|

시장보고서

상품코드

1936615

클린룸 장비 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Cleanroom Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

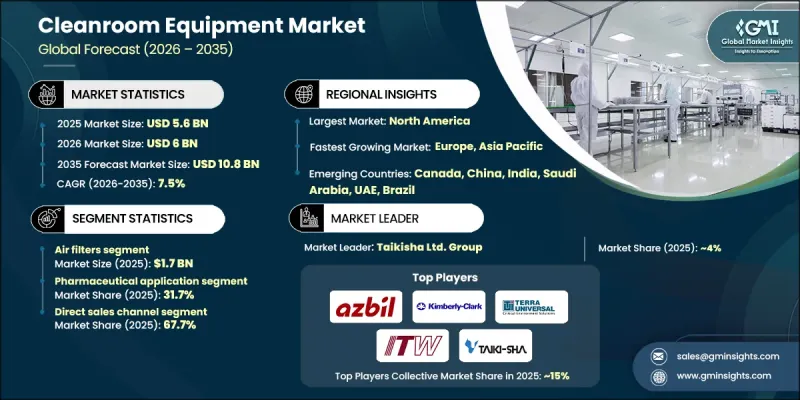

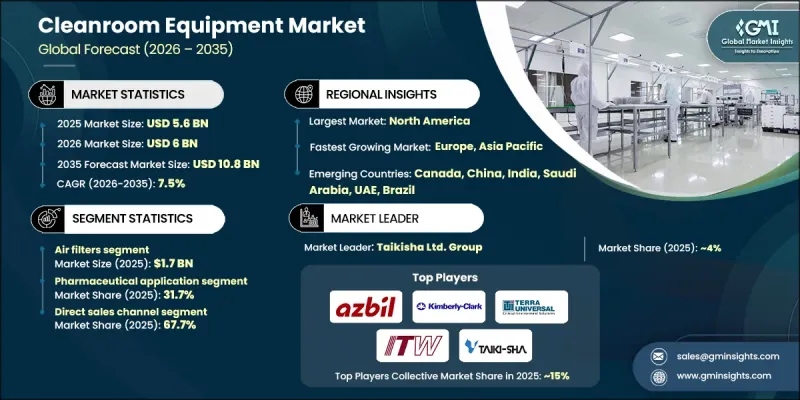

세계의 클린룸 장비 시장은 2025년에 56억 달러로 평가되었으며, 2035년까지 CAGR 7.5%로 성장하여 108억 달러에 달할 것으로 예측됩니다.

의약품, 생명공학, 첨단 치료법의 제조가 전 세계적으로 확대됨에 따라 시장은 빠르게 성장하고 있습니다. 무균 주사제, 생물학적 제제, 백신, 맞춤형 의료, 세포 및 유전자 치료제의 생산이 증가함에 따라 통제된 제조 환경에 대한 수요가 크게 증가하고 있습니다. 이러한 생산 공간에는 최첨단 공조 시스템, HEPA 및 ULPA 필터, 고급 공기 처리 장치, 지속적인 환경 모니터링이 필요합니다. 성장을 촉진하는 또 다른 중요한 요인은 모듈식 및 유연한 클린룸 솔루션의 채택이 증가하고 있다는 점입니다. 제조업체들은 낮은 설치 비용, 빠른 도입, 그리고 진화하는 규제와 생산 요구에 따라 생산 공간을 확장할 수 있다는 점에서 모듈식 클린룸을 선호합니다. 생산량 증가 및 규제 준수에 대응하기 위해 클린룸 레이아웃을 신속하게 확장하거나 재구성할 수 있는 유연성이 전 세계적으로 채택을 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 56억 달러 |

| 예측 금액 | 108억 달러 |

| CAGR | 7.5% |

에어 필터 부문은 2025년 17억 달러의 시장 규모를 기록했으며, 2026년부터 2035년까지 CAGR 7.7%로 성장할 것으로 예측됩니다. 제약, 생명공학, 반도체 제조, 의료 산업의 엄격한 오염 관리 규정이 고효율 HEPA 및 ULPA 필터에 대한 수요를 주도하고 있습니다. 정밀 전자장비, 나노기술 부품, 의료장비를 제조하는 산업에서는 초 청정 공기 환경이 필요하며, 신규 클린룸 설치 및 기존 시설의 개보수 모두에서 고급 여과 솔루션에 대한 수요가 증가하고 있습니다.

2025년 기준 직접 판매 부문은 67.7%의 점유율을 차지하고 있으며, 2035년까지 CAGR 7.2%로 성장할 것으로 예상됩니다. 직접 판매를 통해 기업은 특수 공조 장치, 통합형 라미나르 플로우 시스템, 실시간 모니터링 기능을 갖춘 자동화 시스템 등 맞춤형 솔루션을 제공할 수 있습니다. 이러한 접근 방식은 GMP, FDA, EMA, ISO 및 산업별 표준 준수를 보장하는 동시에 단일 소스로부터 완전한 문서화, 검증 및 적격성 확인을 제공합니다. OEM 제조업체는 설계, 설치, 시운전, 수명주기 유지보수를 통해 고객을 지원하여 미션 크리티컬한 클린룸 운영에서 오염 위험과 다운타임을 최소화할 수 있도록 지원합니다.

미국 클린룸 장비 시장은 2025년 15억 달러에 달했으며, 2026년부터 2035년까지 연평균 7.2%의 성장률을 기록할 것으로 전망됩니다. 바이오의약품, 백신, 무균 주사제, 첨단 치료법 등 제약 및 생명공학 산업의 호조는 클린룸 장비에 대한 안정적인 수요를 견인하고 있습니다. 위탁개발제조기관(CDMO)에 대한 의존도가 높아지면서 다품종 대응이 가능한 유연한 클린룸 시설의 구축이 가속화되고 있어 시장 확대에 더욱 박차를 가하고 있습니다. 첨단 공조설비(HVAC), HEPA/ULPA 필터, 층류 공기 시스템, 실시간 환경 모니터링에 대한 투자가 미국 시장의 주요 성장 요인으로 작용하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 장비별, 2022-2035

제6장 시장 추정 및 예측 : 클린룸 종류별, 2022-2035

제7장 시장 추정 및 예측 : 클린룸 분류별, 2022-2035

제8장 시장 추정 및 예측 : 용도별, 2022-2035

제9장 시장 추정 및 예측 : 유통 채널별, 2022-2035

제10장 시장 추정 및 예측 : 지역별, 2022-2035

제11장 기업 개요

KSM 26.03.05The Global Cleanroom Equipment Market was valued at USD 5.6 billion in 2025 and is estimated to grow at a CAGR of 7.5% to reach USD 10.8 billion by 2035.

The market is witnessing rapid growth due to the worldwide expansion of pharmaceutical, biotechnology, and advanced therapy manufacturing. The increasing production of sterile injectables, biologics, vaccines, personalized medicines, and cell and gene therapies has created significant demand for controlled manufacturing environments. These production spaces require state-of-the-art HVAC systems, HEPA and ULPA filtration, advanced air handling units, and continuous environmental monitoring. Another key factor fueling growth is the rising adoption of modular and flexible cleanroom solutions. Manufacturers prefer modular cleanrooms for their lower installation costs, rapid deployment, and ability to scale production spaces according to evolving regulatory or production demands. The flexibility to quickly expand or reconfigure cleanroom layouts to meet increasing output requirements or regulatory compliance is driving strong adoption globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.6 Billion |

| Forecast Value | $10.8 Billion |

| CAGR | 7.5% |

The air filters segment generated USD 1.7 billion in 2025 and is anticipated to grow at a CAGR of 7.7% from 2026 to 2035. Stringent contamination control regulations in pharmaceuticals, biotechnology, semiconductor manufacturing, and healthcare industries are driving demand for high-efficiency HEPA and ULPA filtration. Industries producing sensitive electronics, nanotechnology components, and medical devices require ultra-clean air environments, fueling the need for advanced filtration solutions in both new cleanroom installations and retrofitted facilities.

The direct sales segment held a 67.7% share in 2025 and is expected to grow at a CAGR of 7.2% through 2035. Direct sales allow companies to provide customized solutions such as specialized air handling units, integrated laminar flow systems, and automation with real-time monitoring. This approach ensures compliance with GMP, FDA, EMA, ISO, and industry-specific standards while providing complete documentation, validation, and qualification from a single source. OEMs support customers throughout design, installation, commissioning, and lifecycle maintenance, minimizing contamination risks and downtime in mission-critical cleanroom operations.

U.S. Cleanroom Equipment Market reached USD 1.5 billion in 2025 and is expected to grow at a CAGR of 7.2% from 2026 to 2035. The country's robust pharmaceutical and biotechnology sectors, including biologics, vaccines, sterile injectables, and advanced therapies, drive consistent demand for cleanroom equipment. Increasing reliance on contract development and manufacturing organizations (CDMOs) has accelerated the establishment of multi-product, flexible cleanroom facilities, further supporting market expansion. Investments in advanced HVAC, HEPA/ULPA filtration, laminar airflow systems, and real-time environmental monitoring are key growth drivers in the U.S.

Key players shaping the Global Cleanroom Equipment Market include Abtech, Airomax Airborne LLP, Alpiq Holding AG, Angstrom Technology, Ardmac Ltd., Azbil Corporation, Camfil AB Source, Clean Air Products, HVAX, Illinois Tool Works Inc., Integrated Cleanroom Technologies Pvt. Ltd., Kimberly-Clark Corporation, Labconco, M + W Group, Taikisha Ltd., and Terra Universal Inc. Companies in the cleanroom equipment market strengthen their presence by focusing on product innovation, regulatory compliance, and turnkey solutions. Providers develop modular, scalable, and energy-efficient cleanroom systems to meet evolving industry needs. Strategic collaborations with pharmaceutical, biotech, and semiconductor manufacturers allow co-development of customized solutions. Expanding distribution networks across emerging and established markets improves accessibility, while strong after-sales and maintenance services reinforce customer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment

- 2.2.3 Type of cleanroom

- 2.2.4 Cleanroom classification

- 2.2.5 Application

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expanding pharmaceutical & biotechnology manufacturing

- 3.2.1.2 Adoption of modular & flexible cleanroom solutions

- 3.2.1.3 Stringent regulatory & quality compliance requirements

- 3.2.1.4 Increasing focus on infection control in healthcare facilities

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital expenditure & operating costs

- 3.2.2.2 Energy consumption & sustainability constraints

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Air showers

- 5.3 Air filters

- 5.3.1 HEPA filter

- 5.3.2 ULPA filter

- 5.3.3 Fan filter unit

- 5.3.4 Ceiling HEPA filter AC unit

- 5.4 Laminar flow hood

- 5.4.1 Horizontal laminar flow hood

- 5.4.2 Vertical laminar flow hood

- 5.5 Desiccator cabinet

- 5.5.1 Stainless steel desiccator cabinet

- 5.5.2 Acrylic desiccator cabinet

- 5.6 Pass through

- 5.7 Chemical fume hood

- 5.8 Cleanroom doors

- 5.8.1 Roll up doors

- 5.8.2 Automatic sliding doors

- 5.9 Others (sink, bench, door interlock system, etc.)

Chapter 6 Market Estimates & Forecast, By Type of Cleanroom, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Traditional cleanroom

- 6.3 Modular cleanroom

- 6.4 Modular softwall cleanrooms

- 6.5 Mobile cleanrooms

- 6.6 Hybrid cleanrooms

Chapter 7 Market Estimates & Forecast, By Cleanroom Classification, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 ISO Class 1-3

- 7.3 ISO Class 4-5

- 7.4 ISO Class 6-7

- 7.5 ISO Class 8-9

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Pharmaceutical

- 8.3 Semiconductors

- 8.4 Biotechnology

- 8.5 Hospital

- 8.6 Aerospace

- 8.7 Automotive

- 8.8 Others (Life sciences, Military facilities, Research laboratories, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Abtech

- 11.2 Airomax Airborne LLP

- 11.3 Alpiq holding AG

- 11.4 Angstrom Technology

- 11.5 Ardmac Ltd.

- 11.6 Azbil Corporation

- 11.7 Camfil AB Source

- 11.8 Clean Air Products

- 11.9 HVAX

- 11.10 Illinois Tool Works Inc.

- 11.11 Integrated Cleanroom Technologies Pvt. Ltd.

- 11.12 Kimberly-Clark Corporation

- 11.13 Labconco

- 11.14 M + W Group

- 11.15 Taikisha Ltd.

- 11.16 Terra Universal Inc.