|

시장보고서

상품코드

1928904

자동차용 에너지 회수 시스템 시장의 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Energy Recovery System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

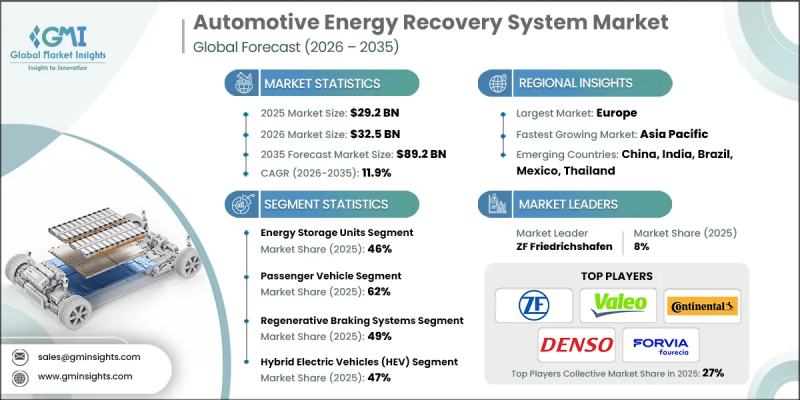

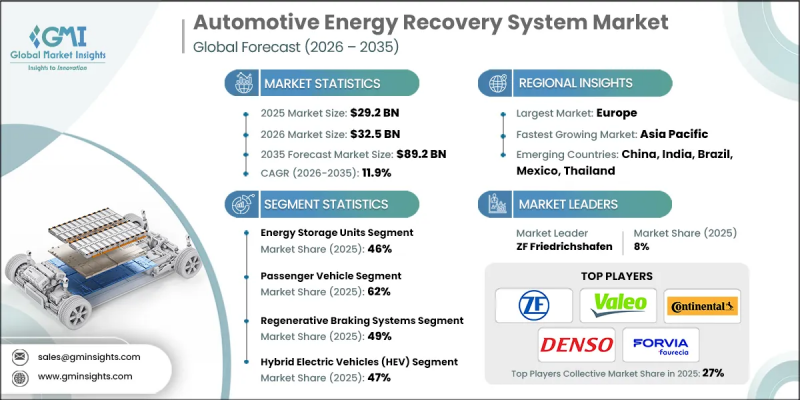

세계의 자동차용 에너지 회생 시스템 시장은 2025년에 292억 달러로 평가되었으며, 2035년까지 CAGR 11.9%로 성장하여 892억 달러에 달할 것으로 예측됩니다.

이러한 성장은 차량의 에너지 사용 효율 향상, 연료 소비 감소, 그리고 점점 더 엄격해지는 환경 규제에 대한 대응이 필요하기 때문입니다. 자동차 제조사들은 차량 운행 중 손실되는 에너지를 회수하고 재사용하는 시스템을 우선적으로 도입하고 있으며, 이를 통해 비용 효율성과 배기가스 배출량 감소라는 두 가지 목표를 모두 달성할 수 있습니다. 전기 및 하이브리드 파워트레인으로의 전환이 가속화되면서 에너지 회수 솔루션은 선택적 추가 기능이 아닌 차량 구조에 필수적인 요소로 자리 잡고 있습니다. 이러한 시스템은 주행거리 연장, 에너지 관리 최적화, 차량 전체 성능 향상에 도움을 줍니다. 세계 시장의 규제 압력으로 인해 자동차 제조업체들은 종합적인 에너지 최적화 전략을 지속적으로 추진하고 있습니다. 그 결과, 시장은 여러 회수 및 관리 기술이 첨단 파워트레인 플랫폼 내에서 함께 작동하는 완전히 통합된 시스템 수준의 솔루션으로 진화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시시 가치 | 292억 달러 |

| 예측 금액 | 892억 달러 |

| CAGR | 11.9% |

에너지 저장장치 부문은 2025년 46%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 12.2%의 성장률을 기록할 것으로 전망됩니다. 이 부문이 선도적인 위치에 있는 이유는 회수된 에너지를 효율적으로 저장하고 재사용하여 측정 가능한 성능과 효율성 향상을 달성해야 하기 때문입니다. 에너지 저장 솔루션은 전동화 및 하이브리드 차량 플랫폼 전반에 걸쳐 추진 요구 사항, 보조 시스템 및 종합적인 전력 관리를 지원합니다. 회수 시스템과의 통합은 에너지 재사용을 극대화하고 운영 효율성을 향상시키는 데 필수적입니다.

승용차 부문은 2025년 62%의 점유율을 차지했으며, 2035년까지 CAGR 12%로 성장할 것으로 전망됩니다. 이러한 성장은 연비 효율과 저공해 차량에 대한 소비자의 관심 증가, 지원적인 정책 프레임워크, 가격대를 불문한 전기 모델의 보급 확대에 힘입은 바 큽니다. 첨단 회수 솔루션은 고급차 부문과 양산차 부문 모두에서 점점 더 많이 채택되고 있습니다.

독일의 자동차 에너지 회수 시스템 시장은 2026년부터 2035년까지 CAGR 10%로 성장할 것으로 예상됩니다. 중국의 강력한 자동차 제조 기반과 배출가스 감축에 대한 규제적 초점이 여러 차량 카테고리에서 첨단 회수 기술의 통합을 가속화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률 분석

- 비용 구조

- 각 단계의 부가가치

- 밸류체인에 영향을 미치는 요인

- 디스럽션

- 업계에 대한 영향요인

- 성장 촉진요인

- 전기자동차 및 하이브리드 자동차 보급 확대

- 엄격한 배출가스 규제 및 연비 기준

- 에너지 회수 기술 진전

- 친환경적이고 비용 효율적인 차량에 대한 소비자 수요 증가

- 교통 정체와 도시화 압력

- 업계의 잠재적 리스크와 과제

- 에너지 회수 시스템의 높은 초기 비용

- 소비자 사이의 에너지 회수 기술에 관한 인지도와 이해도의 부족

- 시장 기회

- 전기자동차 및 하이브리드 자동차 보급 확대

- 보다 엄격한 배출가스 규제 및 연비 효율 규제

- 플릿 및 상용차 효율성에 대한 관심 상승

- 에너지 저장 기술로 파워 일렉트로닉스의 진보

- 신흥 자동차 시장의 새로운 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국 - 환경 보호 청(EPA) MY2027+기준

- 캐나다 - 캐나다 ZEV 프로그램

- 유럽

- 독일 - EU 이산화탄소 배출 기준(2030년까지 37.5% 감축)

- 영국 - 영국 ZEV 의무(2035년까지 신차 판매의 100%를 제로 에미션 차량으로)

- 프랑스 - 보너스-말러스 제도

- 이탈리아 - 국가회복·탄력성계획(PNRR)

- 아시아태평양

- 중국 - 신에너지차(NEV) 도입 의무

- 인도 - FAME-II 프로그램

- 일본 - 하이브리드 자동차·전기자동차에 대한 경제 산업성 보조금

- 호주 - 국가 전기자동차 전략

- LATAM

- 멕시코 - NOM-163-SCFI-2013 배출가스 기준

- 아르헨티나 - 연비 규제

- 중동 및 아프리카

- 남아프리카공화국 - 도로 교통 배출가스 기준

- 사우디아라비아 - 국가 산업 개발·물류 프로그램

- 북미

- Porters 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 특허 분석

- 사용 사례와 성공 사례

- 지속가능성과 환경면

- 지속가능한 실천

- 폐기물 절감 전략

- 생산의 에너지 효율

- 친환경 이니셔티브

- 탄소발자국에 관한 고려사항

- 향후 전망과 기회

- OEM 통합과 차량 아키텍처 적합성

- 패키징 제약(공간, 중량, 열)

- 기존 파워트레인 및 브레이크 시스템과의 통합

- 플랫폼 레벨에서의 준비 상황(내연기관 vs 하이브리드 vs BEV 스케이트보드)

- 교정 및 검증의 과제

- 비용 편익 및 회수기간 분석

- 차량당 비용 프리미엄

- 연비·항속거리 향상과 추가 비용의 비교

- 차종별 회수기간

- 플릿과 승용차 경제성 비교

- ERS 성능 벤치마크

- 소프트웨어, 제어 시스템 및 에너지 관리 인텔리전스

- 열 관리 및 방열 제약

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병

- 제휴·협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추정 및 예측 : 구성요소별, 2022-2035

- 에너지 저장 유닛

- 전지

- 슈퍼커패시터

- 플라이휠

- 에너지 변환 유닛

- 전동기/발전기

- 유압식 또는 공압식 컨버터

- 제어 유닛

- 전자 제어 모듈(ECM)

- 전력 관리 시스템

제6장 시장 추정 및 예측 : 차량별, 2022-2035

- 승용차

- 해치백

- SUV

- 세단

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

- 전기자동차 및 하이브리드 자동차

제7장 시장 추정 및 예측 : 시스템별, 2022-2035

- 운동 에너지 회생 시스템(KERS)

- 회생 제동 시스템

- 배기 에너지 회수 시스템(EERS)

- 서스펜션 기반 에너지 회수 시스템

제8장 시장 추정 및 예측 : 추진력별, 2022-2035

- 내연기관차

- 하이브리드 전기자동차(HEV)

- 플러그인 하이브리드 전기자동차(PHEV)

- 배터리식 전기자동차(BEV)

제9장 시장 추정 및 예측 : 용도별, 2022-2035

- 제동 에너지 회생

- 폐열 회수

- 열 관리 및 폐열 이용

- 파워트레인 효율 향상

- 연비 향상

- 성능 향상

- 기타

제10장 시장 추정 및 예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 베네룩스

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 싱가포르

- 태국

- 인도네시아

- 베트남

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

제11장 기업 개요

- 세계 플레이어

- Aisin Seiki

- BorgWarner

- Continental

- Cummins

- Denso

- Forvia

- Hitachi Automotive Systems

- Hyundai Mobis

- Mahle

- Mitsubishi Electric

- Robert Bosch

- Schaeffler

- Valeo

- ZF Friedrichshafen

- 지역별 기업

- Kongsberg Automotive

- Mando

- Nabtesco

- Tenneco

- TRW Automotive

- Emerging Technology 이노베이터

- BYD Auto

- Leoni

- Nidec

- Rimac Automobili

The Global Automotive Energy Recovery System Market was valued at USD 29.2 billion in 2025 and is estimated to grow at a CAGR of 11.9% to reach USD 89.2 billion by 2035.

Growth is driven by the need to improve vehicle energy utilization, lower fuel consumption, and meet increasingly strict environmental standards. Automotive manufacturers are prioritizing systems that capture and reuse energy that would otherwise be lost during vehicle operation, supporting both cost efficiency and emission reduction goals. The accelerating shift toward electric and hybrid powertrains is further reinforcing demand, as energy recovery solutions are becoming integral to vehicle architecture rather than optional add-ons. These systems support extended driving range, optimized energy management, and improved overall vehicle performance. Regulatory pressure across global markets continues to push automakers toward comprehensive energy optimization strategies. As a result, the market is evolving toward fully integrated system-level solutions where multiple recovery and management technologies operate together within advanced powertrain platforms.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $29.2 Billion |

| Forecast Value | $89.2 Billion |

| CAGR | 11.9% |

The energy storage units segment held a 46% share in 2025 and is forecast to grow at a CAGR of 12.2% from 2026 to 2035. This segment leads because recovered energy must be efficiently stored and redeployed to deliver measurable performance and efficiency benefits. Energy storage solutions support propulsion requirements, auxiliary systems, and overall power management across electrified and hybrid vehicle platforms. Their integration with recovery systems is central to maximizing energy reuse and improving operational efficiency.

The passenger vehicle category accounted for 62% share in 2025 and is projected to grow at a CAGR of 12% through 2035. Growth is supported by rising consumer interest in fuel-efficient and low-emission vehicles, combined with supportive policy frameworks and broader availability of electrified models across pricing tiers. Advanced recovery solutions are increasingly incorporated across both premium and high-volume vehicle segments.

Germany Automotive Energy Recovery System Market is expected to grow at a CAGR of 10% between 2026 and 2035. The country's strong automotive manufacturing base and regulatory focus on emissions reduction are accelerating the integration of advanced recovery technologies across multiple vehicle categories.

Key companies operating in the Global Automotive Energy Recovery System Market include Robert Bosch, Continental, ZF Friedrichshafen, Valeo, Schaeffler, Denso, Hyundai Mobis, Mahle, Forvia, and Mando. Companies in the Global Automotive Energy Recovery System Market are strengthening their competitive positions through continuous innovation and strategic integration. Manufacturers are investing heavily in research and development to improve system efficiency, reduce weight, and enhance compatibility with electrified powertrains. Collaboration with automakers is being prioritized to enable early-stage integration into vehicle platforms. Many players are expanding modular and scalable solutions to serve multiple vehicle categories. Geographic expansion and localization strategies help suppliers meet regional regulatory and cost requirements.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicles

- 2.2.4 System

- 2.2.5 Propulsion

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Increasing adoption of electric and hybrid vehicles

- 3.2.1.3 Stringent emission regulations and fuel efficiency standards

- 3.2.1.4 Advancements in energy recovery technologies

- 3.2.1.5 Growing consumer demand for environmentally friendly and cost-efficient vehicles

- 3.2.1.6 Traffic congestion & urbanization pressures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial costs of energy recovery systems

- 3.2.2.2 Limited awareness and understanding of energy recovery technologies among consumers

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of electric and hybrid vehicles.

- 3.2.3.2 Stricter emission and fuel efficiency regulations.

- 3.2.3.3 Growing focus on fleet and commercial vehicle efficiency.

- 3.2.3.4 Advancements in energy storage and power electronics.

- 3.2.3.5 Emerging opportunities in developing automotive markets.

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- EPA MY2027+ standards

- 3.4.1.2 Canada - Canadian ZEV program

- 3.4.2 Europe

- 3.4.2.1 Germany- EU CO2 standards (37.5% reduction by 2030)

- 3.4.2.2 UK- UK ZEV mandate (100% new car sales zero-emission by 2035)

- 3.4.2.3 France- Bonus-malus incentive program

- 3.4.2.4 Italy- National Recovery and Resilience Plan (PNRR)

- 3.4.3 Asia Pacific

- 3.4.3.1 China- New Energy Vehicle (NEV) mandate

- 3.4.3.2 India- FAME-II program

- 3.4.3.3 Japan- METI subsidies for hybrid/electric vehicles

- 3.4.3.4 Australia- National Electric Vehicle Strategy

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM-163-SCFI-2013 emissions standard

- 3.4.4.2 Argentina- Fuel economy regulation

- 3.4.5 MEA

- 3.4.5.1 South Africa- Road Traffic Emissions Standards

- 3.4.5.2 Saudi Arabia- National Industrial Development and Logistics Program

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Use cases & success stories

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Future outlook and opportunities

- 3.12 OEM Integration & Vehicle Architecture Fit

- 3.12.1 Packaging constraints (space, weight, thermal)

- 3.12.2 Integration with existing powertrain & braking systems

- 3.12.3 Platform-level readiness (ICE vs hybrid vs BEV skateboards)

- 3.12.4 Calibration & validation challenges

- 3.13 Cost-Benefit & Payback Analysis

- 3.13.1 Cost premium per vehicle

- 3.13.2 Fuel economy / range gains vs added cost

- 3.13.3 Payback period by vehicle type

- 3.13.4 Fleet vs passenger economics

- 3.14 ERS Performance Benchmarking

- 3.15 Software, Controls & Energy Management Intelligence

- 3.16 Thermal Management & Heat Rejection Constraints

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Energy storage units

- 5.2.1 Batteries

- 5.2.2 Supercapacitors

- 5.2.3 Flywheels

- 5.3 Energy conversion units

- 5.3.1 Electric motors/generators

- 5.3.2 Hydraulic or pneumatic converters

- 5.4 Control units

- 5.4.1 Electronic control modules (ECM)

- 5.4.2 Power management systems

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 SUV

- 6.2.3 Sedan

- 6.3 Commercial Vehicles

- 6.3.1 Light commercial vehicles (LCVs)

- 6.3.2 Medium commercial vehicles (MCVs)

- 6.3.3 Heavy commercial vehicles (HCVs)

- 6.4 Electric and hybrid vehicles

Chapter 7 Market Estimates & Forecast, By System, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Kinetic energy recovery systems (KERS)

- 7.3 Regenerative braking systems

- 7.4 Exhaust energy recovery systems (EERS)

- 7.5 Suspension-based energy recovery systems

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Internal combustion engine (ICE) vehicles

- 8.3 Hybrid electric vehicles (HEV)

- 8.4 Plug-in hybrid electric vehicles (PHEV)

- 8.5 Battery electric vehicles (BEV)

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Braking energy recovery

- 9.3 Exhaust heat recovery

- 9.4 Thermal management & waste heat utilization

- 9.5 Powertrain efficiency enhancement

- 9.6 Fuel economy improvement

- 9.7 Performance boosting

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Benelux

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aisin Seiki

- 11.1.2 BorgWarner

- 11.1.3 Continental

- 11.1.4 Cummins

- 11.1.5 Denso

- 11.1.6 Forvia

- 11.1.7 Hitachi Automotive Systems

- 11.1.8 Hyundai Mobis

- 11.1.9 Mahle

- 11.1.10 Mitsubishi Electric

- 11.1.11 Robert Bosch

- 11.1.12 Schaeffler

- 11.1.13 Valeo

- 11.1.14 ZF Friedrichshafen

- 11.2 Regional Players

- 11.2.1 Kongsberg Automotive

- 11.2.2 Mando

- 11.2.3 Nabtesco

- 11.2.4 Tenneco

- 11.2.5 TRW Automotive

- 11.3 Emerging Technology Innovators

- 11.3.1 BYD Auto

- 11.3.2 Leoni

- 11.3.3 Nidec

- 11.3.4 Rimac Automobili