|

시장보고서

상품코드

1936578

인터벤션 영상의학 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Interventional Radiology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

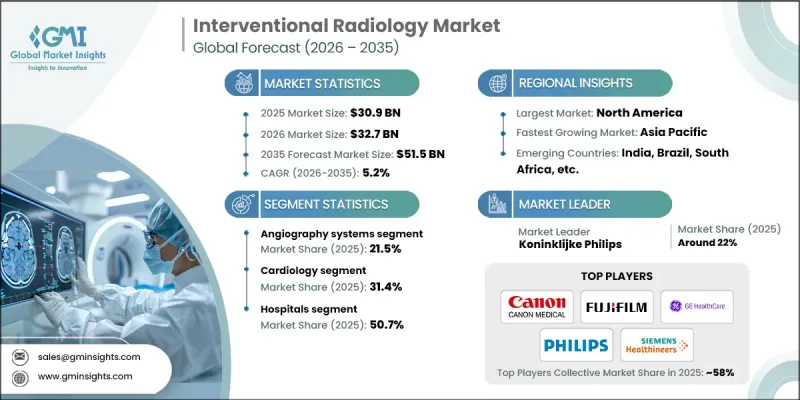

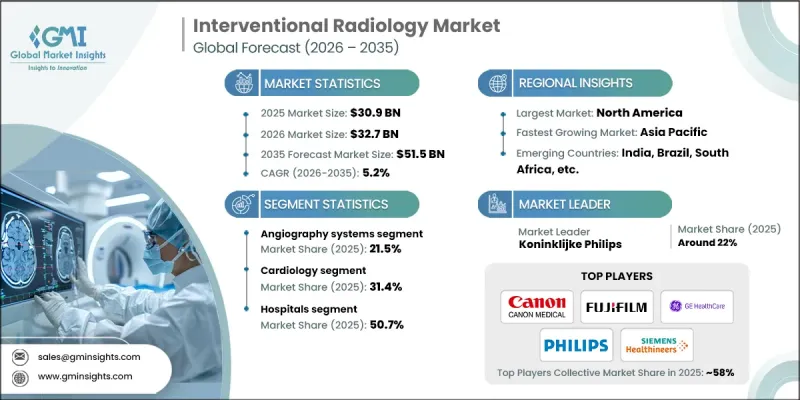

세계의 인터벤션 영상의학 시장은 2025년에 309억 달러로 평가되었으며, 2035년까지 CAGR 5.2%로 성장하여 515억 달러에 달할 것으로 예측됩니다.

시장 확대의 주요 요인으로는 만성질환의 증가, 고령화 사회의 진전, 영상기술의 급속한 발전, 최소침습적 치료법에 대한 수요 확대 등을 들 수 있습니다. 종양학 분야에서의 중재적 방사선학의 채택, 첨단 3D/4D 영상 시스템의 통합, 영상 유도 치료의 보급이 IR 솔루션에 대한 수요를 주도하고 있습니다. 영상 진단용 하드웨어 및 소프트웨어의 지속적인 개선으로 새로운 임상적 응용이 가능해졌으며, 현대의 혈관조영 시스템은 공간적 해상도와 시간적 해상도를 향상시켰습니다. 또한, 융합영상, 3D 시술 로드맵 등의 추가 기술을 통해 시술 중 정밀한 계획 수립과 실시간 내비게이션이 가능해져 시술 성공률 향상과 합병증 감소를 도모하고 있습니다. 이러한 혁신 기술과 더불어 휴대용 영상 진단 시스템의 보급으로 중환자실, 응급실, 자원이 제한된 환경에서 중재적 방사선학의 접근성이 확대되어 세계 시장 성장을 더욱 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 309억 달러 |

| 예측 금액 | 515억 달러 |

| CAGR | 5.2% |

2025년 기준 병원 부문은 50.7%의 점유율을 차지하고 있습니다. 이는 병원이 복잡한 중재 시술을 지원하는 데 필요한 인프라, 다직종 팀, 자본 투자를 제공하기 때문입니다. 대형 대학병원이나 가동률이 높은 지역 병원에서는 고도의 영상 진단, 입원환자 지원, 전문지식을 필요로 하는 고도의 중재적 방사선(IR) 시술을 많이 시행하고 있습니다. 병원은 첨단 기술을 통합하고 시술 중 집중적인 치료 지원을 제공할 수 있기 때문에 복잡한 중재 시술에서 여전히 우선적인 선택이 되고 있습니다.

클리닉 부문은 2025년 7.8억 달러로 평가되며, 영상유도를 통한 최소침습적 중재치료에 대한 외래환자 접근성 확대를 통해 시장 성장에 기여할 것으로 예상됩니다. 전문 인터벤션 영상의학 클리닉은 환자 대응 능력 향상, 전문적 지식 제공, 첨단 영상 진단 시스템 도입, 평가 과정의 효율화를 실현하고 있습니다. 이를 통해 환자의 편의성이 향상될 뿐만 아니라, 병원의 부담도 경감되어 의료 시스템이 고품질의 치료 결과를 유지하면서 보다 효율적으로 의료를 제공할 수 있게 됩니다.

북미 중재적 방사선학 시장은 2025년 36%의 점유율을 차지했습니다. 이 지역의 선도적 지위는 선진화된 의료 인프라, 높은 시술 건수, 첨단 기술의 조기 도입, 탄탄한 상환 체계, 주요 의료기기 제조업체의 집중에 기인합니다. 북미는 또한 높은 1인당 의료비 지출, 공공 및 민간 보험 시스템의 종합적인 보험 적용 범위, 그리고 환자 안전을 보장하면서 혁신을 지원하는 성숙한 규제 환경의 혜택을 누리고 있습니다. 이러한 요인들이 복합적으로 작용하여 이 지역은 중재적 방사선학 솔루션의 주요 시장으로 부상하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품별, 2022-2035

제6장 시장 추정 및 예측 : 용도별, 2022-2035

제7장 시장 추정 및 예측 : 최종 용도별, 2022-2035

제8장 시장 추정 및 예측 : 지역별, 2022-2035

제9장 기업 개요

KSM 26.03.05The Global Interventional Radiology Market was valued at USD 30.9 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 51.5 billion by 2035.

Market expansion is driven by several key factors, including the increasing prevalence of chronic diseases, an aging population, rapid advancements in imaging technologies, and growing demand for minimally invasive procedures. The adoption of interventional radiology in oncology, the integration of advanced 3D and 4D imaging systems, and the rising use of image-guided therapies are fueling the demand for IR solutions. Continuous improvements in imaging hardware and software are unlocking new clinical applications, while modern angiographic systems offer enhanced spatial and temporal resolution. Additional technologies, such as fused imaging and 3D procedural roadmaps, enable precise planning and real-time navigation during procedures, increasing procedural success rates and reducing complications. These innovations, combined with the availability of portable imaging systems, are expanding IR accessibility in intensive care units, emergency departments, and resource-limited settings, further driving the market's growth globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $30.9 Billion |

| Forecast Value | $51.5 Billion |

| CAGR | 5.2% |

The hospitals segment held a 50.7% share in 2025, as hospitals provide the necessary infrastructure, multidisciplinary teams, and capital investment to support complex interventional procedures. Large academic medical centers and high-volume community hospitals perform many advanced IR procedures, particularly those requiring sophisticated imaging, inpatient support, and specialized expertise. Hospitals remain the preferred choice for complex interventions due to their ability to integrate advanced technologies and provide critical care support during procedures.

The clinics segment was valued at USD 7.8 billion in 2025, contributing to market growth by expanding outpatient access to image-guided, minimally invasive interventions. Specialized IR clinics are improving patient throughput, offering focused expertise, advanced imaging systems, and streamlined evaluation processes. This not only enhances patient convenience but also alleviates hospital burdens, enabling healthcare systems to deliver care more efficiently while maintaining high-quality outcomes.

North America Interventional Radiology Market held 36% share in 2025. The region's leadership stems from advanced healthcare infrastructure, high procedure volumes, early adoption of cutting-edge technologies, robust reimbursement frameworks, and concentration of top medical device manufacturers. North America also benefits from high per-capita healthcare spending, comprehensive insurance coverage through public and private systems, and a mature regulatory environment that supports innovation while ensuring patient safety. These factors make the region a prime market for interventional radiology solutions.

Key players in the Global Interventional Radiology Market include Agfa-Gevaert Group, Canon Medical Systems, Carestream Health Inc., Cook, Esaote SPA, Fujifilm Corporation, GE Healthcare, Hologic, Inc., Koninklijke Philips, Mindray, Olympus Corporation, Samsung Healthcare, Shimadzu Corporation, Siemens Healthineers, and Teleflex. Companies in the interventional radiology market are strengthening their foothold by investing in R&D for advanced imaging technologies, 3D/4D navigation systems, and AI-assisted procedural planning. Strategic partnerships with hospitals, clinics, and health systems enhance market reach and clinical integration. Firms are also expanding service networks and offering training programs to improve adoption and maximize equipment utilization. Focused innovation in portable and minimally invasive systems allows companies to target underserved markets. Additionally, adopting value-based solutions, flexible financing models, and cloud-enabled imaging platforms helps firms improve patient outcomes while reinforcing their competitive positioning in key regions worldwide.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic disease worldwide

- 3.2.1.2 Technological advancements in medical imaging

- 3.2.1.3 Increasing demand for minimally invasive procedures

- 3.2.1.4 Growing elderly population base

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with product

- 3.2.2.2 Complex regulatory scenario

- 3.2.3 Opportunities

- 3.2.3.1 AI- and robotics-enabled image-guided interventions

- 3.2.3.2 Increasing investments in hybrid operating rooms

- 3.2.3.3 Development of low-radiation and radiation-free imaging technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Value chain analysis

- 3.7 Reimbursement scenario

- 3.8 In-patient to outpatient shift landscape

- 3.9 Pricing analysis

- 3.10 Policy landscape

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Gap analysis

- 3.14 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Angiography systems

- 5.3 Ultrasound imaging systems

- 5.4 CT scanners

- 5.5 MRI systems

- 5.6 Fluoroscopy systems

- 5.7 Biopsy devices

- 5.8 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Cardiology

- 6.3 Oncology

- 6.4 Gynecology

- 6.5 Obstetrics

- 6.6 Urology

- 6.7 Gastroenterology

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Clinics

- 7.4 Ambulatory surgical centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Agfa-Gevaert Group

- 9.2 Canon Medical Systems

- 9.3 Carestream Health Inc.

- 9.4 Cook

- 9.5 Esaote SPA

- 9.6 Fujifilm Corporation

- 9.7 GE Healthcare

- 9.8 Hologic, Inc.

- 9.9 Koninklijke Philips

- 9.10 Mindray

- 9.11 Olympus Corporation

- 9.12 Samsung Healthcare

- 9.13 Shimadzu Corporation

- 9.14 Siemens Healthineers

- 9.15 Teleflex