|

시장보고서

상품코드

1936529

아크릴 에멀전 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Acrylic Emulsion Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

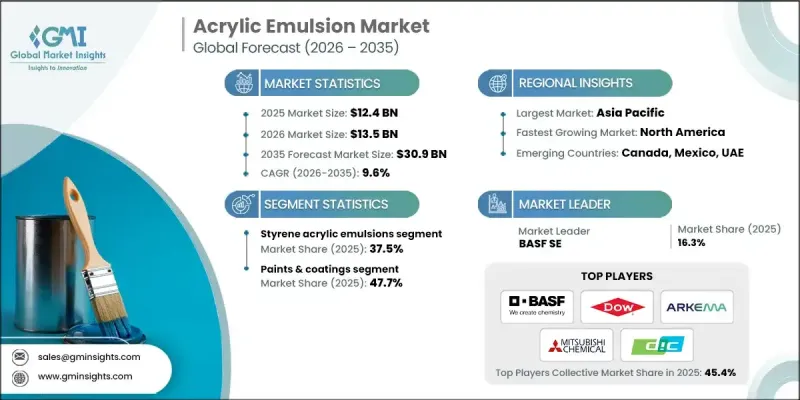

세계의 아크릴 에멀전 시장은 2025년에 124억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 9.6%로 성장할 전망이며, 309억 달러에 이를 것으로 예측됩니다.

아크릴 에멀전은 우수한 내열성, 내화학성 및 다양한 유체에 대한 내성을 특징으로 하는 합성 엘라스토머로, 고성능 밀봉 및 코팅 솔루션을 필요로 하는 산업에서 필수적인 존재입니다. 주요 용도는 자동차, 항공우주, 화학 처리, 석유 및 가스 분야에 달려 있습니다. 시장 역학은 아크릴 단량체 및 기타 화학 원료를 포함한 원재료의 가용성과 가격에 강하게 영향을 받으며 지정학적 이벤트 및 자연 재해로 인한 공급 혼란에 따라 달라질 수 있습니다. 급격한 비용 변동은 제조업체가 안정적인 제품 가격을 유지하는 데 어려움을 겪으며 이익률 압축 및 업무 효율성에 영향을 줄 수 있습니다. 지속가능성의 동향이 업계를 형성하고 있으며, 보다 엄격한 환경 규제 및 환경 친화적인 배합에 대한 소비자 수요 증가에 대응하여 수성 및 저 VOC 아크릴 에멀전이 주목을 받고 있습니다. 보다 환경 친화적이고 안전한 솔루션에 대한 추구는 시장의 장기적인 성장 궤도를 형성할 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 시 가치 | 124억 달러 |

| 예측 금액 | 309억 달러 |

| CAGR | 9.6% |

스티렌 아크릴 에멀전 부문은 2025년에 37.5%의 점유율을 차지했으며, 2035년까지 연평균 복합 성장률(CAGR) 9.4%를 나타낼 것으로 예측됩니다. 이러한 에멀전은 특히 장식용 페인트, 접착제, 실란트 등의 용도 분야에서 성능과 비용 효율성의 균형을 이루는 점에서 높은 평가를 받고 있습니다. 내수성, 내구성, 비용 효율성이 우수한 피복성을 제공하기 위해, 소비자용 제품으로부터 급속하게 도시화가 진행되는 시장까지 폭넓게 적합합니다.

페인트 및 코팅 분야는 2025년에 47.7%의 점유율을 차지했습니다. 아크릴 에멀전은 건축용, 내장용, 외장용, 산업용 코팅에 널리 사용됩니다. 특히 내장용 코팅은 뛰어난 밀착성, 장기간의 내구성, 낮은 VOC 배출량 등의 이점이 있어 주택 환경 및 상업 환경에 적합합니다. 고품질의 페인트 및 코팅에 대한 안정적인 수요가 세계 시장 확대를 지속적으로 견인하고 있습니다.

북미의 아크릴 에멀전 시장은 2026-2035년 연평균 복합 성장률(CAGR) 9.4%로 성장할 것으로 예측됩니다. 이 성장은 순환 경제의 원칙에 따른 폐수 재활용, 폐수 처리 및 지속 가능한 제조의 산업 혁신에 의해 촉진되고 있습니다. 게다가, 퍼스널케어, 청소, 의료 분야에서 환경 배려 제품의 소비자 의식과 선호의 고조가, 보다 엄격한 생태학적 기준을 만족시키는 아크릴 에멀전의 채용을 기업에 촉구하고 있어 시장 발전을 한층 더 추진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 환경에 배려한 저 VOC 페인트에 대한 수요 증가

- 건설 업계의 성장이 아크릴 에멀전계 페인트 수요 견인

- 기능성 가공에 있어서 아크릴 에멀전의 활용에 의한 섬유 산업 성장

- 업계의 잠재적 위험 및 과제

- 환경에 배려한 저 VOC 페인트에 대한 수요 증가

- 건설 업계의 성장이 아크릴 에멀전계 페인트 수요 견인

- 시장 기회

- 포장 및 표시 업계에 있어서 수요 확대

- 혁신적이고 환경에 배려한 배합에 대한 전개

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 유형별

- 향후 시장 동향

- 기술 및 혁신 동향

- 현재 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)

(참고 : 무역 통계는 주요 국가에서만 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국 고려

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 유형별(2022-2035년)

- 순 아크릴 에멀전

- 스티렌 아크릴 에멀전

- 비닐 아크릴 에멀전

- 아크릴 실리콘 에멀전

- 기타

제6장 시장 추계 및 예측 : 용도별(2022-2035년)

- 페인트 및 코팅

- 건축용 페인트

- 내장용 페인트

- 외장용 페인트

- 공업용 페인트

- 자동차용 페인트

- 목공용 페인트

- 금속용 페인트

- 기타

- 특수용도 페인트

- 선박용 페인트

- 보호 페인트

- 기타

- 건축용 페인트

- 접착제 및 실란트

- 감압 접착제

- 건축용 접착제

- 포장용 접착제

- 기타

- 건설 자재

- 시멘트 개질제

- 방수제

- 그라우트 모르타르

- 기타

- 섬유 및 부직포

- 섬유 가공제

- 부직포용 바인더

- 기타

- 종이 및 포장

- 종이용 페인트

- 포장용 페인트

- 기타

- 기타

제7장 시장 추계 및 예측 : 최종 이용 산업별(2022-2035년)

- 건축 및 건설

- 주택 건설

- 상업 건축

- 인프라 개발

- 자동차 및 운송

- 승용차

- 상용차

- 기타

- 산업용

- 금속 가공

- 화학 가공

- 기타

- 소비재

- 가구

- 가전제품

- 기타

- 포장

- 식품 및 음료 포장

- 소비재 포장

- 공업용 포장

- 섬유 및 피혁

- 기타

제8장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- BASF SE

- AkzoNobel NV

- Allnex

- Arkema SA

- Asian Paints

- Celanese Corporation

- DIC Corporation

- Dow Inc.

- Evonik Industries AG

- Lubrizol Corporation

- Mitsubishi Chemical Corporation

- Momentive Performance Materials Inc

- Sika AG

- Synthomer plc

- Wacker Chemie AG

The Global Acrylic Emulsion Market was valued at USD 12.4 billion in 2025 and is estimated to grow at a CAGR of 9.6% to reach USD 30.9 billion by 2035.

Acrylic emulsions are synthetic elastomers known for their excellent resistance to heat, chemicals, and a variety of fluids, making them indispensable in industries that demand high-performance sealing and coating solutions. Key applications span automotive, aerospace, chemical processing, and oil and gas sectors. Market dynamics are strongly influenced by the availability and pricing of raw materials, including acrylic monomers and other chemical inputs, which can fluctuate due to geopolitical events or natural disruptions. Sudden cost volatility can challenge manufacturers in maintaining stable product pricing, potentially compressing profit margins and affecting operational efficiency. Sustainability trends are shaping the industry, with water-based, low-VOC acrylic emulsions gaining prominence in response to stricter environmental regulations and increasing consumer demand for eco-friendly formulations. The drive for greener, safer solutions is expected to shape the market's long-term growth trajectory.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.4 Billion |

| Forecast Value | $30.9 Billion |

| CAGR | 9.6% |

The styrene acrylic emulsions segment accounted for 37.5% share in 2025 and is anticipated to grow at a CAGR of 9.4% through 2035. These emulsions are highly valued for their combination of performance and cost efficiency, particularly in applications such as decorative coatings, adhesives, and sealants. They offer water-resistance, durability, and cost-effective coverage, which make them suitable for both consumer-grade products and rapidly urbanizing markets.

The paints & coatings segment held a 47.7% share in 2025. Acrylic emulsions are extensively used across architectural, interior, exterior, and industrial coatings. Interior coatings, in particular, benefit from strong adhesion, long-lasting durability, and low VOC emissions, making them suitable for residential and commercial environments. The consistent demand for high-quality paints and coatings continues to drive market expansion globally.

North America Acrylic Emulsion Market is projected to grow at a CAGR of 9.4% share from 2026 to 2035. Growth is fueled by industrial innovations in wastewater recycling, effluent treatment, and sustainable manufacturing aligned with circular economy principles. Additionally, increasing consumer awareness and preference for environmentally friendly products across personal care, cleaning, and healthcare sectors are encouraging companies to adopt acrylic emulsions that meet stricter ecological standards, further supporting market development.

Leading players in the Global Acrylic Emulsion Market include BASF SE, AkzoNobel N.V., Allnex, Arkema S.A., Asian Paints, Celanese Corporation, DIC Corporation, Dow Inc., Evonik Industries AG, Lubrizol Corporation, Mitsubishi Chemical Corporation, Momentive Performance Materials Inc., Sika AG, Synthomer plc, and Wacker Chemie AG. Companies in the acrylic emulsion industry are employing diverse strategies to strengthen their market position. They are investing heavily in research and development to create eco-friendly, low-VOC, and water-based formulations that comply with evolving environmental regulations. Strategic partnerships with regional distributors and suppliers help expand supply chains and reach new end-use markets. Continuous product innovation, branding initiatives, and marketing campaigns emphasize sustainability and performance benefits, while targeted pricing strategies and flexible production capacities ensure competitiveness across price-sensitive and premium markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.2.4 End use industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for eco-friendly and low-VOC coatings

- 3.2.1.2 Growth in the construction industry, driving demand for acrylic emulsion-based paints

- 3.2.1.3 Growth in the textile industry, leveraging acrylic emulsions in functional finishes

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Increasing demand for eco-friendly and low-VOC coatings

- 3.2.2.2 Growth in the construction industry, driving demand for acrylic emulsion-based paints

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand in packaging and labeling industries

- 3.2.3.2 Expansion into innovative and eco-friendly formulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pure acrylic emulsions

- 5.3 Styrene acrylic emulsions

- 5.4 Vinyl acrylic emulsions

- 5.5 Acrylic silicone emulsions

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Paints & coatings

- 6.2.1 Architectural coatings

- 6.2.1.1 Interior coatings

- 6.2.1.2 Exterior coatings

- 6.2.1.3 Industrial coatings

- 6.2.2 Automotive coatings

- 6.2.2.1 Wood coatings

- 6.2.2.2 Metal coatings

- 6.2.2.3 Others

- 6.2.3 Special purpose coatings

- 6.2.3.1 Marine coatings

- 6.2.3.2 Protective coatings

- 6.2.3.3 Others

- 6.2.1 Architectural coatings

- 6.3 Adhesives & sealants

- 6.3.1 Pressure-sensitive adhesives

- 6.3.2 Construction adhesives

- 6.3.3 Packaging adhesives

- 6.3.4 Others

- 6.4 Construction materials

- 6.4.1 Cement modifiers

- 6.4.2 Waterproofing compounds

- 6.4.3 Grouts and mortars

- 6.4.4 Others

- 6.5 Textiles & nonwovens

- 6.5.1 Textile finishes

- 6.5.2 Nonwoven binders

- 6.5.3 Others

- 6.6 Paper & packaging

- 6.6.1 Paper coatings

- 6.6.2 Packaging coatings

- 6.6.3 Others

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Building & construction

- 7.2.1 Residential construction

- 7.2.2 Commercial construction

- 7.2.3 Infrastructure development

- 7.3 Automotive & transportation

- 7.3.1 Passenger vehicles

- 7.3.2 Commercial vehicles

- 7.3.3 Others

- 7.4 Industrial

- 7.4.1 Metal processing

- 7.4.2 Chemical processing

- 7.4.3 Others

- 7.5 Consumer goods

- 7.5.1 Furniture

- 7.5.2 Appliances

- 7.5.3 Others

- 7.6 Packaging

- 7.6.1 Food & beverage packaging

- 7.6.2 Consumer goods packaging

- 7.6.3 Industrial packaging

- 7.7 Textile & leather

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 AkzoNobel N.V

- 9.3 Allnex

- 9.4 Arkema S.A

- 9.5 Asian Paints

- 9.6 Celanese Corporation

- 9.7 DIC Corporation

- 9.8 Dow Inc.

- 9.9 Evonik Industries AG

- 9.10 Lubrizol Corporation

- 9.11 Mitsubishi Chemical Corporation

- 9.12 Momentive Performance Materials Inc

- 9.13 Sika AG

- 9.14 Synthomer plc

- 9.15 Wacker Chemie AG