|

시장보고서

상품코드

1936599

간암 치료제 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Liver Cancer Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

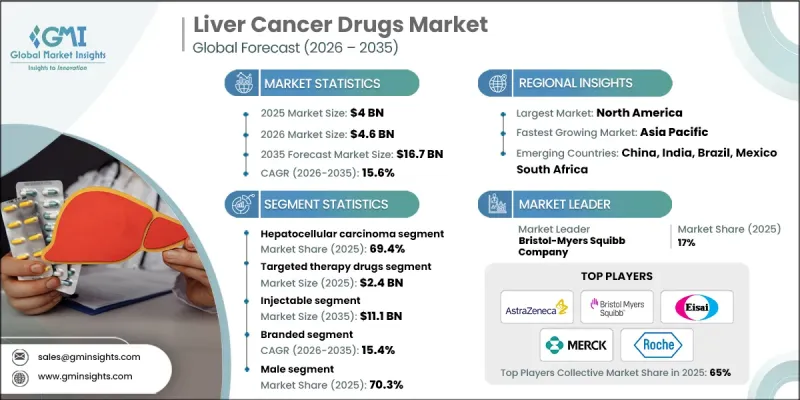

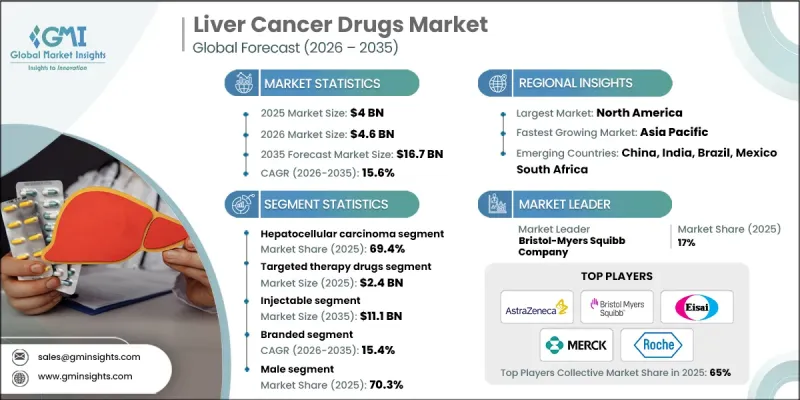

세계의 간암 치료제 시장은 2025년에 40억 달러로 평가되었으며, 2035년까지 CAGR 15.6%로 성장하여 167억 달러에 달할 것으로 예측됩니다.

시장 성장은 전 세계적으로 원발성 간암 발생률 증가와 진단 지연 및 근본적인 치료 옵션이 제한적이어서 지속적으로 높은 사망률에 의해 주도되고 있습니다. 간암은 여전히 가장 치사율이 높은 종양 질환 중 하나이며, 생존기간을 연장하고 질병 진행을 지연시키는 효과적인 약물요법이 절실히 요구되고 있습니다. 간암 치료제 시장은 치료 성과와 삶의 질을 개선하기 위해 고안된 치료법을 포함하여 간 악성 종양 관리에 사용되는 의약품 치료제의 연구, 생산, 상업화를 포괄합니다. 약물 개발의 초점은 표적 치료제, 면역치료제, 생물학적 제제, 화학요법 기반 요법으로 점점 더 옮겨가고 있습니다. 많은 환자들이 진행성 단계에서 진단되기 때문에 전신 치료는 질병 관리에 있어 매우 중요한 역할을 합니다. 강력한 종양학 연구 파이프라인, 지원적인 규제 프레임워크, 확대되는 보험 적용 범위는 혁신을 촉진하고 환자 접근을 가속화하기 위해 지속적으로 노력하고 있습니다. 정밀의료와 병용치료 전략이 확산되는 가운데 간암치료제에 대한 제약투자가 활발해지면서 시장은 지속적이고 장기적인 확대 기반을 마련하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 40억 달러 |

| 예측 금액 | 167억 달러 |

| CAGR | 15.6% |

2025년 기준 간세포암 부문은 69.4%의 점유율을 차지하고 있으며, 2035년까지 CAGR 15.5%로 성장할 것으로 예상됩니다. 이러한 우위는 전 세계적으로 이 암종의 높은 발병률과 병용요법 및 면역요법을 포함한 치료 접근법의 지속적인 발전을 반영하고 있습니다. 기저 간질환의 지속적인 유병률은 효과적인 치료 옵션에 대한 강력한 수요를 뒷받침하고 있습니다.

주사제 부문은 2025년 27억 달러의 시장 규모를 기록했으며, 2035년까지 111억 달러로 성장할 것으로 전망됩니다. 주사제 제제는 관리된 투여와 임상적 모니터링이 필요한 면역요법 및 생물학적 제제에 적합하기 때문에 고급 치료 환경에서 널리 사용되고 있습니다. 1차 치료 및 병용요법에서 확립된 역할은 이 부문의 선도적 지위를 더욱 뒷받침하고 있습니다.

북미 간암 치료제 시장은 2025년 41.1%의 점유율을 차지했습니다. 이러한 지역적 우위는 강력한 규제 경로, 첨단 진단 인프라, 혁신적인 치료법의 조기 도입, 그리고 잘 구축된 임상 연구 생태계에 의해 뒷받침되고 있습니다. 유리한 상환 정책과 조기 발견 및 치료 최적화에 대한 관심이 높아지면서 수요를 지속적으로 견인하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 유형별, 2022-2035

제6장 시장 추정 및 예측 : 약물 종류별, 2022-2035

제7장 시장 추정 및 예측 : 투여 경로별, 2022-2035

제8장 시장 추정 및 예측 : 약물 유형별, 2022-2035

제9장 시장 추정 및 예측 : 성별, 2022-2035

제10장 시장 추정 및 예측 : 최종 용도별, 2022-2035

제11장 시장 추정 및 예측 : 지역별, 2022-2035

제12장 기업 개요

KSM 26.03.05The Global Liver Cancer Drugs Market was valued at USD 4 billion in 2025 and is estimated to grow at a CAGR of 15.6% to reach USD 16.7 billion by 2035.

Market growth is driven by the rising incidence of primary liver cancers worldwide and the persistently high mortality rates associated with delayed diagnosis and limited curative treatment options. Liver cancer remains one of the most fatal oncology indications, creating an urgent need for effective drug-based therapies that can extend survival and slow disease progression. The liver cancer drugs market encompasses the research, production, and commercialization of pharmaceutical treatments used to manage liver malignancies, including therapies designed to improve outcomes and quality of life. Drug innovation is increasingly focused on targeted agents, immunotherapies, biologics, and chemotherapy-based regimens. Because many patients are diagnosed at advanced stages, systemic therapies play a critical role in disease management. Strong oncology research pipelines, supportive regulatory frameworks, and expanding reimbursement coverage continue to encourage innovation and accelerate patient access. As precision medicine and combination treatment strategies gain traction, pharmaceutical investment in liver cancer therapeutics is intensifying, positioning the market for sustained long-term expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4 Billion |

| Forecast Value | $16.7 Billion |

| CAGR | 15.6% |

The hepatocellular carcinoma segment accounted for 69.4% share in 2025 and is expected to grow at a CAGR of 15.5% throughout 2035. This dominance reflects the high global burden of this cancer type and continued advancements in treatment approaches, including combination therapies and immune-based drugs. Ongoing prevalence of underlying liver conditions continues to support strong demand for effective therapeutic options.

The injectable segment generated USD 2.7 billion in 2025 and is projected to grow to USD 11.1 billion by 2035. Injectable formulations are widely used in advanced treatment settings due to their suitability for immunotherapies and biologics, which require controlled administration and clinical supervision. Their established role in first line and combination regimens further supports segment leadership.

North America Liver Cancer Drugs Market held 41.1% share in 2025. Regional dominance is supported by strong regulatory pathways, advanced diagnostic infrastructure, early adoption of innovative therapies, and a well-developed clinical research ecosystem. Favorable reimbursement policies and increasing focus on early detection and treatment optimization continue to drive demand.

Key companies operating in the Global Liver Cancer Drugs Market include Merck & Co., F. Hoffmann-La Roche, AstraZeneca, Bayer, Bristol-Myers Squibb Company, Regeneron Pharmaceuticals, Johnson & Johnson, Eisai, Exelixis, Sanofi, Amgen, AbbVie, Taiho Pharmaceutical, Servier Pharmaceuticals, and Glenmark Pharmaceuticals. Companies in the liver cancer drugs market are strengthening their competitive position through aggressive research and development initiatives focused on novel drug targets and combination therapies. Many players are expanding immuno-oncology portfolios and investing in precision medicine to improve treatment response rates. Strategic collaborations with research institutions and biotechnology firms are accelerating clinical development timelines. Companies are also prioritizing regulatory approvals across multiple regions to expand market access. Lifecycle management strategies, including label expansions and next-generation formulations, are being used to extend product value.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Drug class trends

- 2.2.4 Route of administration trends

- 2.2.5 Medication type trends

- 2.2.6 Gender trends

- 2.2.7 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global incidence of liver cancer

- 3.2.1.2 Shift toward targeted and immuno-oncology therapies

- 3.2.1.3 Expanding geriatric population

- 3.2.1.4 Rising healthcare expenditure and oncology focus

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs and reimbursement constraints

- 3.2.2.2 Late diagnosis limiting treatment eligibility

- 3.2.3 Market opportunities

- 3.2.3.1 Next-generation combination and personalized therapies

- 3.2.3.2 Growth potential in emerging, high-burden regions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Liver cancer statistics, by region

- 3.6 Future market trends

- 3.7 Pipeline analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Hepatocellular carcinoma

- 5.3 Cholangiocarcinoma

- 5.4 Hepatoblastoma

- 5.5 Liver metastasis

- 5.6 Other types

Chapter 6 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Chemotherapeutic agents

- 6.3 Targeted therapy drugs

- 6.4 Immunotherapy drugs

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

Chapter 8 Market Estimates and Forecast, By Medication Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Generic

- 8.3 Branded

Chapter 9 Market Estimates and Forecast, By Gender, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Male

- 9.3 Female

Chapter 10 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Hospitals

- 10.3 Specialty cancer centers

- 10.4 Research and academic centers

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 AbbVie

- 12.2 Amgen

- 12.3 AstraZeneca

- 12.4 Bayer

- 12.5 Bristol-Myers Squibb Company

- 12.6 Eisai

- 12.7 Exelixis

- 12.8 F. Hoffmann-La Roche

- 12.9 Glenmark Pharmaceuticals

- 12.10 Johnson & Johnson

- 12.11 Merck & Co.

- 12.12 Regeneron Pharmaceuticals

- 12.13 Sanofi

- 12.14 Servier Pharmaceuticals

- 12.15 Taiho Pharmaceutical