|

시장보고서

상품코드

1936546

유방 초음파 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Breast Ultrasound Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

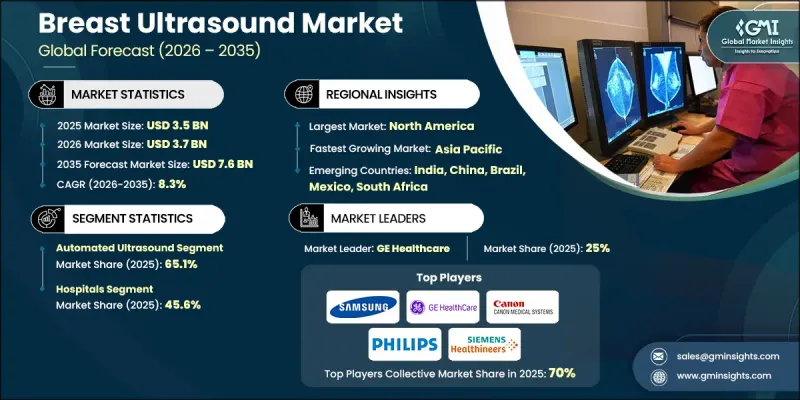

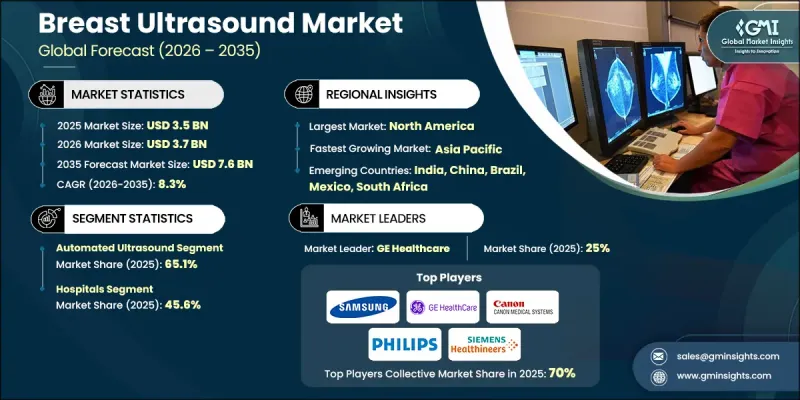

세계의 유방 초음파 시장은 2025년에 35억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 8.3%로 성장할 전망이며, 76억 달러에 이를 것으로 예측됩니다.

시장 성장은 세계 유방암 부담 증가, 검진 의식 증가, 공중 위생 시책 지원, 초음파 영상 기술의 지속적인 혁신에 의해 지원되고 있습니다. 세계 유방암 발생률의 상승은 조기 발견 및 정확한 진단 도구의 필요성을 강화하고 유방 초음파 시스템 수요를 직접적으로 증가시키고 있습니다. 이러한 시스템은 방사선 피폭이 없는 비침습적 영상 진단을 가능하게 하며, 반복 검진이나 경과 관찰에 적합하기 때문에 널리 채용되고 있습니다. 계발 활동 확대 및 의료 정책 지원으로 정기 검진 참여율이 향상되고 시장 수요가 더욱 강화되고 있습니다. 유방의 건강에 대한 이해의 심화와 진단 서비스에의 액세스 확대가 함께, 의료 현장 전체에서의 도입을 추진하고 있습니다. 이미지의 선명도, 자동화 및 진단 정확도의 기술적 진보는 임상 현장의 신뢰성을 높이고 유방 초음파의 표준 진단 워크플로우에 대한 광범위한 통합을 지원합니다. 의료 시스템이 조기 진단과 환자 안전을 더욱 중시하는 동안 유방 초음파는 장기적인 시장 성장을 지원하는 중요한 이미징 솔루션입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 시 가치 | 35억 달러 |

| 예측 금액 | 76억 달러 |

| CAGR | 8.3% |

자동화 초음파 부문은 2025년에 23억 달러 시장 규모를 창출해, 65.1%의 점유율을 차지했습니다. 자동화된 유방 초음파 기술은 표준화된 스캔을 통해 종합적인 이미지를 제공하여 일관된 화질 및 유방 조직의 상세한 시각화를 가능하게 합니다. 운영자 의존도 감소 및 진단 신뢰성의 향상은 임상 현장에서 자동화 시스템의 도입을 강력하게 뒷받침하고 있습니다.

병원 부문은 2024년에 45.6%의 점유율을 차지했으며, 유방 초음파의 주요 의료 현장으로 계속되고 있습니다. 이러한 시설은 첨단 영상 진단 장비와 통합된 진단 서비스에 대한 액세스를 제공하여 단일 의료 환경 내에서 정확한 감지, 평가 및 경과 관찰을 지원합니다.

북미의 유방 초음파 시장은 2025년 34%의 점유율을 차지했습니다. 질병 유병률 증가, 스크리닝 검사의 보급 확대, 지속적인 기술 통합이 지역 전체 수요를 견인하고 있습니다. 의료 제공업체는 진단의 확신도 향상과 판독의 편차 감소를 위해 고급 초음파 솔루션에 대한 의존도를 높이고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계의 유방암 이환율 증가

- 유방 초음파 진단 장치에서 기술 진보의 진전

- 유방암에 대한 인식 증가 및 유리한 정부 시책

- 미국에서 유방 초음파의 보험 상환률 향상

- 업계의 잠재적 위험 및 과제

- 자동화 유방 초음파 장치의 고비용

- 개발도상 지역 및 미개발 지역에서 숙련 또는 훈련을 받은 인재 부족

- 시장 기회

- 원격 의료와의 제휴

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술적 진보

- 현재 기술 동향

- 신흥 기술

- 가격 분석(2024년)

- 장래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 공동 사업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 유형별(2022-2035년)

- 기존 초음파

- 자동 초음파 장치

제6장 시장 추계 및 예측 : 최종 용도별(2022-2035년)

- 병원

- 진단 실험실

- 기타 최종 사용자

제7장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제8장 기업 프로파일

- CapeRay

- Delphinus Medical Technologies, Inc.

- GE Healthcare

- Koninklijke Philips NV

- Siemens Healthineers AG

- Canon Medical Systems Corporation

- Fukuda Denshi

- Hologic, Inc.

- Seno Medical Instruments Inc.

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- Samsung Electronics Co. Ltd.

- FujiFilm Holdings Corporation

The Global Breast Ultrasound Market was valued at USD 3.5 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 7.6 billion by 2035.

Market growth is supported by the rising global burden of breast cancer, increasing screening awareness, supportive public health initiatives, and continuous innovation in ultrasound imaging technologies. The growing incidence of breast cancer worldwide has intensified the need for early-stage detection and accurate diagnostic tools, directly increasing demand for breast ultrasound systems. These systems are widely adopted because they enable non-invasive imaging without radiation exposure, making them suitable for repeated screenings and follow-up evaluations. Expanded awareness programs and favorable healthcare policies have encouraged higher participation in routine screening, further strengthening market demand. Improved understanding of breast health, combined with broader access to diagnostic services, continues to drive adoption across healthcare settings. Technological improvements in image clarity, automation, and diagnostic accuracy are enhancing clinical confidence and supporting wider integration of breast ultrasound into standard diagnostic workflows. As healthcare systems place greater emphasis on early diagnosis and patient safety, breast ultrasound remains a critical imaging solution supporting long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.5 Billion |

| Forecast Value | $7.6 Billion |

| CAGR | 8.3% |

The automated ultrasound segment generated USD 2.3 billion in 2025 and accounted for a share of 65.1%. Automated breast ultrasound technology provides comprehensive imaging through standardized scanning, enabling consistent image quality and detailed visualization of breast tissue. Reduced operator dependency and enhanced diagnostic reliability continue to support strong adoption of automated systems in clinical practice.

The hospitals segment accounted for 45.6% share in 2024 and remains the leading care setting for breast ultrasound procedures. These facilities offer access to advanced imaging equipment and integrated diagnostic services, supporting accurate detection, evaluation, and follow-up within a single care environment.

North America Breast Ultrasound Market represented 34% share in 2025. Rising disease prevalence, strong screening adoption, and continuous technology integration are driving demand across the region. Healthcare providers increasingly rely on advanced ultrasound solutions to improve diagnostic confidence and reduce interpretation variability.

Key companies operating in the Global Breast Ultrasound Market include GE Healthcare, Siemens Healthineers AG, Koninklijke Philips N.V., Canon Medical Systems Corporation, Samsung Electronics Co. Ltd., Hologic, Inc., Fujifilm Holdings Corporation, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Delphinus Medical Technologies, Inc., CapeRay, Seno Medical Instruments Inc., Fukuda Denshi, and others. Companies in the breast ultrasound market strengthen their competitive position by investing in advanced imaging innovation, automation, and diagnostic accuracy. Many players focus on developing systems with improved resolution, workflow efficiency, and reduced operator variability. Strategic partnerships with healthcare providers and research institutions support clinical validation and market expansion. Firms also emphasize integration with digital health platforms and AI-assisted diagnostics to enhance detection capabilities. Expanding global distribution networks and offering comprehensive service and training programs help improve adoption.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of breast cancer worldwide

- 3.2.1.2 Rising technological advancements in breast ultrasound systems

- 3.2.1.3 Rising awareness and favourable government initiatives regarding breast cancer

- 3.2.1.4 Increased reimbursement for breast ultrasound in the U.S.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of the automated breast ultrasound system devices

- 3.2.2.2 Lack of skilled or trained personnel in the developing and underdeveloped region

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with Telemedicine

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2024

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Conventional ultrasound

- 5.3 Automated ultrasound

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Diagnostic Laboratories

- 6.4 Other end users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 CapeRay

- 8.2 Delphinus Medical Technologies, Inc.

- 8.3 GE Healthcare

- 8.4 Koninklijke Philips N.V.

- 8.5 Siemens Healthineers AG

- 8.6 Canon Medical Systems Corporation

- 8.7 Fukuda Denshi

- 8.8 Hologic, Inc.

- 8.9 Seno Medical Instruments Inc.

- 8.10 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- 8.11 Samsung Electronics Co. Ltd.

- 8.12 FujiFilm Holdings Corporation