시장 추정 및 예측 : 용도별, 2022-2035

- 신규 철도 건설

- 궤도 유지 보수

- 업그레이드 및 현대화

제8장 시장 추정 및 예측 : 최종 용도별, 2022-2035

- 공공 철도 시스템

- 민간 화물 운송 회사

- 민간 여객 사업자

- 방어

제9장 시장추정 및 예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 말레이시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제10장 기업 프로파일

- Global Player

- Balfour Beatty Rail

- Enviri

- Harsco Rail

- Matisa

- Plasser & Theurer

- Salfec

- Spenco

- Tampertec

- Vossloh

- Weihua Group

- Regional Player

- Alstom Track Solutions

- CRRC Railway Equipment

- CSR Zhuzhou

- Kinki Sharyo

- Lloyds Register Rail

- Orenstein &Koppel

- Robel

- Shandong Railway Construction Machinery

- VAE Group

- ZTR Rail

- 신규기업

- Gulf Rail Technologies

- Metro Track Systems

- RailTech Innovations

- RapidRail Machinery

- TrackTech Solutions

The Global Track Laying Equipment Market was valued at USD 715.3 million in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 1.2 billion by 2035.

Market expansion is fueled by large-scale railway network development, accelerating urban population growth, and rising spending on new rail corridors as well as upgrades of older rail assets. Rail authorities, metro operators, and freight service providers are increasingly focused on improving construction accuracy, lowering lifecycle costs, and meeting strict project delivery schedules. As a result, the adoption of modern track laying solutions is becoming essential to achieve consistent build quality, improve workforce productivity, and enhance long-term track performance. The market outlook is further strengthened by the growing emphasis on safety compliance and precision-based installation across new rail lines and rehabilitation projects. Continued investments in urban transit, freight connectivity, and long-distance rail routes are creating sustained demand for efficient equipment that supports faster deployment while maintaining engineering standards. The track laying equipment market continues to gain traction as rail infrastructure remains a priority for economic growth and mobility development across both mature and emerging regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $715.3 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 5.2% |

Advancements in equipment design and digital integration are reshaping how rail tracks are installed and maintained. The shift toward semi-automated and automated machinery, combined with intelligent control systems and connected monitoring platforms, is enabling more consistent output and reduced dependency on manual intervention. Enhanced accuracy, improved asset utilization, and reduced downtime are becoming key advantages for operators adopting next-generation track laying solutions. Increasing deployment across urban rail systems and long-distance corridors is reinforcing demand for technologically advanced equipment that supports efficiency and durability throughout the project lifecycle.

The track laying machines segment held 34% share in 2025. This dominance is attributed to the segment's ability to support rapid installation of rails and sleepers while maintaining alignment precision and construction consistency. High utilization across metro rail projects, freight lines, and large infrastructure developments has positioned track laying machines as a core component of modern rail construction workflows.

The manual segment held 55% share in 2025 and is anticipated to grow at a CAGR of 4.4% from 2026 to 2035. Strong adoption is driven by affordability, operational simplicity, and suitability for standard rail construction and maintenance activities. Many contractors and rail authorities continue to rely on manual equipment due to its flexibility and lower upfront investment, particularly in regions where large-scale automation is still developing.

China Track Laying Equipment Market held 42% share in 2025. Asia-Pacific emerged as the leading regional market, supported by extensive rail network expansion, high infrastructure spending, and increasing adoption of advanced track construction solutions. Ongoing investments in rail modernization and technology integration are reinforcing the region's strong market position.

Key participants active in the Global Track Laying Equipment Market include Plasser & Theurer, Matisa, Harsco Rail, Vossloh, Weihua Group, Balfour Beatty Rail, Enviri, Salfec, Spenco, and Tampertec. Companies operating in the Track Laying Equipment Market are focusing on technology-driven differentiation to strengthen their competitive position. Leading manufacturers are investing in product innovation to enhance precision, reliability, and operational efficiency while reducing total ownership costs for customers. Strategic collaborations with rail authorities and infrastructure contractors are being pursued to secure long-term supply agreements and repeat business. Many players are expanding their regional footprints through localized manufacturing, service centers, and aftermarket support to improve responsiveness and customer retention. Digital integration, including advanced diagnostics and condition-based maintenance solutions, is also being prioritized to deliver value-added services.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment

- 2.2.3 Technology

- 2.2.4 Application

- 2.2.5 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid expansion of rail infrastructure worldwide

- 3.2.1.2 Technological advancements in track laying and maintenance equipment

- 3.2.1.3 Government investments and modernization programs

- 3.2.1.4 Urbanization, industrialization, and growing freight demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital expenditure and cost of equipment

- 3.2.2.2 Skilled labor shortage and training requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Automation and digitalization of rail construction and maintenance

- 3.2.3.2 Emerging markets and greenfield rail projects

- 3.2.3.3 Upgrading and modernizing existing rail infrastructure

- 3.2.3.4 Adoption of digital and automated track laying solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. Federal Railroad Administration (FRA) Regulations

- 3.4.1.2 Canada Transport Standards

- 3.4.2 Europe

- 3.4.2.1 Germany TUV & BaFin Compliance

- 3.4.2.2 France DGITM Guidelines

- 3.4.2.3 United Kingdom ORR Regulations

- 3.4.2.4 Italy Ministry of Infrastructure & Transport Compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China MIIT Guidelines

- 3.4.3.2 Japan MLIT Standards

- 3.4.3.3 South Korea MOLIT Regulations

- 3.4.3.4 India Ministry of Railways & BIS Guidelines

- 3.4.4 Latin America

- 3.4.4.1 Brazil ANTT & DENIT Regulations

- 3.4.4.2 Mexico SCT & FERROCARRILES Guidelines

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE Roads & Transport Authority (RTA) Guidelines

- 3.4.5.2 Saudi Arabia General Authority for Transport (GAT) Regulations

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Automation & robotics

- 3.7.1.2 AI & machine learning

- 3.7.1.3 Internet of things (IoT)

- 3.7.2 Emerging technologies

- 3.7.2.1 Hyper-connected rail networks

- 3.7.2.2 Robotics-as-a-service (RaaS) for track laying

- 3.7.2.3 AI-driven predictive maintenance & dynamic resource allocation

- 3.7.1 Current technological trends

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Equipment, 2022 - 2035 ($ Mn, Units)

- 5.1 Key trends

- 5.2 Track Laying Machines

- 5.3 Tamping Machines

- 5.4 Ballast Regulators

- 5.5 Sleeper Laying Machines

- 5.6 Welding Machines

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035 ($ Mn, Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automated

- 6.4 Fully Automated

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($ Mn, Units)

- 7.1 Key trends

- 7.2 New Railway Construction

- 7.3 Track Maintenance

- 7.4 Upgrades and Modernization

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 ($ Mn, Units)

- 8.1 Key trends

- 8.2 Public Rail Systems

- 8.3 Private Freight Companies

- 8.4 Private Passenger Operators

- 8.5 Defense

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Belgium

- 9.3.7 Netherlands

- 9.3.8 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Singapore

- 9.4.6 South Korea

- 9.4.7 Vietnam

- 9.4.8 Indonesia

- 9.4.9 Malaysia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Global Player

- 10.1.1 Balfour Beatty Rail

- 10.1.2 Enviri

- 10.1.3 Harsco Rail

- 10.1.4 Matisa

- 10.1.5 Plasser & Theurer

- 10.1.6 Salfec

- 10.1.7 Spenco

- 10.1.8 Tampertec

- 10.1.9 Vossloh

- 10.1.10 Weihua Group

- 10.2 Regional Player

- 10.2.1 Alstom Track Solutions

- 10.2.2 CRRC Railway Equipment

- 10.2.3 CSR Zhuzhou

- 10.2.4 Kinki Sharyo

- 10.2.5 Lloyds Register Rail

- 10.2.6 Orenstein & Koppel

- 10.2.7 Robel

- 10.2.8 Shandong Railway Construction Machinery

- 10.2.9 VAE Group

- 10.2.10 ZTR Rail

- 10.3 Emerging Players

- 10.3.1 Gulf Rail Technologies

- 10.3.2 Metro Track Systems

- 10.3.3 RailTech Innovations

- 10.3.4 RapidRail Machinery

- 10.3.5 TrackTech Solutions