|

시장보고서

상품코드

1936581

의료장비 냉각 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Medical Equipment Cooling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

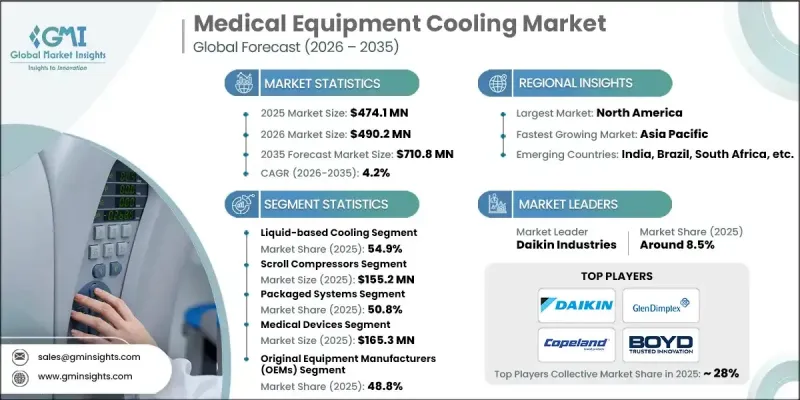

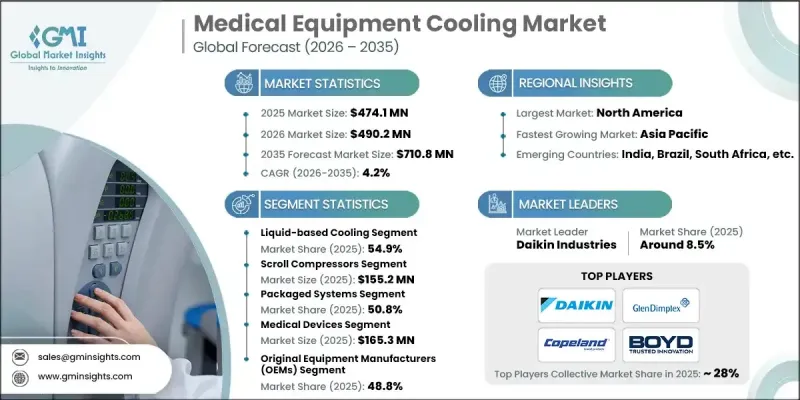

세계의 의료장비 냉각 시장은 2025년에 4억 7,410만 달러로 평가되었으며, 2035년까지 CAGR 4.2%로 성장하여 7억 1,080만 달러에 달할 것으로 예측됩니다.

시장 성장은 만성질환의 증가, 최소침습 수술의 보급 확대, 진단용 영상 장비의 기술 발전, 의료 시설에서 정밀한 온도 관리의 필요성 증가 등 여러 가지 상호 연관된 요인에 의해 촉진되고 있습니다. 첨단 의료기기의 신뢰성, 수명 및 최고 성능을 유지하기 위해서는 열 관리 시스템이 필수적이며, 냉각 솔루션에 대한 지속적인 투자를 주도하고 있습니다. 암 발병률의 증가와 기타 만성질환의 확대로 인해 MRI 장비, CT 스캐너, 리니어락, PET-CT 시스템, 실험실 장비 등 대용량 냉각 솔루션을 필요로 하는 장비에 대한 수요가 증가하고 있습니다. 고자기장 MRI 장비만 해도 시스템당 30-50kW의 냉각 용량이 필요하기 때문에 강력한 열 관리의 중요성이 부각되고 있습니다. 또한, 전 세계 의료 인프라의 확충, 기술 혁신, 임상 기준의 향상도 의료장비 냉각 솔루션에 대한 지속적인 수요에 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 4억 7,410만 달러 |

| 예측 금액 | 7억 1,080만 달러 |

| CAGR | 4.2% |

액체 기반 냉각 시스템 부문은 높은 열 제거 효율로 인해 2025년 54.9%의 점유율을 차지했습니다. 냉수 냉각기, 글리콜 냉각 장치, 직접 냉매 기술 등을 포함한 이러한 시스템은 MRI, CT 장비, 리니어락 등 열 부하가 높은 응용 분야에 적합합니다. 액체 냉각은 공랭식 시스템에 비해 컴팩트한 디자인과 정숙성을 실현하기 때문에 병원 및 임상 환경에 적합합니다. 에너지 효율, 저소음, 고밀도 방열에 대한 관심이 높아지면서 전 세계 의료 시설에서 액체 냉각 기술 채택이 더욱 가속화되고 있습니다.

스크롤 컴프레서 분야는 2025년 1억 5,520만 달러의 시장 규모를 형성했으며, 5-60톤의 냉각 용량을 가진 중소형 애플리케이션에서 선두를 유지하고 있습니다. 높은 신뢰성, 저진동, 정숙성을 갖추고 있어 MRI 냉각장치, CT 스캐너, 정밀 실험실 공조 시스템에 널리 채택되고 있습니다. 평균 고장 간격(MTBF)이 10만 시간에 달하는 스크롤 컴프레서는 의료의 중요한 환경에서 신뢰할 수 있는 성능을 제공합니다. 스크롤링 기술에 대한 선호는 환자 치료 공간 및 실험실 환경에서 필수적인 저소음의 안정적인 냉각 성능에 기인합니다.

북미 의료장비 냉각 시장은 2025년 34.4%의 점유율을 차지했으며, 예측 기간 동안 견조한 성장세를 유지할 것으로 예상됩니다. 이 지역은 진단 영상 인프라가 선진화되어 있고, 노후화된 장비의 지속적인 교체가 이루어지고 있어 첨단 냉각 솔루션에 대한 수요가 증가하고 있습니다. 북미 병원 및 연구센터에서는 프리미엄 기능을 지원하고 장비의 최적의 기능을 보장하는 고성능, 고신뢰성 냉각 시스템에 대한 수요가 증가하고 있습니다. 규제 기준과 운영 효율성에 대한 관심은 첨단 열 관리 시스템에 대한 투자를 촉진하여 시장 확대를 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품별, 2022-2035

제6장 시장 추정 및 예측 : 컴프레서별, 2022-2035

제7장 시장 추정 및 예측 : 구성별, 2022-2035

제8장 시장 추정 및 예측 : 용도별, 2022-2035

제9장 시장 추정 및 예측 : 최종 용도별, 2022-2035

제10장 시장 추정 및 예측 : 지역별, 2022-2035

제11장 기업 개요

KSM 26.03.05The Global Medical Equipment Cooling Market was valued at USD 474.1 million in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 710.8 million by 2035.

Market growth is fueled by several interconnected factors, including the rising prevalence of chronic diseases, expanding adoption of minimally invasive surgeries, technological advancements in diagnostic imaging devices, and the growing need for precise temperature control in healthcare facilities. Thermal management systems are critical in maintaining the reliability, longevity, and peak performance of sophisticated medical equipment, driving ongoing investment in cooling solutions. Increasing cancer incidence and other chronic conditions are boosting the demand for MRI units, CT scanners, linear accelerators, PET-CT systems, and laboratory equipment, all of which require high-capacity cooling solutions. High-field MRI units alone demand 30-50 kW of cooling per system, highlighting the importance of robust thermal management. Additionally, the expanding global healthcare infrastructure, technological innovation, and rising clinical standards contribute to sustained demand for medical equipment cooling solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $474.1 Million |

| Forecast Value | $710.8 Million |

| CAGR | 4.2% |

The liquid-based cooling systems segment accounted for 54.9% share in 2025, driven by their high heat removal efficiency. These systems, including chilled water chillers, glycol cooling units, and direct refrigerant technologies, are ideal for applications with high thermal loads, such as MRI and CT machines or linear accelerators. Liquid cooling offers compact designs and quieter operation compared to air-cooled systems, making them well-suited for hospital and clinical environments. The growing focus on energy efficiency, reduced noise levels, and high-density heat dissipation further accelerates the adoption of liquid-based cooling technologies across healthcare facilities globally.

The scroll compressors segment generated USD 155.2 million in 2025 and continues to dominate small- to medium-capacity applications ranging from 5 to 60 tons of cooling. They are widely deployed in MRI chillers, CT scanners, and precision laboratory air conditioning systems due to their high reliability, low vibration, and quiet operation. With an average time between failures of 100,000 hours, scroll compressors provide dependable performance in critical healthcare environments. The preference for scroll technology is also driven by its ability to deliver consistent cooling at lower operational noise levels, which is essential in patient care areas and laboratory settings.

North America Medical Equipment Cooling Market held 34.4% share in 2025 and is expected to maintain strong growth during the forecast period. The region leads in diagnostic imaging infrastructure and ongoing replacement of aging equipment, resulting in heightened demand for advanced cooling solutions. Hospitals and research centers in North America increasingly require high-performance, reliable cooling systems that support premium features and ensure optimal equipment functionality. Regulatory standards and a focus on operational efficiency also encourage investment in advanced thermal management systems, further supporting market expansion.

Key players in the Global Medical Equipment Cooling Market include American Chillers, Atlas Copco, Boyd, Copeland, Daikin Industries, Drake Refrigeration, Ecochillers, EKS Thermal Systems, ELGi Equipments Limited, Filtrine, General Air Products, Glen Dimplex Group, Haskris, Ingersoll Rand, KKT Chillers, Legacy Chillers, Motivair Corporation, Tark Thermal Solutions, and Thermal Care. Companies are strengthening market presence through continuous R&D to enhance liquid and air-cooled system efficiency, noise reduction, and compact design. Strategic partnerships with hospitals, diagnostic centers, and medical equipment manufacturers help expand distribution channels. Many players are introducing modular and scalable cooling solutions to cater to diverse healthcare facilities. Investments in energy-efficient, eco-friendly, and low-maintenance technologies help firms differentiate their offerings.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Compressor trends

- 2.2.4 Configuration trends

- 2.2.5 Application trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Technological advancements in diagnostic imaging modalities

- 3.2.1.3 Growing demand for temperature control

- 3.2.1.4 Rising adoption of minimally invasive surgical techniques

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Upfront costs associated with purchasing and installing medical equipment cooling systems

- 3.2.2.2 Regulatory compliance challenges

- 3.2.3 Opportunities

- 3.2.3.1 Increased investment in new medical imaging and diagnostic equipment

- 3.2.3.2 Expanding applications of cooling systems in new medical technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Value chain analysis

- 3.7 Pricing analysis

- 3.8 Environmental and sustainability considerations

- 3.9 Policy landscape

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis, by compressors

- 4.3.1 Reciprocating compressors

- 4.3.2 Scroll compressors

- 4.3.3 Screw compressors

- 4.3.4 Centrifugal compressors

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Liquid-based cooling

- 5.3 Air-based cooling

Chapter 6 Market Estimates and Forecast, By Compressor, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Reciprocating compressors

- 6.3 Scroll compressors

- 6.4 Screw compressors

- 6.5 Centrifugal compressors

Chapter 7 Market Estimates and Forecast, By Configuration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Packaged systems

- 7.3 Modular systems

- 7.4 Split systems

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Medical devices

- 8.2.1 Medical imaging systems

- 8.2.1.1 Magnetic resonance imaging systems (MRI)

- 8.2.1.2 Computed tomography scanners (CT)

- 8.2.1.3 Positron emission tomography systems (PET)

- 8.2.2 Medical lasers

- 8.2.3 Linear accelerators

- 8.2.1 Medical imaging systems

- 8.3 Cold Storage and testing

- 8.4 Dehumidification

- 8.5 Analytical & laboratory equipment

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Original equipment manufacturers (OEMs)

- 9.3 Hospitals

- 9.4 Diagnostic laboratories

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 American Chillers

- 11.2 Atlas Copco

- 11.3 Boyd

- 11.4 Copeland

- 11.5 Daikin Industries

- 11.6 Drake Refrigeration

- 11.7 Ecochillers

- 11.8 EKS Thermal Systems

- 11.9 ELGi Equipments Limited

- 11.10 Filtrine

- 11.11 General Air Products

- 11.12 Glen Dimplex Group

- 11.13 Haskris

- 11.14 Ingersoll Rand

- 11.15 KKT chillers

- 11.16 Legacy Chillers

- 11.17 Motivair Corporation

- 11.18 Tark Thermal Solutions

- 11.19 Thermal Care