|

시장보고서

상품코드

1936559

중공 유리 미소구 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Hollow Glass Microspheres Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

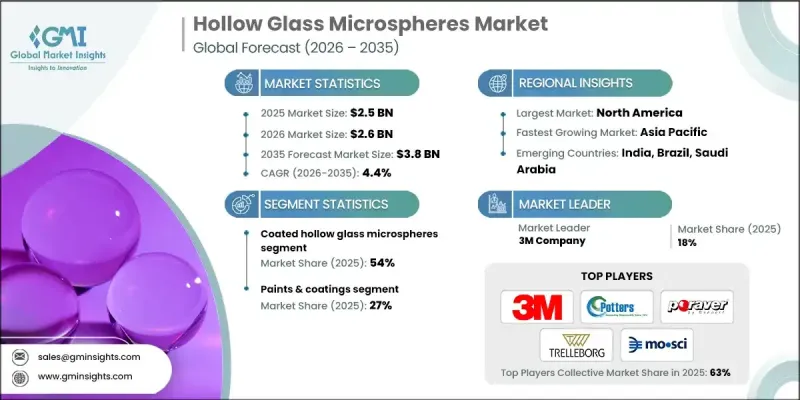

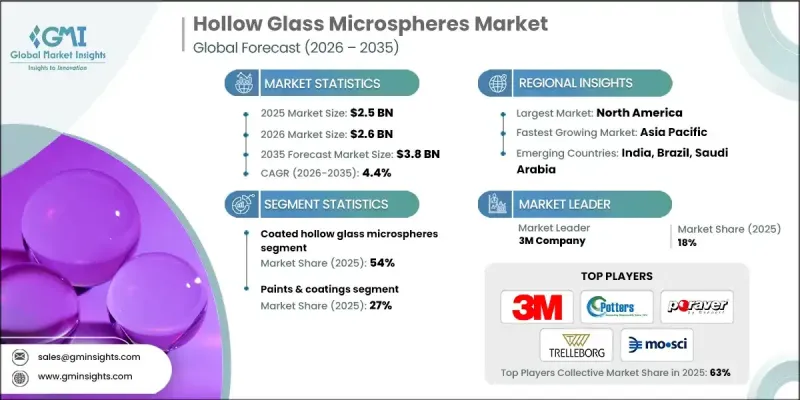

세계의 중공 유리 미소구 시장은 2025년에 25억 달러로 평가되었으며, 2035년까지 CAGR 4.4%로 성장하여 38억 달러에 달할 것으로 예측됩니다.

시장 성장은 자동차 및 산업 분야의 연비 효율과 배출가스 규제 강화에 따른 압력 증가에 의해 주도되고 있습니다. 중공 유리 마이크로스피어는 제품의 경량화에 기여하고, 차량의 연비 효율 향상 및 기타 용도의 에너지 절약을 촉진합니다. 북미와 유럽에서는 엄격한 CO2 규제와 넷제로(Net Zero) 이니셔티브로 인해 자동차 제조업체와 소재 공급업체들이 기존의 광물성 충전재를 경량화 된 마이크로 스피어로 대체하는 움직임이 가속화되고 있습니다. 건설 및 인프라 분야도 크게 기여하고 있으며, 건축물의 에너지 효율 규제 강화에 따라 단열 패널, 코팅, 실란트 등에 마이크로스피어 채용이 진행되고 있습니다. 이를 통해 무게 증가 없이 열 조절 성능이 향상됩니다. 페인트, 코팅, 폴리머 업계에서는 VOC 함량 감소, 방음성 향상, 경량화 및 고성능 제품 실현을 목적으로 마이크로스피어 채용이 확대되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 25억 달러 |

| 예측 금액 | 38억 달러 |

| CAGR | 4.4% |

코팅된 중공 유리 마이크로스피어 부문은 2025년에 54%의 점유율을 차지했으며, 2035년까지 연평균 4.6%의 성장률을 기록할 것으로 예상됩니다. 제조업체들은 단순히 코팅된 마이크로스피어를 공급하는 것뿐만 아니라 에폭시, 폴리우레탄, 폴리올레핀, 특수 코팅 응용 분야와 같은 최종 사용 시스템에 대한 맞춤형 솔루션을 제공하는 방향으로 전환하고 있습니다. 은 및 니켈 코팅은 주로 전도성 및 EMI 차폐 기능을 목적으로하며, 알루미늄 및 이산화 티타늄 코팅은 반사율과 광학 장벽 특성을 향상시킵니다. 맞춤형 코팅을 통해 배합 기술자는 높은 기술적 잠재력과 성능 요구 사항이 있는 틈새 응용 분야를 개척할 수 있습니다.

페인트 및 코팅 분야는 27%의 점유율을 차지하며 2035년까지 CAGR 4.8%로 확대될 것으로 예상됩니다. 중공유리 마이크로스피어는 제품 밀도를 낮추면서 단열성, 차음성을 향상시켜 건설 및 운송 분야의 에너지 효율을 높입니다. 자동차 및 인프라 분야의 최종사용자들은 연료 절감, 운영 효율성, 진화하는 환경 표준에 대한 적합성 등의 이점을 높이 평가하고 있습니다.

북미 중공 유리 마이크로스피어 시장은 2034년 11억 9,000만 달러에 달할 것으로 추정됩니다. 이 지역의 시장 성장은 자동차 분야의 경량화 조치와 에너지 절약형 건축자재, 그리고 산업 및 상업 분야에서의 복합재료의 확립된 용도에 의해 주도되고 있습니다. 미국은 핵심 수요처로서 항공우주, 자동차, 건축용 도료, 석유 및 가스 등의 분야가 신텍틱 폼, 첨단 복합재, 고성능 단열재 응용 분야에서 마이크로스피어 채택을 주도하고 있습니다. 강력한 OEM의 존재, 업데이트된 산업 인프라, 확립된 복합재 제조는 북미 시장에서의 선도적 지위를 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품 유형별, 2022-2035

제6장 시장 추정 및 예측 : 용도별, 2022-2035

제7장 시장 추정 및 예측 : 지역별, 2022-2035

제8장 기업 개요

KSM 26.03.05The Global Hollow Glass Microspheres Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 4.4% to reach USD 3.8 billion by 2035.

Market growth is driven by increasing pressure from fuel efficiency and emissions regulations across the automotive and industrial sectors. Hollow glass microspheres help reduce product weight, enhancing fuel efficiency in vehicles and promoting energy savings in other applications. In North America and Europe, stringent CO2 regulations and net-zero initiatives have motivated vehicle manufacturers and material suppliers to replace traditional mineral fillers with lightweight microspheres. The construction and infrastructure sectors have also contributed significantly, as stricter building energy efficiency regulations encourage the use of microspheres in insulation panels, coatings, and sealants to improve thermal regulation without adding weight. Paints, coatings, and polymer industries are increasingly using microspheres to reduce VOC content, improve acoustic insulation, and produce lightweight, high-performance products across applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $3.8 Billion |

| CAGR | 4.4% |

The coated hollow glass microspheres segment accounted for 54% share in 2025 and is expected to grow at a CAGR of 4.6% through 2035. Manufacturers are increasingly shifting from simply supplying coated microspheres to providing tailored solutions for end-use systems such as epoxy, polyurethane, polyolefin, and specialty-coated applications. Silver and nickel coatings are primarily targeted at electroconductive and EMI-shielding functions, while aluminum and titanium dioxide coatings enhance reflectivity and optical barrier properties. Custom coatings enable formulators to explore niche applications with high technological potential and performance requirements.

The paints and coatings segment held 27% share and is projected to grow at a CAGR of 4.8% by 2035. Hollow glass microspheres reduce product density while improving thermal and acoustic insulation, driving energy efficiency in construction and transport applications. End-users in automotive and infrastructure value these benefits for fuel savings, operational efficiency, and compliance with evolving environmental standards.

North America Hollow Glass Microspheres Market is estimated to reach USD 1.19 billion in 2034. Market growth in the region is fueled by lightweighting initiatives in automotive and energy-efficient building materials, as well as the established use of composites in industrial and commercial sectors. The U.S. serves as the core demand hub, with sectors including aerospace, automotive, construction coatings, and oil & gas driving microsphere adoption for syntactic foams, advanced composites, and high-performance insulation applications. Strong OEM presence, retrofitting of industrial infrastructure, and established composite manufacturing contribute to North America's leading market position.

Key players in the Global Hollow Glass Microspheres Market include Polysciences, Inc, Sovitec, Nova Instruments LLC, Mo-Sci Corporation, Geocon Products, Kish Company Inc, Cenostar Corporation, Dennert Poraver GmbH, Ceno Technologies, Potters Industries LLC, Trelleborg AB, Cospheric LLC, and 3M Company. Companies in the hollow glass microspheres market are employing several strategies to expand their footprint and strengthen market positioning. These include investing heavily in R&D to develop customized microspheres with specialized coatings for specific applications such as EMI shielding, reflectivity, and insulation. Manufacturers are forming strategic partnerships with polymer, automotive, and construction companies to integrate microspheres into advanced formulations. Market players are also expanding geographically to target emerging regions and leveraging digital marketing and technical service support to improve client engagement.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Lightweighting in automotive and transportation

- 3.2.1.2 Demand for energy-efficient, insulated buildings

- 3.2.1.3 Growth of advanced composites and 3D printing

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Higher cost versus conventional mineral fillers

- 3.2.2.2 Processing challenges and crush sensitivity

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in EVs, aerospace and marine sectors

- 3.2.3.2 Use in medical, dental and specialty devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Uncoated hollow glass microspheres

- 5.3 Coated hollow glass microspheres

- 5.3.1 Silver-coated hollow glass microspheres

- 5.3.2 Nickel-coated hollow glass microspheres

- 5.3.3 Aluminum-coated hollow glass microspheres

- 5.3.4 Titanium dioxide-coated hollow glass microspheres

- 5.3.5 Other coated hollow glass microspheres

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Paints & coatings

- 6.2.1 Industrial coatings

- 6.2.2 Marine and protective coatings

- 6.2.3 Automotive refinish and OEM coatings

- 6.2.4 Architectural and decorative paints

- 6.3 Plastics, composites & rubber

- 6.3.1 Thermoplastic composites

- 6.3.2 Thermoset composites (epoxy, polyester)

- 6.3.3 Elastomers and rubber products

- 6.3.4 3D printing and specialty plastics

- 6.4 Transportation

- 6.4.1 Automotive (interiors, body panels)

- 6.4.2 Aerospace and aviation components

- 6.4.3 Rail and marine structures

- 6.4.4 Commercial vehicle and truck parts

- 6.5 Insulation and buoyancy

- 6.5.1 Thermal insulation panels and foams

- 6.5.2 Buoyancy modules for offshore and subsea

- 6.5.3 Pipeline and tank insulation

- 6.5.4 Cryogenic and LNG insulation systems

- 6.6 Healthcare

- 6.6.1 Medical devices and components

- 6.6.2 Dental materials and cements

- 6.6.3 Drug delivery and controlled-release systems

- 6.6.4 Orthopedic and prosthetic composites

- 6.7 Others (applications)

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Polysciences, Inc

- 8.2 Sovitec

- 8.3 Nova Instruments LLC

- 8.4 Mo-Sci Corporation

- 8.5 Geocon Products

- 8.6 Kish Company Inc

- 8.7 Cenostar Corporation

- 8.8 Dennert Poraver Gmbh

- 8.9 Ceno Technologies

- 8.10 Potters Industries LLC

- 8.11 Trelleborg AB

- 8.12 Cospheric LLC

- 8.13 3M Company