|

시장보고서

상품코드

1936532

희귀질환 치료 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Rare Disease Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

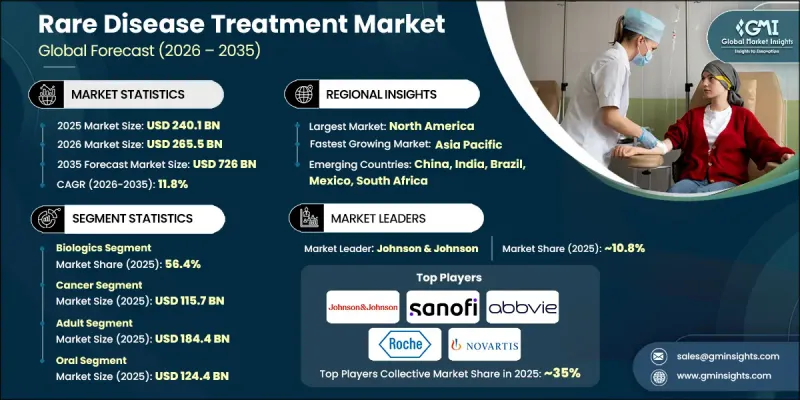

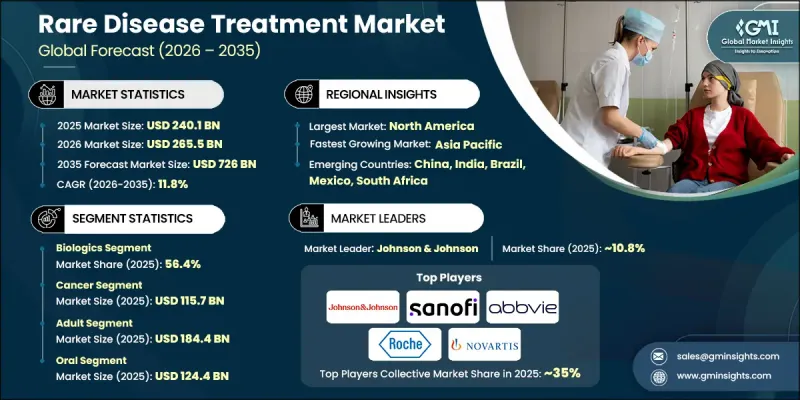

세계의 희귀질환 치료 시장은 2025년에 2,401억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 11.8%로 성장할 전망이며, 7,260억 달러에 달할 것으로 예측되고 있습니다.

이 시장은 제한된 환자 수와 미충족 요구가 뚜렷한 질병을 대상으로 한 치료법의 개발과 상업화에 중점을 둡니다. 희귀질환 치료는 전문적인 규제 경로에 따라 개발된 광범위한 고급 치료법 및 유리한 정책 인센티브 및 상환 제도에 의해 지원됩니다. 정밀의료의 지속적인 진전 및 혁신을 촉진하는 규제 지원 프로그램이 시장 확대를 가속화하고 있습니다. 업계는 증상 관리뿐만 아니라 근본적인 생물학적 메커니즘을 표적으로 하는 질병 변형 및 근치 접근법에 점점 더 주력하고 있습니다. 분자 과학과 치료 공학의 혁신은 치료 성과 및 장기적인 질병 관리를 변화시키고 있습니다. 과학적 진보, 환자 중심 개발 전략 및 지원 규제 환경의 융합은 의약품 및 헬스케어 시장 전반에 걸쳐 세계 수요와 투자를 지속적으로 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 시 가치 | 2,401억 달러 |

| 예측 금액 | 7,260억 달러 |

| CAGR | 11.8% |

시장에서의 현저한 변화로서, 분자 표적 요법 및 유전자 정보에 기초한 치료로의 전환을 포함합니다. 첨단 치료 접근법은 지속적인 임상 효과 및 질병 진행을 변화시킬 가능성을 제공하기 위해 주목을 받고 있습니다. 유전체 연구와 정밀 진단의 진보에 힘입어 맞춤형 치료의 개발이 점점 보급되고 있습니다. 이러한 맞춤형 요법은 치료 효과를 높이는 동시에 부작용 위험을 줄이고 희귀질환 관리 전반에 걸친 개인화 관리 모델로의 전환을 촉진합니다.

바이오로직 분야는 2025년에 56.4%의 점유율을 차지하였고, 2026-2035년 CAGR 11.7%로 성장할 것으로 예측됩니다. 이러한 치료법은 특이성과 강력한 치료 효과로 인해 복잡한 생물학적 상태를 다루는 데 중심적인 역할을 합니다. 안전성 프로파일을 개선한 표적 개입을 실현하는 능력이 광범위한 채용을 추진하고 있습니다. 환자 수준 데이터를 기반으로 한 맞춤화를 포함한 생물학적 제형 개발의 지속적인 혁신은 부문의 지속적인 성장을 더욱 지원하고 정밀의료 중심의 헬스케어로 광범위한 전환과 일치합니다.

성인 환자를 위한 시장 규모는 2025년 1,844억 달러에 이르렀으며, 2035년까지 연평균 복합 성장률(CAGR) 11.7%로 확대될 것으로 전망됩니다. 질병의 진행 패턴 및 진단 시기의 특성으로 인해 성인은 세계 최대의 치료 대상층을 차지합니다. 소아 시장은 비교적 소규모이지만 진단 기술의 진보와 조기 발견의 진전에 의해 성장이 가속화되고 있으며, 양 시장층에 대한 지속적인 투자가 치료 환경의 진화를 보장하고 있습니다.

북미의 희귀 질환 치료 시장은 2025년에 41.1%의 점유율을 차지했으며, 첨단 헬스케어 시스템, 강력한 규제 인센티브, 혁신적인 치료법의 신속한 도입으로 주도적 지위를 유지하고 있습니다. 이 지역은 광범위한 조사 인프라, 정밀의료의 조기 통합 및 생명 공학 개발에 많은 투자를 혜택을 받고 있습니다. 지원 상환 제도와 적극적인 환자 지원 활동은 또한 지역 전체의 지속적인 수요와 시장 성숙도에 기여합니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 희귀질환의 유병률 증가

- 정밀의료 및 생명 공학의 진전

- 지원적인 규제 프레임워크 및 인센티브

- 높아지는 인지도 및 조기 진단률

- 업계의 잠재적 위험 및 과제

- 높은 비용 및 제한된 가격

- 환자수가 적고 임상시험의 복잡성

- 시장 기회

- 헬스케어 인프라가 개선되고 있는 신흥 시장에 대한 진출

- 협업 및 디지털 건강 통합

- 성장 촉진요인

- 성장 가능성 분석

- 기술 동향

- 현재 기술 동향

- 신흥 기술

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 파이프라인 분석

- 장래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력 관계

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 약제 유형별(2022-2035년)

- 생물학적 제형

- 비생물학적 제형

제6장 시장 추계 및 예측 : 치료 영역별(2022-2035년)

- 암

- 혈액 관련 질환

- 중추신경계

- 호흡기 질환

- 근골격계 질환

- 순환기 질환

- 기타 치료 영역

제7장 시장 추계 및 예측 : 환자별(2022-2035년)

- 성인용

- 소아용

제8장 시장 추계 및 예측 : 투여 경로별(2022-2035년)

- 경구

- 주사제

- 기타 투여 경로

제9장 시장 추계 및 예측 : 최종 용도별(2022-2035년)

- 병원 및 진료소

- 재택 치료 환경

- 기타 최종 사용자

제10장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- AbbVie

- Alexion Pharmaceuticals

- Amgen

- AstraZeneca

- Baxter International

- Bayer

- Bristol-Myers Squibb

- Eli Lilly and Company

- F. Hoffmann La Roche

- GlaxoSmithKline

- Johnson & Johnson

- Merck & Co.

- Novartis

- Novo Nordisk

- Pfizer

- Sanofi

- Takeda Pharmaceutical

- Vertex Pharmaceutical

The Global Rare Disease Treatment Market was valued at USD 240.1 billion in 2025 and is estimated to grow at a CAGR of 11.8% to reach USD 726 billion by 2035.

The market focuses on the development and commercialization of therapies designed to address conditions affecting limited patient populations but characterized by substantial unmet clinical needs. Rare disease treatments span a broad range of advanced therapeutic modalities developed under specialized regulatory pathways, supported by favorable policy incentives and reimbursement structures. Continued progress in precision medicine, along with regulatory support programs that encourage innovation, continues to accelerate market expansion. The industry is increasingly centered on disease-modifying and curative approaches that target underlying biological mechanisms rather than symptom management alone. Innovations in molecular science and therapeutic engineering are transforming treatment outcomes and long-term disease control. The convergence of scientific advancements, patient-focused development strategies, and supportive regulatory ecosystems continues to strengthen global demand and investment across pharmaceutical and healthcare markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $240.1 Billion |

| Forecast Value | $726 Billion |

| CAGR | 11.8% |

A notable transformation within the market is the shift toward molecularly targeted and genetically informed therapies. Advanced therapeutic approaches are gaining traction as they offer durable clinical benefits and the potential to alter disease progression. Personalized treatment development has become increasingly prevalent, supported by advancements in genomic research and diagnostic precision. These tailored therapies enhance treatment effectiveness while reducing the risk of adverse reactions, reinforcing the transition toward individualized care models across rare disease management.

The biologics segment held 56.4% share in 2025 and is projected to grow at a CAGR of 11.7% during 2026-2035. These therapies play a central role in addressing complex biological conditions due to their specificity and strong therapeutic performance. Their ability to deliver targeted intervention with improved safety profiles has driven widespread adoption. Continued innovation in biologic development, including customization based on patient-level data, further supports sustained segment growth and aligns with the broader shift toward precision-driven healthcare.

The adult patient population generated reached USD 184.4 billion in 2025 and is expected to grow at a CAGR of 11.7% throughout 2035. Adults represent the largest treatment group globally due to disease progression patterns and diagnosis timelines. While the pediatric segment remains smaller in comparison, it continues to experience accelerated growth, supported by expanded diagnostic capabilities and earlier disease identification. The evolving treatment landscape ensures continued investment across both population segments.

North America Rare Disease Treatment Market accounted for 41.1% share in 2025, maintaining its leadership position due to advanced healthcare systems, strong regulatory incentives, and rapid adoption of innovative therapies. The region benefits from extensive research infrastructure, early integration of precision medicine, and substantial investment in biotechnology development. Supportive reimbursement structures and active patient advocacy further contribute to sustained demand and market maturity across the region.

Key companies operating in the Global Rare Disease Treatment Market include Novartis, Pfizer, Sanofi, Vertex Pharmaceutical, Takeda Pharmaceutical, Bristol-Myers Squibb, AstraZeneca, Merck & Co., AbbVie, Bayer, Novo Nordisk, GlaxoSmithKline, Eli Lilly and Company, Johnson & Johnson, Amgen, Alexion Pharmaceuticals, Baxter International, and F. Hoffmann La Roche. These organizations maintain strong positions through innovation-driven pipelines and long-term investment strategies. To reinforce their foothold, companies in the rare disease treatment sector are prioritizing sustained investment in research and development focused on high-value, disease-modifying therapies. Strategic collaborations, licensing agreements, and acquisitions are widely used to expand therapeutic pipelines and accelerate commercialization timelines. Firms are also leveraging precision medicine platforms to develop targeted treatments that address specific patient subgroups.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug type trends

- 2.2.3 Therapeutic area trends

- 2.2.4 Patient trends

- 2.2.5 Route of administration trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of rare diseases

- 3.2.1.2 Advancements in precision medicine and biotechnology

- 3.2.1.3 Supportive regulatory frameworks and incentives

- 3.2.1.4 Growing awareness and early diagnosis rates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost and limited affordability

- 3.2.2.2 Small patient populations and clinical trial complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with improving healthcare infrastructure

- 3.2.3.2 Collaborations and digital health integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Biologics

- 5.3 Non-biologics

Chapter 6 Market Estimates and Forecast, By Therapeutic Area, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Cancer

- 6.3 Blood-related disorders

- 6.4 Central nervous system

- 6.5 Respiratory disorders

- 6.6 Musculoskeletal disorders

- 6.7 Cardiovascular disorders

- 6.8 Other therapeutic areas

Chapter 7 Market Estimates and Forecast, By Patient, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Adult

- 7.3 Pediatric

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Oral

- 8.3 Injectable

- 8.4 Other routes of administration

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and clinics

- 9.3 Homecare settings

- 9.4 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AbbVie

- 11.2 Alexion Pharmaceuticals

- 11.3 Amgen

- 11.4 AstraZeneca

- 11.5 Baxter International

- 11.6 Bayer

- 11.7 Bristol-Myers Squibb

- 11.8 Eli Lilly and Company

- 11.9 F. Hoffmann La Roche

- 11.10 GlaxoSmithKline

- 11.11 Johnson & Johnson

- 11.12 Merck & Co.

- 11.13 Novartis

- 11.14 Novo Nordisk

- 11.15 Pfizer

- 11.16 Sanofi

- 11.17 Takeda Pharmaceutical

- 11.18 Vertex Pharmaceutical