|

시장보고서

상품코드

1928905

메틸에틸케톤 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Methyl Ethyl Ketone (MEK) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

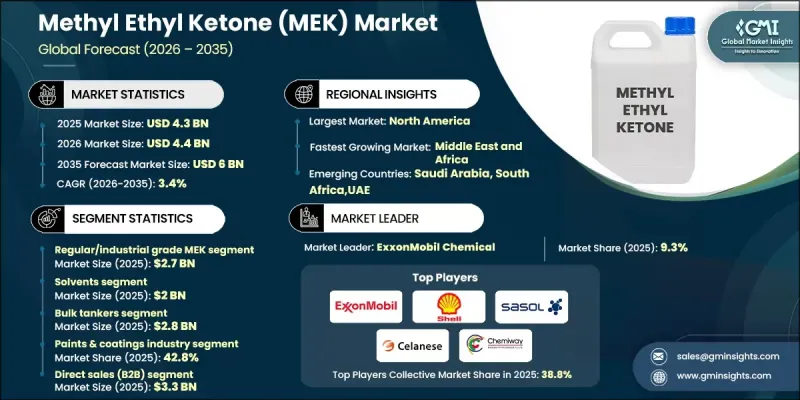

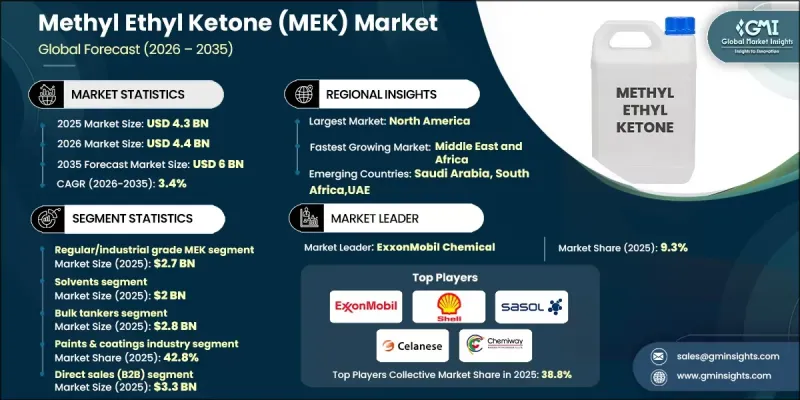

세계의 메틸에틸케톤(MEK) 시장은 2025년에 43억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 3.4%로 성장하여 60억 달러에 이를 것으로 예측됩니다.

MEK(일반명: 부타논)는 무색의 휘발성이 높은 액체로 날카로운 단맛이 나는 냄새와 가연성을 가지고 있습니다. 우수한 용해성, 빠른 증발 속도, 수지, 페인트, 접착제, 잉크의 용해 능력으로 널리 인정받고 있습니다. 시장 성장은 주로 페인트 및 코팅, 접착제, 인쇄 잉크, 고무 가공, 화학 제조 등의 산업 수요에 힘입어 성장하고 있습니다. 건설, 자동차 생산, 포장 등의 확장 분야가 지속적인 소비를 뒷받침하며 꾸준한 시장 확대를 추진하고 있습니다. 지역별로 성장률은 제조 밀도, 환경 규제, 용제 대체 동향에 따라 차이가 있습니다. 경쟁력을 유지하기 위해 공급업체들은 신뢰할 수 있는 공급망, 비용 효율성, 안전 및 환경 기준 준수에 초점을 맞추었습니다. MEK는 다양한 제조 분야의 표면 코팅, 보호 마감, 특수 화학 응용 분야에서 여전히 필수적인 산업용 용임베디드니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 43억 달러 |

| 예측 금액 | 60억 달러 |

| CAGR | 3.4% |

일반용 또는 산업용 MEK 부문은 2025년 27억 달러의 매출을 기록할 것으로 예측됩니다. 산업용 등급의 MEK는 다용도성과 범용성으로 인해 코팅, 접착제, 세정 공정 등 다양한 분야에서 선호되고 있습니다. 한편, 전자 등급 MEK는 반도체 제조 및 회로 세척의 고순도 용도에 맞게 설계되었으며, 제약 등급 MEK는 의약품 제조에 필요한 엄격한 순도 및 안전 기준을 충족합니다.

포장 형태별로는 벌크 탱커 부문이 2025년 28억 달러에 달할 것으로 예측됩니다. 벌크 탱커는 대량의 MEK를 필요로 하는 대규모 산업 바이어에게 비용 효율적인 운송 및 취급을 제공합니다. 중간 벌크 컨테이너(IBC)는 용량과 편의성의 균형을 제공하며, 중간 규모의 사업에서 보관 및 물류 간소화를 위해 널리 이용되고 있습니다.

북미 메틸에틸케톤(MEK) 시장은 2025년 22억 달러 규모를 차지할 것으로 예상되며, 2035년에는 31억 달러에 달할 것으로 예측됩니다. 이 지역 시장은 엄격한 환경 규제의 영향을 받아 VOC 배출량 감소와 청정 용매의 채택을 촉진하고 있습니다. 성숙한 산업기반으로 인해 페인트, 접착제, 화학 제조 분야의 MEK 수요는 안정적이지만, 규제 압력에 대응하기 위해 제조업체들이 대체 용매를 찾고 있기 때문에 성장은 완만하게 이루어지고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 페인트 및 코팅 산업으로부터 수요 증가

- 제조 활동 확대

- 자동차 및 항공우주 분야 성장

- 업계의 잠재적 리스크&과제

- 원재료 가격 변동성

- 높은 가연성과 휘발성

- 시장 기회

- 저배출 한편 지속가능MEK 등급 개발

- 포장 및 표시 용도 확대

- 용제 회수·재활용 시스템 도입

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter의 Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 가격 동향

- 지역별

- 등급별

- 향후 시장 동향

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 특허 동향

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추산·예측 : 등급별, 2022-2035

- 일반/산업용 등급 MEK

- 전자 등급 MEK

- 의약품 등급 MEK

- 우레탄 등급 MEK

- ACS 시약 등급 MEK

- HPLC 등급 MEK

제6장 시장 추산·예측 : 용도별, 2022-2035

- 용제

- 유성 도료·라텍스 페인트 스키닝 방지제

- 접착제 및 실란트

- 인쇄 잉크

- 수지

- 화학 중간체

- 기타

제7장 시장 추산·예측 : 포장 형태별, 2022-2035

- 벌크(탱커)

- 중간 벌크 컨테이너(IBC)

- 드럼통

- 페일 캔·소형 용기

- 특수 포장

제8장 시장 추산·예측 : 최종 이용 산업별, 2022-2035

- 페인트 및 코팅 산업

- 자동차

- 건설

- 포장

- 일렉트로믹스 및 반도체

- 의약품 및 의료

- 항공우주

- 섬유 및 피혁 산업

- 고무 산업

- 기타

제9장 시장 추산·예측 : 유통 채널별, 2022-2035

- 직접 판매(B2B)

- 온라인 플랫폼/E-Commerce

- 기타

제10장 시장 추산·예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트

- 기타 중동 및 아프리카

제11장 기업 개요

- Arkema S.A.

- Genomatica

- LanzaTech(Carbon Capture to Chemicals)

- Vertec Biosolvents

- Celanese Corporation

- Cetex Petrochemicals

- Eastman Chemical Company

- ExxonMobil Corporation

- INEOS Group

- Idemitsu Kosan Co., Ltd.

- LG Chem Ltd.

- Maruzen Petrochemical Co., Ltd.

- Nouryon

- PTT Global Chemical Public Company Limited

- Sasol Limited

- Shell Chemicals(Shell Plc)

- Solvay S.A.

- SK Energy

- PetroChina Company Limited

- Mitsubishi Chemical Corporation

The Global Methyl Ethyl Ketone (MEK) Market was valued at USD 4.3 billion in 2025 and is estimated to grow at a CAGR of 3.4% to reach USD 6 billion by 2035.

MEK, commonly known as butanone, is a colorless, highly volatile liquid with a sharp, sweet odor and flammable properties. It is widely recognized for its excellent solvency, rapid evaporation, and capacity to dissolve resins, coatings, adhesives, and inks. The market growth is primarily fueled by demand from industries such as paints and coatings, adhesives, printing inks, rubber processing, and chemical manufacturing. Expanding sectors, including construction, automotive production, and packaging, are supporting sustained consumption, driving steady market expansion. Regional growth varies due to manufacturing density, environmental regulations, and trends toward solvent substitution. To stay competitive, suppliers focus on reliable supply chains, cost efficiency, and compliance with safety and environmental standards. MEK remains an essential industrial solvent for surface coatings, protective finishes, and specialized chemical applications across diverse manufacturing sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.3 Billion |

| Forecast Value | $6 Billion |

| CAGR | 3.4% |

The regular or industrial-grade MEK segment generated USD 2.7 billion in 2025. Industrial-grade MEK is preferred for broad applications, including coatings, adhesives, and cleaning processes, due to its versatile, general-purpose performance. In contrast, electronic-grade MEK is tailored for high-purity applications in semiconductor production and circuit cleaning, while pharmaceutical-grade MEK meets the stringent purity and safety standards required for drug manufacturing.

In terms of packaging, the bulk tankers segment reached USD 2.8 billion in 2025. Bulk tankers serve large industrial buyers needing high volumes of MEK, offering cost-effective transportation and handling. Intermediate Bulk Containers (IBCs) provide a balance between volume and convenience, widely used in medium-scale operations for easier storage and logistics.

North America Methyl Ethyl Ketone (MEK) Market accounted for USD 2.2 billion in 2025 and is projected to reach USD 3.1 billion by 2035. The market in this region is influenced by stringent environmental regulations, driving lower VOC emissions and cleaner solvent adoption. A mature industrial base ensures stable demand for MEK in coatings, adhesives, and chemical manufacturing, though growth is moderated as manufacturers explore alternative solvents in response to regulatory pressures.

Key players in the Global Methyl Ethyl Ketone (MEK) Market include Celanese Corporation, Solvay S.A., Arkema S.A., Eastman Chemical Company, ExxonMobil Corporation, Genomatica, LanzaTech (Carbon Capture to Chemicals), SK Energy, PTT Global Chemical Public Company Limited, Vertec Biosolvents, Idemitsu Kosan Co., Ltd., LG Chem Ltd., Maruzen Petrochemical Co., Ltd., Sasol Limited, Shell Chemicals (Shell Plc), PetroChina Company Limited, Nouryon, Cetex Petrochemicals, and Mitsubishi Chemical Corporation. Companies in the Global Methyl Ethyl Ketone (MEK) Market strengthen their presence through strategic investments in production efficiency, sustainability, and technological innovation. Manufacturers focus on expanding production capacity while optimizing cost structures to remain competitive. Research and development initiatives target cleaner solvent alternatives, improved solvent performance, and regulatory compliance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Purity Grade

- 2.2.2 Application

- 2.2.3 Packaging Type

- 2.2.4 End Use Industry

- 2.2.5 Distribution Channel

- 2.2.6 Regional

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand from paints and coatings industry

- 3.2.1.2 Expansion of manufacturing activities

- 3.2.1.3 Automotive and aerospace sector growth

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw material price volatility

- 3.2.2.2 High flammability and volatility

- 3.2.3 Market opportunities

- 3.2.3.1 Development of low-emission and sustainable MEK grades

- 3.2.3.2 Expansion in packaging and labeling applications

- 3.2.3.3 Adoption of solvent recovery and recycling systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By grade

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Grade, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Regular/Industrial Grade MEK

- 5.3 Electronic grade MEK

- 5.4 Pharmaceutical grade MEK

- 5.5 Urethane grade MEK

- 5.6 ACS reagent grade MEK

- 5.7 HPLC grade MEK

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solvents

- 6.3 Anti-skinning agent in oil/latex paints

- 6.4 Adhesives & sealants

- 6.5 Printing inks

- 6.6 Resins

- 6.7 Chemical intermediates

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Packaging Type, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bulk (tankers)

- 7.3 Intermediate bulk container (IBC)

- 7.4 Drums

- 7.5 Pails & small containers

- 7.6 Specialty packaging

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Paints & coatings industry

- 8.3 Automotive

- 8.4 Construction

- 8.5 Packaging

- 8.6 Electronics & semiconductors

- 8.7 Pharmaceuticals & healthcare

- 8.8 Aerospace

- 8.9 Textiles & leather

- 8.10 Rubber industry

- 8.11 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Direct sales (B2B)

- 9.3 Online platforms/E-commerce

- 9.4 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Arkema S.A.

- 11.2 Genomatica

- 11.3 LanzaTech (Carbon Capture to Chemicals)

- 11.4 Vertec Biosolvents

- 11.5 Celanese Corporation

- 11.6 Cetex Petrochemicals

- 11.7 Eastman Chemical Company

- 11.8 ExxonMobil Corporation

- 11.9 INEOS Group

- 11.10 Idemitsu Kosan Co., Ltd.

- 11.11 LG Chem Ltd.

- 11.12 Maruzen Petrochemical Co., Ltd.

- 11.13 Nouryon

- 11.14 PTT Global Chemical Public Company Limited

- 11.15 Sasol Limited

- 11.16 Shell Chemicals (Shell Plc)

- 11.17 Solvay S.A.

- 11.18 SK Energy

- 11.19 PetroChina Company Limited

- 11.20 Mitsubishi Chemical Corporation