|

시장보고서

상품코드

1936584

금속 접착제 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Metal Bonding Adhesives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

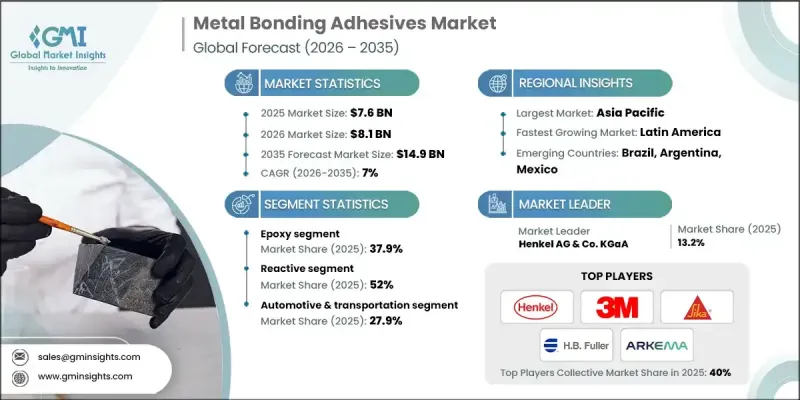

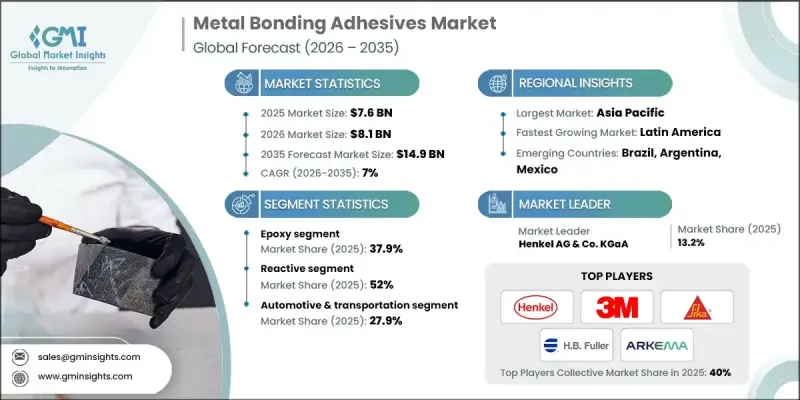

세계의 금속용 접착제 시장은 2025년에 76억 달러로 평가되었으며, 2035년까지 7%의 CAGR로 성장하여 149억 달러에 달할 것으로 예측됩니다.

시장 확대는 전통적인 접합 기술에서 고강도, 유연성, 내구성 및 무게 최적화를 실현하는 첨단 접착제 솔루션으로의 전환이 가속화되고 있기 때문입니다. 업계에서는 최신 설계 요구 사항을 지원하고 재료의 스트레스를 줄이고 전체 구조의 성능을 향상시키는 접착 기술을 점점 더 우선시하고 있습니다. 자동차 및 운송 분야는 제조업체들이 경량화 전략을 강화하고 차세대 차량 플랫폼에 첨단 소재를 통합함에 따라 수요 증가의 중심이 되고 있습니다. 금속 접착제는 구조적 무결성과 설계의 자유도를 유지하면서 다양한 기판의 효과적인 접합을 가능하게 합니다. 항공우주 및 방위 분야는 시장의 모멘텀을 뒷받침하고 있습니다. 제조업체들은 복잡한 조립 구조에서 구조적 안정성, 내진동성, 장기 내구성을 높이기 위해 고성능 접착제 시스템에 지속적으로 의존하고 있습니다. 민간 항공 분야의 활동 증가와 국방 투자의 지속으로 인해 전 세계 제조 거점에서의 수요가 강화되고 있습니다. 산업계가 효율성 향상, 배출량 감소, 제품 수명주기 강화를 추구함에 따라 금속 접착제는 현대의 제조 및 조립 공정에서 필수적인 요소로 자리 잡고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 76억 달러 |

| 예측 금액 | 149억 달러 |

| CAGR | 7% |

에폭시 접착제 부문은 2025년 37.9%의 점유율을 차지했으며, 2035년까지 연평균 6.9%의 성장률을 기록할 것으로 전망됩니다. 높은 기계적 강도, 열 안정성, 내화학성, 장기 내구성 등의 특징으로 인해 까다로운 조건이 요구되는 산업, 운송, 항공우주 분야의 용도에 적합하여 널리 채택되고 있습니다. 다양한 작동 조건에서의 적응성이 안정적인 수요를 지속적으로 뒷받침하고 있습니다.

반응성 접착제 부문은 2025년에 52%의 점유율을 차지하고 2035년까지 7.1%의 CAGR로 성장할 것으로 예상됩니다. 이 시스템은 화학적 경화 메커니즘을 통해 내구성 있는 구조적 결합을 형성할 수 있는 능력으로 여러 산업 분야에서 높은 스트레스와 부하가 가해지는 조건에서도 신뢰할 수 있는 성능을 발휘하는 것으로 유명합니다.

미국 금속 접착제 시장은 2025년 15억 달러에 달할 것으로 예상되며, 강력한 성장 잠재력을 보여주고 있습니다. 첨단 제조, 전기화 이니셔티브 및 고부가가치 산업 생산에 대한 지속적인 투자로 인해 미국 전역에서 고성능 접착제 기술에 대한 수요가 지속되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 수지 유형별, 2022-2035

제6장 시장 추정 및 예측 : 기술별, 2022-2035

제7장 시장 추정 및 예측 : 최종 이용 산업별, 2022-2035

제8장 시장 추정 및 예측 : 지역별, 2022-2035

제9장 기업 개요

KSM 26.03.05The Global Metal Bonding Adhesives Market was valued at USD 7.6 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 14.9 billion by 2035.

Market expansion is driven by the accelerating shift away from conventional joining techniques toward advanced adhesive solutions that deliver high strength, flexibility, durability, and weight optimization. Industries are increasingly prioritizing bonding technologies that support modern design requirements, reduce material stress, and improve overall structural performance. Automotive and transportation applications remain central to demand growth as manufacturers intensify lightweighting strategies and integrate advanced materials into next-generation vehicle platforms. Metal bonding adhesives enable effective joining of varied substrates while maintaining structural integrity and design freedom. The aerospace and defense sector support market momentum, as manufacturers continue to rely on high-performance adhesive systems to enhance structural stability, vibration resistance, and long-term durability in complex assemblies. Rising activity across commercial aviation and sustained defense investments are reinforcing demand across global manufacturing hubs. As industries pursue improved efficiency, lower emissions, and enhanced product lifecycles, metal bonding adhesives are becoming an essential component of modern fabrication and assembly processes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.6 Billion |

| Forecast Value | $14.9 Billion |

| CAGR | 7% |

The epoxy-based adhesives segment accounted for 37.9% share in 2025 and is expected to grow at a CAGR of 6.9% through 2035. Their strong adoption is supported by high mechanical strength, thermal stability, chemical resistance, and long-term durability, making them suitable for demanding industrial, transportation, and aerospace applications. Their adaptability across a wide range of operating conditions continues to support consistent demand.

The reactive adhesives segment held 52% share in 2025 and is projected to grow at a CAGR of 7.1% by 2035. These systems are favored for their ability to form durable structural bonds through chemical curing mechanisms, delivering reliable performance under high stress and load-bearing conditions across multiple industries.

U.S. Metal Bonding Adhesives Market reached USD 1.5 billion in 2025 and continues to show strong growth potential. Ongoing investments in advanced manufacturing, electrification initiatives, and high-value industrial production are sustaining demand for high-performance adhesive technologies across the country.

Key players in the Global Metal Bonding Adhesives Market include Henkel AG & Co. KGaA, 3M Company, BASF SE, Sika AG, Arkema Group, H.B. Fuller, DuPont, Huntsman Corporation, Evonik Industries, Solvay S.A., Ashland Inc., ITW Performance Polymers, Dymax Corporation, LORD Corporation, Panacol-Elosol GmbH, Permabond LLC, L&L Products, Parson Adhesives Inc., Toagosei Co., Ltd., and DELO Industrie Klebstoffe GmbH & Co KGaA. Companies operating in the metal bonding adhesives market are strengthening their market position through continuous innovation, targeted product development, and strategic partnerships with end-use industries. Manufacturers are investing in advanced formulations that improve bonding strength, environmental resistance, and processing efficiency. Expansion of production capabilities in high-growth regions, customization of solutions for industry-specific requirements, and focus on sustainability-driven product portfolios are also central strategies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Resin type

- 2.2.3 Technology

- 2.2.4 End use industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By resin type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Resin Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Epoxy

- 5.3 Polyurethane

- 5.4 Acrylic

- 5.5 Cyanoacrylate

- 5.6 Anaerobic

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solvent-Based

- 6.3 Water-Based

- 6.4 Reactive

- 6.5 Hot Melt

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive & Transportation

- 7.2.1 Passenger Cars

- 7.2.2 Commercial Vehicles

- 7.2.3 Railways & Metro Systems

- 7.2.4 Electric Vehicles (EVs)

- 7.2.5 Marine

- 7.2.6 Specialty Vehicles

- 7.3 Aerospace & Defense

- 7.3.1 Commercial Aviation

- 7.3.2 Military Aircraft & Equipment

- 7.3.3 Spacecraft & Satellites

- 7.3.4 Unmanned Aerial Vehicles

- 7.4 Electronics & Consumer

- 7.4.1 Printed Circuit Boards (PCBs)

- 7.4.2 Semiconductors & Microelectronics

- 7.4.3 Smartphones & Wearables

- 7.4.4 Televisions & Displays

- 7.4.5 Home Appliances

- 7.4.6 Batteries & Electrical Assemblies

- 7.5 Medical & Pharmaceutical

- 7.5.1 Medical Equipment

- 7.5.2 Dental Instruments & Devices

- 7.5.3 Surgical Tools & Implants

- 7.5.4 Drug Delivery Systems

- 7.5.5 Wearable Health Devices

- 7.6 Industrial Equipment & Machinery

- 7.6.1 Heavy Machinery

- 7.6.2 General Manufacturing Equipment

- 7.6.3 Robotics & Automation Systems

- 7.6.4 Pumps, Valves & Compressors

- 7.6.5 HVAC Systems

- 7.7 Construction & Infrastructure

- 7.7.1 Structural Steel Bonding

- 7.7.2 Facade & Curtain Walls

- 7.7.3 Metal Frame Assembly

- 7.7.4 Architectural Panels

- 7.7.5 HVAC Ducts/Pipe Bonding

- 7.8 Energy

- 7.8.1 Wind Turbine Blade Assembly

- 7.8.2 Solar Panel Framing

- 7.8.3 Battery Systems

- 7.8.4 Fuel Cells

- 7.8.5 Power Transmission Equipment

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 3M Company

- 9.2 Arkema Group

- 9.3 Ashland Inc.

- 9.4 BASF SE

- 9.5 DELO Industrie Klebstoffe GmbH & Co KGaA

- 9.6 DuPont

- 9.7 Dymax Corporation

- 9.8 Evonik Industries

- 9.9 H.B. Fuller

- 9.10 Henkel AG & Co. KGaA

- 9.11 Huntsman Corporation

- 9.12 ITW Performance Polymers

- 9.13 L&L Products

- 9.14 LORD Corporation

- 9.15 Panacol-Elosol GmbH

- 9.16 Parson Adhesives Inc.

- 9.17 Permabond LLC

- 9.18 Sika AG

- 9.19 Solvay S.A.

- 9.20 Toagosei Co., Ltd.

- 9.21 Others