|

시장보고서

상품코드

1928970

연료전지 전기자동차 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Fuel Cell Electric Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

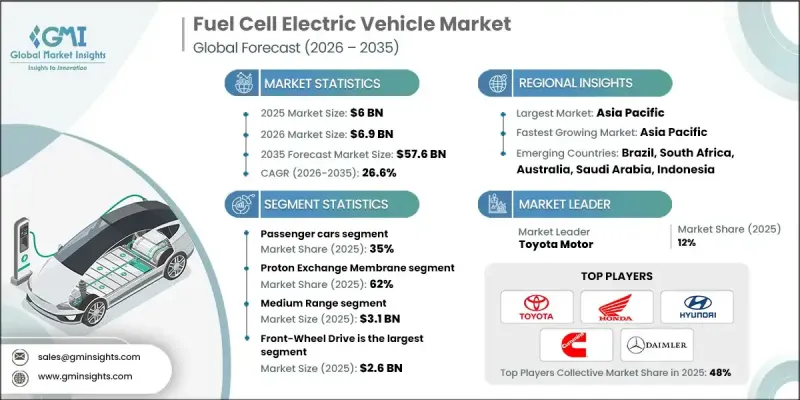

세계의 연료전지 전기자동차 시장은 2025년에 60억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 26.6%로 성장하여 576억 달러에 이를 것으로 예측됩니다.

이러한 성장은 장거리 주행 성능과 빠른 연료 보급 능력으로 인해 대중교통, 물류, 승용차 부문에서 연료전지 전기자동차의 채택이 확대되고 있는 데 따른 것입니다. 청정에너지 촉진을 위한 정부 정책, 보조금, 세제 혜택은 투자자들의 참여를 촉진하고 새로운 시장을 개척하여 산업의 확장을 더욱 가속화하고 있습니다. 공급망 혼란이 수소전기차 판매에 영향을 미치는 것,자동차 제조업체들은 수소 플랫폼 개발을 그 어느 때보다 가속화하고 있습니다. 각 업체들은 차세대 연료전지 기술을 선보이고, 상용화를 위한 양산형 차량을 준비하며 수송 부문의 탈탄소화에 대한 강한 의지를 보여주고 있습니다. 환경 인식이 높아지고 지속가능성 목표가 높아지면서 소비자와 정부 모두 무공해 모빌리티를 우선시하고 있으며, 각국이 온실가스 감축을 위해 노력하는 가운데 수소전기차의 매력은 점점 더 커지고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 60억 달러 |

| 예측 금액 | 576억 달러 |

| CAGR | 26.6% |

승용차 부문은 2025년 35% 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 27.8%로 성장할 것으로 전망됩니다. 승용 연료전지차(FCEV)는 자동차 제조업체들이 파워트레인 설계를 개선하고 일상적인 사용을 위한 통합을 최적화하면서 빠르게 발전하고 있습니다. 지속가능성과 저배출 모빌리티에 대한 소비자의 인식이 높아지면서 수소연료전지 승용차 보급이 가속화되고 있습니다. 각 제조업체들은 기존 내연기관차나 배터리 전기차의 성능에 필적하거나 이를 뛰어넘기 위해 항속거리 연장, 연료 보급 시간 단축, 차량 전체 효율 향상에 집중하고 있습니다. 첨단 인포테인먼트 시스템, 안전 기능, 커넥티비티 옵션도 현대 소비자의 기대에 부응하는 첨단 인포테인먼트 시스템, 안전 기능, 커넥티비티 옵션을 탑재했습니다.

양성자교환막(PEM) 연료전지 부문은 2025년 62%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 28.9%의 성장률을 보일 것으로 전망됩니다. PEM 연료전지는 기존 연료전지보다 낮은 온도에서 작동하기 때문에 빠른 시동, 잦은 스톱 앤 고(stop-and-go) 작동에 대한 적응성 향상, 열 관리 요구사항 감소가 가능합니다. 기술의 발전으로 고효율화, 내구성 향상, 백금 사용량 감소를 실현하여 상업적 용도의 성능 유지와 동시에 비용 경쟁력을 향상시키고 있습니다.

중국의 연료전지 전기자동차(FCEV) 시장은 2025년 17억 9,000만 달러 규모에 달할 것으로 예측됩니다. 정부 프로그램과 민간 투자가 수소전기차의 급속한 보급을 촉진하고 있으며, 국가 차원에서 수만 대의 연료전지차 도입을 위한 노력이 진행되고 있고, 여러 지방에서 수소 충전 인프라를 확충하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 원재료 공급업체

- 부품 공급업체

- 제조업체

- 기술 제공 기업

- 유통 채널

- 최종 용도

- 비용 구조

- 이익률

- 각 단계 부가가치

- 수직통합 동향

- 디스럽터

- 공급업체 상황

- 영향요인

- 성장 촉진요인

- 탈탄소화 의무와 배출 규제

- 수소 인프라 확충

- 물류·공공 교통 상용 플릿 도입

- 클린 차량용 장려책 및 보조금

- 업계의 잠재적 리스크&과제

- 수소 충전 인프라 부족

- 연료전지 시스템 내구성과 유지관리

- 시장 기회

- 배터리 하이브리드 및 연료전지 통합

- 수소 공급망과 그린 수소 도입

- 지역 수소 정책과 산업 제휴

- 자재 운반 및 니치 산업 차량 분야에의 사업 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국 NHTSA 저속 차량(LSV) 기준(FMVSS 500)

- 미국 각주 공도 주행 가능한 저속 차량(LSV) 규제

- 캐나다 운송 성 LSV 규제

- 유럽

- EU사륜 경자동차 카테고리 L6e/L7e

- 유엔 유럽 경제 위원회(UNECE) 자동차 안전 규제

- EU 배터리 규제

- EU폐차 지침

- 아시아태평양

- 중국 신에너지 차(NEV) 및 저속 차량(LSV) GB규격

- 인도 전기자동차용 CMVR 규칙

- 일본 국토 교통성 마이크로모빌리티 규제

- 라틴아메리카

- 브라질 CONTRAN 기준

- 아르헨티나 IRAM 규격

- 멕시코 NOM 차량 기준

- 중동 및 아프리카

- 사우디아라비아 SASO 규격

- 아랍에미리트(UAE) ESMA 규제

- GSO 걸프국가 전기자동차 기준

- 남아프리카공화국 SANS 규격

- 북미

- Porter의 Five Forces 분석

- PESTEL 분석

- 기술 동향과 혁신·에코시스템

- 현행 기술

- 신기술

- 가격 동향

- 지역별

- 제품별

- 특허 분석

- 생산 통계

- 생산 거점

- 소비 거점

- 수출입

- 지속가능성과 환경면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국에 관한 고려사항

- 저속 차량 실현 가능성과 도입에 관한 평가

- 총소유 비용(TCO) 벤치마크

- 배터리, 충전 시스템 및 파워트레인 실용성

- 공도 주행 합법성 및 컴플라이언스 경제성

- 용도 레벨에서의 투자수익률(ROI)과 회수기간

- 인프라 정비 상황과 운영 리스크

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금조달

제5장 시장 추산·예측 : 차량별, 2022-2035

- 승용차

- 세단

- 해치백차

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

- 이륜차 및 삼륜차

제6장 시장 추산·예측 : 연료전지별, 2022-2035

- 양성자 교환막

- 인산형 연료전지

- 고체 산화물 연료전지

제7장 시장 추산·예측 : 범위별, 2022-2035

- 단거리(250마일 미만)

- 중거리(250-500마일)

- 장거리(500마일 이상)

제8장 시장 추산·예측 : 구동 방식별, 2022-2035

- 전륜구동(FWD)

- 후륜구동(RWD)

- 총륜구동(AWD)

제9장 시장 추산·예측 : 용도별, 2022-2035

- 개인 이용

- 상용차

- 라스트 마일 배송

- 물류·화물 운송

- 라이드셰어링 및 공유 모빌리티

- 대중교통

- 산업용 및 자재 운반

- 정부 및 인프라 프로젝트

제10장 시장 추산·예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 개요

- 세계 기업

- Toyota Motor

- Hyundai Motor Company

- Honda Motor

- General Motors Company

- Daimler/Daimler Truck

- BMW

- Audi/Volkswagen

- Bosch

- Ballard Power Systems

- PowerCell Sweden

- Nikola

- Plug Power

- Hino Motors

- 지역 제조업체

- SAIC Motor

- Tata Motors

- Renault

- Nissan Motor

- First Automotive Works(FAW)

- Changan Automobile

- Yutong

- Foton

- Higer Bus

- 신규 기업

- Riversimple

- REV

The Global Fuel Cell Electric Vehicle Market was valued at USD 6 billion in 2025 and is estimated to grow at a CAGR of 26.6% to reach USD 57.6 billion by 2035.

Growth is driven by rising adoption of fuel cell electric vehicles in public transportation, logistics, and passenger vehicle segments due to their long-range performance and fast refueling capabilities. Government policies, subsidies, and tax incentives aimed at promoting clean energy are encouraging investor participation and opening new markets, further fueling industry expansion. Supply chain disruptions have affected FCEV sales, but automakers are accelerating the development of hydrogen platforms faster than ever before. Companies are showcasing next-generation fuel cell technologies and preparing production-level vehicles for commercial deployment, signaling a strong commitment to decarbonizing transportation. Growing environmental awareness and sustainability goals are motivating both consumers and governments to prioritize zero-emission mobility, making FCEVs increasingly appealing as countries strive to reduce greenhouse gas emissions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6 Billion |

| Forecast Value | $57.6 Billion |

| CAGR | 26.6% |

The passenger car segment held 35% share in 2025 and is expected to grow at a CAGR of 27.8% from 2026 to 2035. Passenger FCEVs are rapidly evolving as automakers refine powertrain designs and optimize integration for daily use. Increasing consumer awareness about sustainability and low-emission mobility is accelerating adoption of hydrogen-powered passenger cars. Manufacturers are focusing on enhancing driving range, reducing refueling times, and improving overall vehicle efficiency to match or exceed the performance of traditional internal combustion and battery electric vehicles. Advanced infotainment, safety features, and connectivity options are being incorporated to meet modern consumer expectations.

The proton exchange membrane (PEM) fuel cells segment held 62% share in 2025 and is projected to grow at a CAGR of 28.9% through 2035. PEM fuel cells operate at lower temperatures than conventional fuel cells, enabling quick start-ups, better adaptation to frequent stop-and-go driving, and reduced thermal management requirements. Advances are achieving high efficiencies, longer durability, and reduced platinum use, improving cost competitiveness while sustaining performance for commercial applications.

China Fuel Cell Electric Vehicle Market generated USD 1.79 billion in 2025. Government programs and private investments are driving rapid FCEV adoption, with national initiatives aiming to deploy tens of thousands of fuel cell vehicles while expanding hydrogen refueling infrastructure across multiple provinces.

Key players in the Global Fuel Cell Electric Vehicle Market include Bosch, Honda Motor, Ballard Power Systems, General Motors Company, Daimler, BMW, Toyota Motor, Volkswagen, Hyundai Motor Company, and PowerCell Sweden. Companies in the Global Fuel Cell Electric Vehicle Market are strengthening their position by investing heavily in R&D to enhance fuel cell efficiency, durability, and cost-effectiveness. They are forming strategic alliances with automotive manufacturers, technology providers, and infrastructure developers to accelerate vehicle deployment and expand global reach. Firms are actively developing hydrogen refueling networks, offering integrated mobility solutions, and standardizing vehicle platforms to improve interoperability. Additional strategies include optimizing supply chains, localizing production, launching pilot programs, and leveraging government incentives to build market credibility and drive adoption across public and commercial transportation sectors.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Fuel Cell

- 2.2.4 Range

- 2.2.5 Drive

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component suppliers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel

- 3.1.1.6 End Use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Decarbonization mandates & emissions regulations

- 3.2.1.2 Hydrogen infrastructure expansion

- 3.2.1.3 Commercial fleet adoption in logistics & public transport

- 3.2.1.4 Incentives & subsidies for clean vehicles

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Hydrogen refueling infrastructure scarcity

- 3.2.2.2 Fuel cell system durability & maintenance

- 3.2.3 Market opportunities

- 3.2.3.1 Battery-hybrid & fuel cell integration

- 3.2.3.2 Hydrogen supply chain & green hydrogen adoption

- 3.2.3.3 Regional hydrogen policies & industrial partnerships

- 3.2.3.4 Expansion into material handling and niche industrial vehicles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. NHTSA Low-Speed Vehicle (LSV) Standards (FMVSS 500)

- 3.4.1.2 U.S. State-Level Street-Legal LSV Rules

- 3.4.1.3 Canada Transport Canada LSV Regulations

- 3.4.2 Europe

- 3.4.2.1 EU Quadricycle Category L6e / L7e

- 3.4.2.2 UNECE Vehicle Safety Regulations

- 3.4.2.3 EU Battery Regulation

- 3.4.2.4 EU End-of-Life Vehicle Directive

- 3.4.3 Asia-Pacific

- 3.4.3.1 China GB Standards for NEVs and LSVs

- 3.4.3.2 India CMVR Rules for Electric Vehicles

- 3.4.3.3 Japan MLIT Micro-Mobility Regulations

- 3.4.4 Latin America

- 3.4.4.1 Brazil CONTRAN Standards

- 3.4.4.2 Argentina IRAM Standards

- 3.4.4.3 Mexico NOM Vehicle Standards

- 3.4.5 Middle East & Africa

- 3.4.5.1 Saudi Arabia SASO Standards

- 3.4.5.2 UAE ESMA Regulations

- 3.4.5.3 GSO Gulf Standards for Electric Vehicles

- 3.4.5.4 South Africa SANS Regulations

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology trends & innovation ecosystem

- 3.7.1 Current technologies

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Patent analysis

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Feasibility & adoption of low-speed vehicles assessment

- 3.12.1 Total Cost of Ownership (TCO) benchmarking

- 3.12.2 Battery, charging & powertrain viability

- 3.12.3 Street-legality & compliance economics

- 3.12.4 Application-level ROI & payback

- 3.12.5 Infrastructure readiness & operating risk

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger Cars

- 5.2.1 Sedans

- 5.2.2 Hatchbacks

- 5.2.3 SUVs

- 5.3 Commercial Vehicles

- 5.3.1 Light commercial vehicles (LCV)

- 5.3.2 Medium commercial vehicles (MCV)

- 5.3.3 Heavy commercial vehicles (HCV)

- 5.4 Two & Three Wheelers

Chapter 6 Market Estimates & Forecast, By Fuel Cell, 2022 - 2035 ($Bn, units)

- 6.1 Key trends

- 6.2 Proton Exchange Membrane

- 6.3 Phosphoric Acid Fuel Cell

- 6.4 Solid Oxide Fuel Cell

Chapter 7 Market Estimates & Forecast, By Range, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Short Range (Below 250 Miles)

- 7.3 Medium Range (250 - 500 Miles)

- 7.4 Long Range (Above 500 Miles)

Chapter 8 Market Estimates & Forecast, By Drive, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Front-Wheel Drive (FWD)

- 8.3 Rear-Wheel Drive (RWD)

- 8.4 All-Wheel Drive (AWD)

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Personal use

- 9.3 Commercial fleet

- 9.3.1 Last-mile delivery

- 9.3.2 Logistics & freight

- 9.3.3 Ride-hailing & shared mobility

- 9.4 Public transportation

- 9.5 Industrial & material handling

- 9.6 Government & infrastructure projects

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Toyota Motor

- 11.1.2 Hyundai Motor Company

- 11.1.3 Honda Motor

- 11.1.4 General Motors Company

- 11.1.5 Daimler / Daimler Truck

- 11.1.6 BMW

- 11.1.7 Audi / Volkswagen

- 11.1.8 Bosch

- 11.1.9 Ballard Power Systems

- 11.1.10 PowerCell Sweden

- 11.1.11 Nikola

- 11.1.12 Plug Power

- 11.1.13 Hino Motors

- 11.2 Regional players

- 11.2.1 SAIC Motor

- 11.2.2 Tata Motors

- 11.2.3 Renault

- 11.2.4 Nissan Motor

- 11.2.5 First Automotive Works (FAW)

- 11.2.6 Changan Automobile

- 11.2.7 Yutong

- 11.2.8 Foton

- 11.2.9 Higer Bus

- 11.3 Emerging players

- 11.3.1 Riversimple

- 11.3.2 REV