|

시장보고서

상품코드

1936549

바이오연료 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Biofuel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

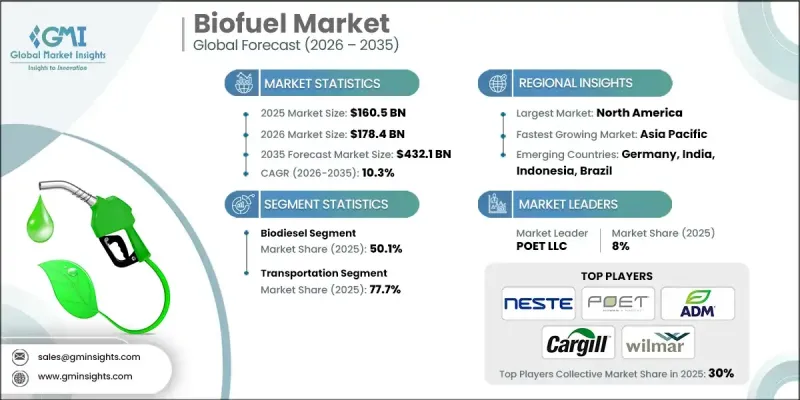

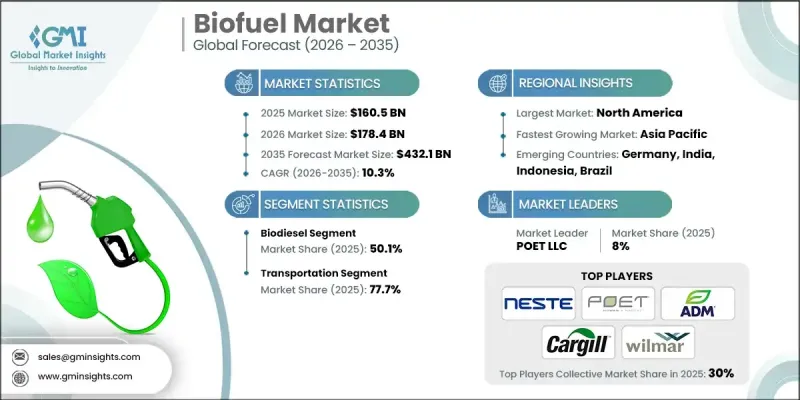

세계의 바이오연료 시장은 2025년에 1,605억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 10.3%로 성장할 전망이며, 4,321억 달러에 이를 것으로 예측됩니다.

운송 부문의 탈탄소화를 목적으로 한 지속적인 규제 요건이 세계적으로 예측 가능하고 지속적인 바이오연료 수요를 견인하고 있습니다. 각국 정부는 연료 정책에 라이프사이클 탄소 강도의 삭감을 통합하는 경향을 강화하고 있으며, 저탄소 연료를 공급하는 생산자가 거래 가능한 크레딧을 획득할 수 있는 컴플라이언스 시장을 창출하고 있습니다. 이러한 규정은 검증 및 추적성을 표준화하고 구매자의 위험을 줄이며 판매 계약을 강화합니다. 그 결과 도로, 항공 및 선박의 각 부문에서 에탄올, 바이오디젤, 재생가능 디젤(HVO), 바이오가스 및 CBG, 지속가능한 항공연료(SAF) 수요가 촉진되고 있습니다. 컴플라이언스 타임라인과 면제 메커니즘을 포함한 적극적인 정책 관리는 시장의 확실성을 유지하고 일관된 공급량을 사업 계획 및 자본 계획에 의존하는 농가, 정제업자, 연료 블렌더에 이익을 줍니다. 저탄소연료기준(LCFS) 등의 프로그램은 계속 확대되고 있으며, 폐기물과 잔사를 원료로 하는 바이오연료를 장려함과 동시에 인프라와 교통기관을 위한 신용 기회를 확대하여 사용후 식용유, 동물성 지방, 매립지 가스, 유기 폐기물 스트림으로부터 대규모 생산을 지원하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 시 가치 | 1,605억 달러 |

| 예측 금액 | 4,321억 달러 |

| CAGR | 10.3% |

바이오디젤 부문은 2025년에 50.1%의 점유율을 차지하였고, 2035년까지 연평균 복합 성장률(CAGR) 10.5%를 나타낼 것으로 예측됩니다. 생산자는 라이프사이클 배출량 감소, LCFS(저탄소 연료 기준)와 같은 프레임워크의 CI 점수 향상, 국내외 컴플라이언스 시장에서 보다 높은 경제적 리턴 획득을 목표로 탄소 캡처 설비 개수에 투자하고 있습니다. 바이오디젤은 엄격한 탄소 강도 정책 및 규제 인센티브 증가의 혜택을 받고 있으며, 폐기물 및 잔류물 원료 유래 연료의 채택을 촉진하고 있습니다.

운송 부문은 2025년에 77.7%의 점유율을 차지하였고, 2035년까지 연평균 복합 성장률(CAGR) 9.5%를 나타낼 것으로 예측됩니다. 규제 의무, 컴플라이언스 주도 신용 시장, 드롭 인형 재생 가능 연료의 가용성으로 인해 운송 부문은 가장 안정적이고 가장 큰 수요원으로 계속되고 있습니다. 정부는 이 분야에서 바이오연료를 우선적으로 채용하고 있습니다. 특히 대형 트럭, 지자체 차량, 장거리 물류에 있어서, 차량이나 인프라의 대폭적인 개조를 수반하지 않고 즉시의 배출 감축을 실현할 수 있기 때문입니다. 에너지 안보에 대한 우려 및 수입 화석 연료에 대한 의존도 저감의 필요성은 선진국 및 신흥국 쌍방에서의 바이오연료 도입을 더욱 뒷받침하고 있습니다.

미국의 바이오연료 시장은 2025년 546억 달러를 창출해, 93%의 점유율을 차지했습니다. 이 주도적 지위는 성숙한 규제 환경, 정비된 원료 공급망, 저탄소 연료를 우월한 컴플라이언스 제도에 의해 지원되고 있습니다. 에너지 안보의 우선 과제, 화석 연료 가격의 변동성, 화물, 항공 및 해운 업계의 탈탄소화에 대한 기업 헌신이 정치적 지원을 강화하고, 이들 전체가 바이오연료 소비의 가속에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 새로운 기회 및 동향

- 디지털화 및 IoT 통합

- 신흥 시장 진출

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 전략적 노력

- 경쟁 벤치마킹

- 전략적 대시보드

- 혁신 및 기술 동향

제5장 시장 규모 및 예측 : 연료별(2022-2035년)

- 바이오디젤

- 에탄올

- 기타

제6장 시장 규모 및 예측 : 원료별(2022-2035년)

- 거친 곡물

- 설탕 작물

- 식물성 기름

- 기타

제7장 시장 규모 및 예측 : 용도별(2022-2035년)

- 교통기관

- 항공분야

- 기타

제8장 시장 규모 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 스페인

- 영국

- 이탈리아

- 아시아태평양

- 중국

- 인도

- 인도네시아

- 호주

- 한국

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 라틴아메리카

- 브라질

- 아르헨티나

제9장 기업 프로파일

- ADM

- Borregaard

- BTG Bioliquids

- Cargill

- Chevron Corporation

- Clariant

- COFCO

- CropEnergies

- FutureFuel

- Munzer Bioindustrie

- My Eco Energy

- Neste Corporation

- POET

- Praj Industries

- The Andersons

- TotalEnergies

- UPM

- Verbio

- Wilmar International

- Zilor

The Global Biofuel Market was valued at USD 160.5 billion in 2025 and is estimated to grow at a CAGR of 10.3% to reach USD 432.1 billion by 2035.

Continuous regulatory mandates aimed at decarbonizing transportation are driving predictable and durable demand for biofuels worldwide. Governments are increasingly embedding lifecycle carbon intensity reductions into fuel policies, creating compliance markets where producers can earn tradable credits for supplying lower-carbon fuels. These regulations standardize verification and traceability, reducing buyer risk and strengthening offtake agreements, which in turn boosts demand for ethanol, biodiesel, renewable diesel (HVO), biogas/CBG, and sustainable aviation fuels across road, aviation, and marine segments. Active policy management, including compliance timelines and waiver mechanisms, maintains market certainty, benefiting farmers, refiners, and fuel blenders who rely on consistent volumes for operational and capital planning. Programs such as Low Carbon Fuel Standards (LCFS) are expanding, incentivizing waste- and residue-based biofuels and broadening credit opportunities for infrastructure and transit, supporting large-scale production from used cooking oil, animal fats, landfill gas, and organic waste streams.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $160.5 Billion |

| Forecast Value | $432.1 billion |

| CAGR | 10.3% |

The biodiesel segment accounted for 50.1% share in 2025 and is projected to grow at a CAGR of 10.5% through 2035. Producers are investing in carbon capture retrofits to reduce lifecycle emissions, improve CI scores under LCFS-like frameworks, and qualify for higher economic returns in both domestic and export compliance markets. Biodiesel continues to benefit from stringent carbon-intensity policies and increasing regulatory incentives, encouraging fleets to adopt fuels derived from waste and residue feedstocks.

The transportation sector represented 77.7% share in 2025 and is expected to grow at a CAGR of 9.5% by 2035. Transport remains the most stable and largest demand center due to regulatory mandates, compliance-driven credit markets, and availability of drop-in renewable fuels. Governments prioritize biofuels in this sector because they achieve immediate emissions reductions without major vehicle or infrastructure modifications, especially in heavy-duty trucking, municipal fleets, and long-haul logistics. Energy security concerns and the need to reduce dependence on imported fossil fuels further reinforce biofuel adoption in developed and emerging economies.

U.S. Biofuel Market held 93% share, generating USD 54.6 billion in 2025. Leadership is driven by a mature regulatory ecosystem, well-developed feedstock supply chains, and compliance mechanisms that reward lower-carbon fuels. Political support is reinforced by energy security priorities, fossil fuel price volatility, and corporate decarbonization commitments from freight, aviation, and maritime industries, which collectively accelerate biofuel consumption.

Key players in the Global Biofuel Market include ADM, Borregaard, BTG Bioliquids, Cargill, Chevron Corporation, Clariant, COFCO, CropEnergies, FutureFuel, Munzer Bioindustrie, My Eco Energy, Neste Corporation, POET, Praj Industries, The Andersons, TotalEnergies, UPM, Verbio, Wilmar International, and Zilor. Companies in the biofuel industry are deploying several strategies to strengthen their market presence. They are investing in R&D to develop low-carbon and waste-based feedstocks, improving efficiency and compliance with regulatory frameworks. Strategic partnerships with local feedstock suppliers and transportation firms expand supply chains and market reach. Businesses are also investing in advanced production infrastructure, including carbon capture retrofits and scale-up of renewable diesel and sustainable aviation fuel capacity. Market penetration is further reinforced through government engagement, lobbying for favorable policies, and participation in compliance credit programs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Fuel trends

- 2.1.3 Feedstock trends

- 2.1.4 Application trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million, Mtoe)

- 5.1 Key trends

- 5.2 Biodiesel

- 5.3 Ethanol

- 5.4 Others

Chapter 6 Market Size and Forecast, By Feedstock, 2022 - 2035 (USD Million, Mtoe)

- 6.1 Key trends

- 6.2 Coarse grain

- 6.3 Sugar crop

- 6.4 Vegetable oil

- 6.5 Others

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million, Mtoe)

- 7.1 Key trends

- 7.2 Transportation

- 7.3 Aviation

- 7.4 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million, Mtoe)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 Spain

- 8.3.4 UK

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Indonesia

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ADM

- 9.2 Borregaard

- 9.3 BTG Bioliquids

- 9.4 Cargill

- 9.5 Chevron Corporation

- 9.6 Clariant

- 9.7 COFCO

- 9.8 CropEnergies

- 9.9 FutureFuel

- 9.10 Munzer Bioindustrie

- 9.11 My Eco Energy

- 9.12 Neste Corporation

- 9.13 POET

- 9.14 Praj Industries

- 9.15 The Andersons

- 9.16 TotalEnergies

- 9.17 UPM

- 9.18 Verbio

- 9.19 Wilmar International

- 9.20 Zilor