|

시장보고서

상품코드

1928983

자동차 도어 모듈 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Door Module Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

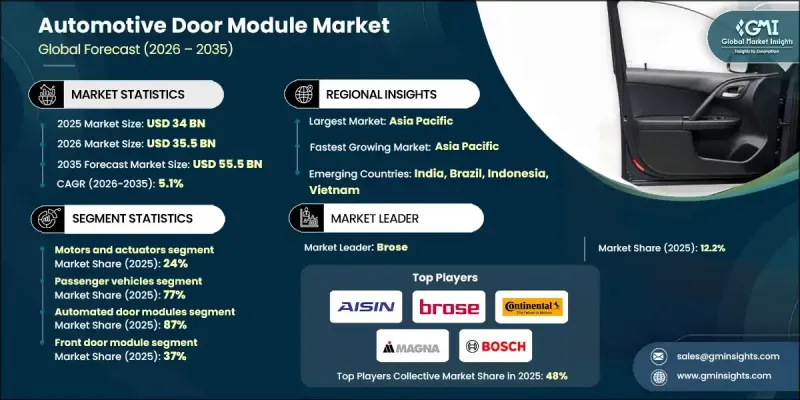

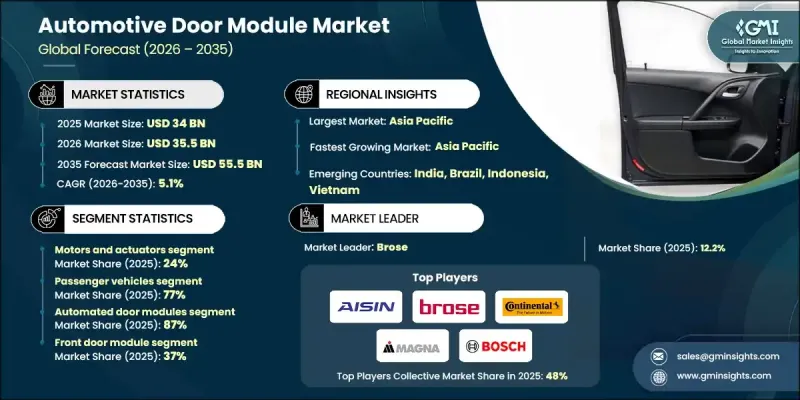

세계의 자동차 도어 모듈 시장은 2025년에 340억 달러로 평가되었으며, 2035년까지 CAGR 5.1%로 성장하여 555억 달러에 달할 것으로 예측됩니다.

시장 확대는 세계 자동차 생산의 꾸준한 성장과 현대 자동차의 편안함, 편의성, 안전 기술의 통합 발전에 의해 주도되고 있습니다. 전기 모빌리티로의 전환이 가속화되면서 도어 모듈 설계가 재구성되고 있으며, 효율성과 주행거리 최적화를 위한 경량 소재와 첨단 전자 시스템 채택이 촉진되고 있습니다. 자동차 제조업체들은 조립 시간 단축, 생산 워크플로우 효율화, 전체 제조 비용 절감을 위해 모듈식 차량 아키텍처에 대한 우선순위를 높이고 있습니다. 여러 개의 도어 관련 부품을 단일 모듈로 통합하여 설치 시간 단축, 품질 일관성 향상, 대량 생산 차량 플랫폼 전체에 대한 확장성을 실현합니다. 안전성과 사용 편의성 향상에 대한 소비자의 기대가 높아진 것도 시장 성장을 더욱 부추기고 있습니다. 출입 통제, 탑승자 보호 및 자동화 기능과 관련된 기능이 차량 카테고리 전반에 걸쳐 광범위하게 채택되고 있으며, 이는 OEM 제조업체의 통합 도어 모듈 솔루션의 대규모 도입을 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시시 가치 | 340억 달러 |

| 예측 금액 | 555억 달러 |

| CAGR | 5.1% |

모터 및 액추에이터 부문은 2025년에 24%의 점유율을 차지했으며, 2026년부터 2035년까지 CAGR 6.1%로 성장할 것으로 예측됩니다. 이 부문의 수요 확대는 차량의 전동화 및 자동화 기능의 사용 증가에 힘입은 바 큽니다. 이러한 기능에는 도어 시스템에 원활하게 통합될 수 있는 소형의 에너지 효율적인 전기기계 부품이 필요합니다.

자동문 모듈 부문은 2025년 87%의 점유율을 차지했습니다. 전자제어식 액세스 시스템 및 윈도우 시스템의 각 차종에 대한 보급 확대가 그 강력한 채택을 주도하고 있습니다. 전기자동차 및 고급 자동차의 지속적인 성장으로 도어 모듈의 전자적 복잡성이 더욱 증가하여 자동화 솔루션에 대한 지속적인 수요를 뒷받침하고 있습니다.

중국 자동차 도어 모듈 시장은 2025년 53%의 점유율을 차지하며 85억 달러 규모에 달할 것으로 예상됩니다. 이 나라의 우위는 높은 자동차 생산량과 양산차부터 프리미엄 승용차(전기자동차 모델 포함)에 이르기까지 다양한 수요에 의해 뒷받침되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률 분석

- 비용 구조

- 각 단계의 부가가치

- 밸류체인에 영향을 미치는 요인

- 디스럽션

- 업계에 대한 영향요인

- 성장 촉진요인

- 증가하는 자동차 생산대수

- 전기자동차 및 고급차 성장

- 모듈러 차량 아키텍처에 초점을 맞춰

- 안전성 및 쾌적성 기능 향상

- 업계의 잠재적 리스크와 과제

- 첨단 시스템 통합 복잡성

- OEM 제조업체에의 비용 압력

- 시장 기회

- 경량 소재 채용

- 스마트 도어 및 액세스 기술

- 신흥 자동차 시장의 확대

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국의 차량 안전 대책

- FMVSS 측면 충돌 기준

- 캘리포니아주 차량 규제 적합성

- 캐나다 차량 가이드라인

- 유럽

- EU 차량 기준

- 유로 NCAP 가이드라인

- 국내 규제에의 적합

- EN 도어 모듈 규격

- 아시아태평양

- 중국의 자동차 규제

- 인도 안전기준

- 일본 모듈 가이드라인

- 한국 규격

- ASEAN 지역 가이드라인

- 라틴아메리카

- 브라질의 자동차 기준

- 아르헨티나의 컴플라이언스

- 멕시코의 규제

- 지역별 안전 가이드라인

- 중동 및 아프리카

- 아랍에미리트(UAE) 차량 기준

- 사우디아라비아의 규제

- 남아프리카공화국의 컴플라이언스

- 지역별 자동차 기준

- 북미

- Porters 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출입

- 비용 내역 분석

- 특허 분석

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 절감 전략

- 생산의 에너지 효율

- 친환경적인 대처

- 탄소발자국에 관한 고려사항

- OEM 채용과 플랫폼 보급률 분석

- 가격 책정, 평균판매가격(ASP) 및 비용 추이

- EV 아키텍처가 도어 모듈 설계에 미치는 영향

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병

- 제휴·협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추정 및 예측 : 구성요소별, 2022-2035

- 래치 및 핸들

- 윈도우 레귤레이터

- 스피커

- 모터 및 액추에이터

- 전기 커넥터 및 배선

- 제어 유닛

- 씰 시스템

- 기타

제6장 시장 추정 및 예측 : 차량별, 2022-2035

- 승용차

- 해치백차

- 세단

- SUV 및 크로스오버차

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제7장 시장 추정 및 예측 : 모듈별, 2022-2035

- 수동 도어 모듈

- 자동문 모듈

제8장 시장 추정 및 예측 : 추진력별, 2022-2035

- 내연기관(ICE)

- BEV(배터리식 전기자동차)

- 하이브리드 자동차

제9장 시장 추정 및 예측 : 도어별, 2022-2035

- 현관 도어 모듈

- 리어 도어 모듈

- 슬라이딩 도어 모듈

- 리프트게이트 도어 모듈

제10장 시장 추정 및 예측 : 판매 채널별, 2022-2035

- OEM

- 애프터마켓

제11장 시장 추정 및 예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 싱가포르

- 태국

- 인도네시아

- 베트남

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

- 튀르키예

제12장 기업 개요

- 세계 플레이어

- Aisin

- Brose

- Continental

- Denso

- Forvia

- Hyundai Mobis

- Magna International

- Robert Bosch

- Valeo

- ZF Friedrichshafen

- 지역 플레이어

- Flex-N-Gate

- Grupo Antolin

- Hi-Lex

- Inteva Products

- PHA Korea

- 신흥 기업/디스럽터

- CIE Automotive

- DaikyoNishikawa

- Dura Automotive Systems

- Hirotec

- Kiekert

The Global Automotive Door Module Market was valued at USD 34 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 55.5 billion by 2035.

Market expansion is driven by steady growth in global vehicle production along with the rising integration of comfort, convenience, and safety technologies in modern vehicles. The accelerating shift toward electric mobility is reshaping door module design, encouraging the adoption of lightweight materials and advanced electronic systems to support efficiency and range optimization. Vehicle manufacturers are increasingly prioritizing modular vehicle architectures to reduce assembly time, streamline production workflows, and lower overall manufacturing costs. Integrating multiple door-related components into a single module allows faster installation, improved quality consistency, and scalability across high-volume vehicle platforms. Growing consumer expectations for enhanced safety and ease of use are further supporting market growth. Features related to access control, occupant protection, and automated functionality are becoming widely adopted across vehicle categories, encouraging higher-volume deployment of integrated door module solutions by original equipment manufacturers.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $34 Billion |

| Forecast Value | $55.5 Billion |

| CAGR | 5.1% |

The motors and actuators segment held a 24% share in 2025 and is projected to grow at a CAGR of 6.1% from 2026 to 2035. Demand growth in this segment is being supported by rising vehicle electrification and increased use of automated functions, which require compact and energy-efficient electromechanical components that can be seamlessly integrated into door systems.

The automated door modules segment accounted for 87% share in 2025. Strong adoption is being driven by the widespread installation of electronically controlled access and window systems across vehicle segments. The continued growth of electric and premium vehicles is further increasing the electronic complexity of door modules, supporting sustained demand for automated solutions.

China Automotive Door Module Market held a 53% share and generated USD 8.5 billion in 2025. The country's dominance is supported by high vehicle production volumes and strong demand across both mass-market and premium passenger vehicles, including electric models.

Key companies operating in the automotive door module market include Magna International, Brose, Hyundai Mobis, Continental, ZF Friedrichshafen, Aisin, Inteva Products, Denso, Robert Bosch, and Hi-Lex. Companies active in the Global Automotive Door Module Market are strengthening their market position through continuous innovation, lightweight design development, and increased electronics integration. Many players are investing in research to improve module efficiency, reduce weight, and support electrified vehicle platforms. Expanding modular product portfolios that can be adapted across multiple vehicle architectures is a key strategy. Manufacturers are also forming long-term supply agreements with automakers to secure consistent demand. Enhancements in manufacturing automation and digital quality control systems are improving cost efficiency and scalability.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Module

- 2.2.5 Propulsion

- 2.2.6 Door

- 2.2.7 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Rising vehicle production volumes

- 3.2.1.3 Growth of electric and premium vehicles

- 3.2.1.4 Focus on modular vehicle architectures

- 3.2.1.5 Increasing safety and comfort features

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system integration complexity

- 3.2.2.2 Cost pressure on OEMs

- 3.2.3 Market opportunities

- 3.2.3.1 Lightweight material adoption

- 3.2.3.2 Smart door and access technologies

- 3.2.3.3 Expansion in emerging automotive markets

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States Vehicle Safety

- 3.4.1.2 FMVSS Side Impact Standards

- 3.4.1.3 California Vehicle Compliance

- 3.4.1.4 Canada Vehicle Guidelines

- 3.4.2 Europe

- 3.4.2.1 EU Vehicle Standards

- 3.4.2.2 Euro NCAP Guidelines

- 3.4.2.3 National Compliance

- 3.4.2.4 EN Door Module Standards

- 3.4.3 Asia Pacific

- 3.4.3.1 China Vehicle Regulations

- 3.4.3.2 India Safety Standards

- 3.4.3.3 Japan Module Guidelines

- 3.4.3.4 South Korea Standards

- 3.4.3.5 ASEAN Regional Guidelines

- 3.4.4 Latin America

- 3.4.4.1 Brazil Vehicle Standards

- 3.4.4.2 Argentina Compliance

- 3.4.4.3 Mexico Regulations

- 3.4.4.4 Regional Safety Guidelines

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Vehicle Standards

- 3.4.5.2 Saudi Arabia Regulations

- 3.4.5.3 South Africa Compliance

- 3.4.5.4 Regional Automotive Standards

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 OEM adoption & platform penetration analysis

- 3.14 Pricing, ASP & Cost Evolution

- 3.15 Impact of EV architectures on door module design

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Latches & handles

- 5.3 Window regulators

- 5.4 Speakers

- 5.5 Motors & actuators

- 5.6 Electrical connectors & wiring

- 5.7 Control units

- 5.8 Sealing systems

- 5.9 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUVs & crossovers

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCVs)

- 6.3.2 Medium Commercial Vehicles (MCVs)

- 6.3.3 Heavy Commercial Vehicles (HCVs)

Chapter 7 Market Estimates & Forecast, By Module, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Manual door modules

- 7.3 Automated door modules

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 ICE

- 8.3 BEVs

- 8.4 Hybrid Vehicles

Chapter 9 Market Estimates & Forecast, By Door, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 Front door modules

- 9.3 Rear door modules

- 9.4 Sliding door modules

- 9.5 Liftgate door modules

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 (USD Mn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.3.8 Netherlands

- 11.3.9 Sweden

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Turkey

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Aisin

- 12.1.2 Brose

- 12.1.3 Continental

- 12.1.4 Denso

- 12.1.5 Forvia

- 12.1.6 Hyundai Mobis

- 12.1.7 Magna International

- 12.1.8 Robert Bosch

- 12.1.9 Valeo

- 12.1.10 ZF Friedrichshafen

- 12.2 Regional Players

- 12.2.1 Flex-N-Gate

- 12.2.2 Grupo Antolin

- 12.2.3 Hi-Lex

- 12.2.4 Inteva Products

- 12.2.5 PHA Korea

- 12.3 Emerging Players/Disruptors

- 12.3.1 CIE Automotive

- 12.3.2 DaikyoNishikawa

- 12.3.3 Dura Automotive Systems

- 12.3.4 Hirotec

- 12.3.5 Kiekert