|

시장보고서

상품코드

1928914

질소 가스 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Nitrogen Gas Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

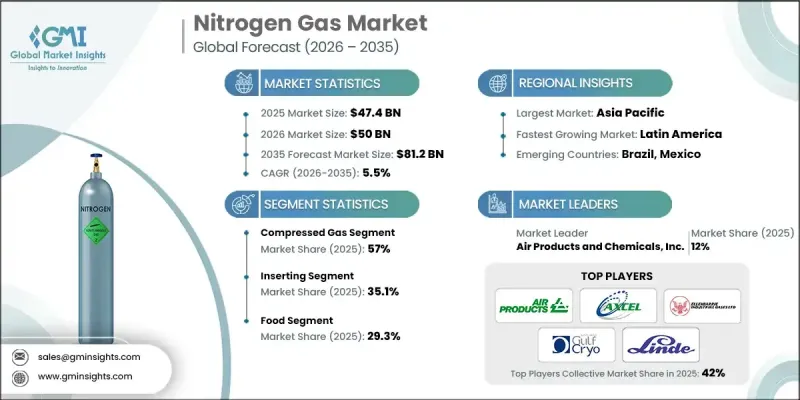

세계의 질소 가스 시장은 2025년에 474억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.5%로 성장하여 812억 달러에 이를 것으로 예측됩니다.

이러한 성장은 에너지 집약적 산업의 생산 활동 증가로 인해 불활성화, 블랭킷 처리 및 공정 보호 응용 분야에서 질소 사용량이 증가함에 따라 주도되고 있습니다. 또한, 첨단 생명과학 제조 분야의 생산 확대도 수요를 뒷받침하고 있으며, 질소는 제어 환경, 보존, 안정화 공정에 널리 활용되고 있습니다. 고순도 질소는 민감한 생물학적 물질의 보존 및 첨단 치료제 제조 공정에서 지속적으로 채택이 확대되고 있습니다. 전자기기 및 반도체 생산의 급속한 확대도 소비량 증가에 기여하고 있으며, 질소는 제조 공정에서 제어 분위기 유지에 중요한 역할을 하고 있습니다. 동시에, 생산자들은 공기 분리 기술 향상과 청정 전력 및 열원 통합을 통해 에너지 효율을 개선하고 배출을 줄이는 것을 우선시하고 있습니다. 중공업 분야의 최종 사용자는 공급 신뢰성을 높이고 운송 관련 배출량을 줄이면서 현장 생성 시스템 및 파이프라인 공급 모델로의 전환을 가속화하고 있습니다. 이러한 복합적인 요인들이 여러 산업 분야에서 장기적인 시장 확대를 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 474억 달러 |

| 예측 금액 | 812억 달러 |

| CAGR | 5.5% |

압축 질소 부문은 2025년 57%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 5.3%의 성장률을 보일 것으로 예측됩니다. 공급업체는 압축 형태와 액체 형태를 모두 제공함으로써 이익을 얻고 있으며, 각기 다른 운영 요구 사항을 지원합니다. 압축 질소는 실린더, 번들 또는 벌크 시스템을 통해 공급되는 일상적인 산업 공정에서 널리 사용됩니다. 한편, 액체 질소는 급속하고 고강도의 냉각과 극저온 성능을 필요로 하는 응용 분야에 필수적입니다.

삽입 부문은 2025년 35.1%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 14.8%를 나타낼 것으로 예측됩니다. 블랭킹, 퍼징 및 관련 기능과 함께 질소 기반 솔루션은 운영 안전성 향상, 오염 위험 감소, 점점 더 엄격해지는 품질 및 안전 표준에 대응하기 위해 여러 산업 분야에서 표준화가 진행되고 있습니다.

북미 질소 가스 시장 세분화는 2025년에 미화 119억 달러에 달했습니다. 이러한 성장은 다양한 산업 기반과 파이프라인 유통 및 현장 질소 생성을 위한 성숙한 인프라, 그리고 첨단 제조 분야에서의 활동 증가에 의해 뒷받침되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 증가하는 산업 생산과 제조업 생산

- 식품 가공 및 콜드체인 물류 성장

- 제약, 바이오테크놀러지, 반도체 분야 확대

- 업계의 잠재적 리스크&과제

- 공기 분리 플랜트 고에너지 비용

- 현지 발전에 의한 대량 배송량 삭감

- 시장 기회

- 친환경 저탄소 질소 생산 도입

- 신흥 시장 산업 화와 인프라 정비

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter의 Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 형태별

- 향후 시장 동향

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 특허 상황

- 무역 통계(HS코드)

(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추산·예측 : 형태별, 2022-2035

- 압축 가스

- 고압 봄베

- 벌크/튜브 트레일러

- 현지 생성 압축 질소

- 액체 질소 가스

- 벌크 저장탱크

- 듀워/휴대용 용기

- 온사이트 극저온 플랜트

제6장 시장 추산·예측 : 용도별, 2022-2035

- 불활성화

- 반응기 및 용기 불활성화

- 저장탱크 불활성화

- 파이프라인 불활성화

- 브란켓팅

- 식품 및 음료 헷드스페이스브란케팅

- 화학제품·용제 탱크용 브란케팅

- 석유·연료 저장용 브란케팅

- 용접·절단

- 금속 용접용 실드 가스 혼합 가스

- 레이저 절단 및 플라즈마 절단 지원

- 열처리 및 납땜용 분위기

- 퍼징

- 파이프라인 및 프로세스 라인 퍼징

- 설비 기동시 및 정지시 퍼징

- 유지보수 및 안전 작업을 위한 퍼징

- 기타

제7장 시장 추산·예측 : 최종 이용 산업별, 2022-2035

- 화장품

- 식품

- 자동차

- 의약품

- 기타

제8장 시장 추산·예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트

- 기타 중동 및 아프리카

제9장 기업 개요

- Air Products and Chemicals, Inc.

- Axcel Gases

- Ellenbarrie industrial Gases.

- Gulfcryo

- Linde PLC

- Messer Group

- Omega Air

- PARKER HANNIFIN CORP

- Praxair Technology, Inc.

- Southern Industrial Gas

- Universal Industrial Gases, Inc.

- Yingde Gases Group

The Global Nitrogen Gas Market was valued at USD 47.4 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 81.2 billion by 2035.

Growth is driven by rising production activity across energy-intensive industries, which has increased the use of nitrogen for inerting, blanketing, and process protection applications. Expanding output in advanced life science manufacturing has further supported demand, as nitrogen is widely used for controlled environments, preservation, and stabilization processes. High-purity nitrogen continues to see increased adoption in the storage of sensitive biological materials and in advanced therapeutic manufacturing workflows. The rapid expansion of electronics and semiconductor production has also contributed to higher consumption, as nitrogen plays a critical role in maintaining controlled atmospheres during fabrication. At the same time, producers are prioritizing improvements in energy efficiency and emissions reduction by enhancing air separation technologies and integrating cleaner power and heat sources. End users across heavy industries are increasingly shifting toward on-site generation systems and pipeline-based supply models, which improve supply reliability while lowering transportation-related emissions. These combined factors are reinforcing long-term market expansion across multiple industrial sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $47.4 Billion |

| Forecast Value | $81.2 Billion |

| CAGR | 5.5% |

The compressed nitrogen segment accounted for 57% share in 2025 and is forecast to grow at a CAGR of 5.3% through 2035. Suppliers benefit from offering both compressed and liquid formats, as each supports different operational requirements. Compressed nitrogen is widely used in routine industrial processes delivered via cylinders, bundles, or bulk systems, while liquid nitrogen is essential for applications requiring rapid and high-intensity cooling and cryogenic performance.

The inserting segment held a 35.1% share in 2025 and is expected to grow at a CAGR of 14.8% from 2026 to 2035. Along with blanketing, purging, and related functions, nitrogen-based solutions are becoming standardized across multiple industries to enhance operational safety, reduce contamination risks, and meet increasingly strict quality and safety standards.

North America Nitrogen Gas Market segment reached USD 11.9 billion in 2025. This growth is supported by a diverse industrial base and mature infrastructure for pipeline distribution and on-site nitrogen generation, alongside rising activity in advanced manufacturing sectors.

Key companies active in the Global Nitrogen Gas Market include Linde PLC, Air Products and Chemicals, Inc., Praxair Technology, Inc., Messer Group, Yingde Gases Group, PARKER HANNIFIN CORP, Gulfcryo, Omega Air, Ellenbarrie Industrial Gases, Universal Industrial Gases, Inc., Southern Industrial Gas, and Axcel Gases. Companies operating in the Global Nitrogen Gas Market are strengthening their market positions through capacity expansion, infrastructure investment, and technology optimization. Many players are focusing on on-site generation solutions and long-term supply agreements to secure stable demand and improve customer retention. Investments in advanced air separation systems are helping reduce operating costs and environmental impact. Strategic partnerships and geographic expansion are used to improve market reach, while portfolio diversification across purity levels and delivery modes allows suppliers to address a broader range of industrial requirements and maintain competitive differentiation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Form

- 2.2.3 Application

- 2.2.4 End Use Industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising industrial production and manufacturing output

- 3.2.1.2 Growth in food processing and cold-chain logistics

- 3.2.1.3 Expansion of pharma, biotech and semiconductor sectors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High energy costs for air separation plants

- 3.2.2.2 On-site generation reducing bulk delivery volumes

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of green, low-carbon nitrogen production

- 3.2.3.2 Emerging market industrialisation and infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By form

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Compressed gas

- 5.2.1 High-pressure cylinders

- 5.2.2 Bulk / tube trailers

- 5.2.3 On-site generated compressed nitrogen

- 5.3 Liquid nitrogen gas

- 5.3.1 Bulk storage tanks

- 5.3.2 Dewars / portable containers

- 5.3.3 On-site cryogenic plants

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Inerting

- 6.2.1 Reactor and vessel inerting

- 6.2.2 Storage tank inerting

- 6.2.3 Pipeline inerting

- 6.3 Blanketing

- 6.3.1 Food and beverage headspace blanketing

- 6.3.2 Chemical and solvent tank blanketing

- 6.3.3 Oil and fuel storage blanketing

- 6.4 Welding & cutting

- 6.4.1 Metal welding shielding gas blends

- 6.4.2 Laser cutting and plasma cutting support

- 6.4.3 Heat treatment and brazing atmospheres

- 6.5 Purging

- 6.5.1 Pipeline and process line purging

- 6.5.2 Start-up and shutdown purging of equipment

- 6.5.3 Purging for maintenance and safety operations

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Cosmetics

- 7.3 Food

- 7.4 Automotive

- 7.5 Pharmaceutical

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Air Products and Chemicals, Inc.

- 9.2 Axcel Gases

- 9.3 Ellenbarrie industrial Gases.

- 9.4 Gulfcryo

- 9.5 Linde PLC

- 9.6 Messer Group

- 9.7 Omega Air

- 9.8 PARKER HANNIFIN CORP

- 9.9 Praxair Technology, Inc.

- 9.10 Southern Industrial Gas

- 9.11 Universal Industrial Gases, Inc.

- 9.12 Yingde Gases Group