|

시장보고서

상품코드

1936616

형광 안료 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Phosphorescent Pigments Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

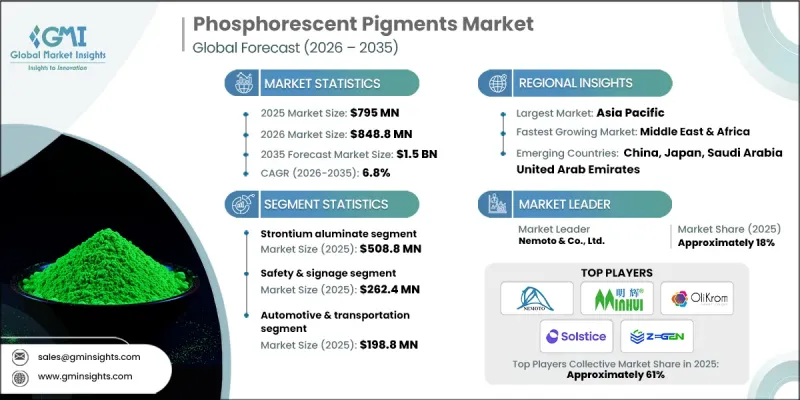

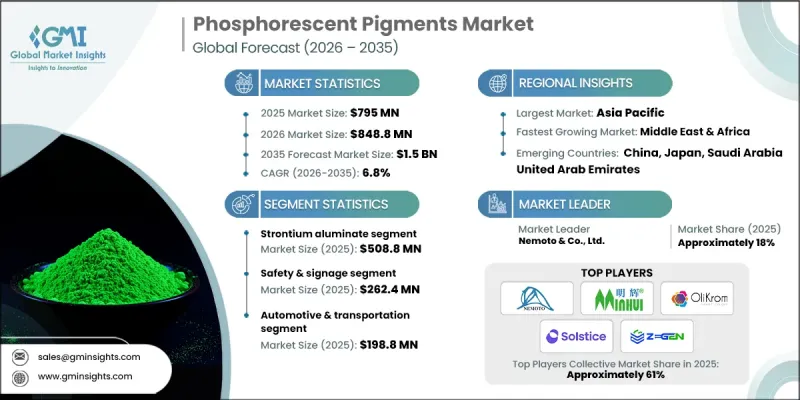

세계의 형광 안료 시장은 2025년에 7억 9,500만 달러로 평가되었으며, 2035년까지 CAGR 6.8%로 성장하여 15억 달러에 달할 것으로 예측됩니다.

시장 성장은 상업용 건물, 공공 인프라, 교통 시설, 산업 환경 등 안전성을 중시하는 응용 분야에서 축광성 소재의 채택이 확대되고 있는 데 따른 것입니다. 정전 시에도 안정적인 조명을 제공하는 축광 소재에 대한 수요는 비상시 대응과 가시성에 대한 중요성이 높아지면서 지속적으로 증가하고 있습니다. 건축물의 안전 및 화재 예방에 관한 규제 프레임워크는 전력이 필요 없이 작동하는 가시광선 유도 시스템 설치를 의무화함으로써 안정적인 수요를 강화하고 있습니다. 안료 기술의 지속적인 발전은 밝기 강도, 발광 지속 시간, 환경 스트레스에 대한 내성을 향상시킴으로써 시장 확대를 더욱 가속화하고 있습니다. 재료 성능의 향상으로 코팅, 엔지니어링 플라스틱, 특수 소재 등에서의 응용 분야가 확대되어 제조업체는 보다 고부가가치 응용 분야를 공략할 수 있게 되었습니다. 지속적인 기술 혁신을 통해 고온, 습기, 자외선에 대한 내구성이 향상되어 장기적인 성능을 지원합니다. 안전 기준의 발전과 세계 인프라 투자 증가에 따라 형광 안료는 가시성을 중시하는 응용 분야에서 필수적인 구성요소로 남아 있으며, 시장의 꾸준한 성장세를 유지하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 7억 9,500만 달러 |

| 예측 금액 | 15억 달러 |

| CAGR | 6.8% |

스트론튬 알루미네이트 안료 부문은 2025년 5억 8,800만 달러에 달했습니다. 이 안료는 우수한 발광성, 장시간의 잔광 지속성 및 향상된 에너지 흡수 효율로 인해 전 세계 수요를 지배하고 있습니다. 이러한 성능적 우위를 바탕으로 장기간의 가시성이 요구되는 애플리케이션에서 선호되는 솔루션으로 자리매김하고 있습니다. 이러한 안료의 무해한 성분은 특히 엄격한 안전 기준을 준수해야 하는 건설 및 운송 환경과 같은 규제 산업 전반에서 폭넓게 수용되고 있습니다.

안전 및 표지판 분야는 2025년 2억 6,240만 달러를 차지했으며, 시장에서 가장 중요한 응용 분야 중 하나입니다. 이러한 용도에서는 외부 전원이 필요 없는 비상시 가시성 유지에 인광 안료가 활용되고 있습니다. 작업장 안전, 비상사태 대응, 건축 기준 준수에 대한 관심이 높아지면서 상업, 산업, 공공시설의 안정적인 수요를 견인하고 있습니다. 인프라 구축의 진전은 이 분야가 전체 시장 성장에 기여하는 정도를 더욱 강화시키고 있습니다.

북미 형광 안료 시장은 2025년 1억 7,490만 달러 규모에 달했으며, 예측 기간 동안 매력적인 성장세를 보일 것으로 예상됩니다. 안전 기준 준수와 인프라 내결함성에 대한 강력한 규제 집행이 지역 수요의 지속을 뒷받침하고 있습니다. 상업용 건축 및 교통 시설에 대한 지속적인 투자가 다양한 응용 분야에서 발광 재료의 채택을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품 유형별, 2022-2035

제6장 시장 추정 및 예측 : 용도별, 2022-2035

제7장 시장 추정 및 예측 : 최종 이용 산업별, 2022-2035

제8장 시장 추정 및 예측 : 지역별, 2022-2035

제9장 기업 개요

KSM 26.03.05The Global Phosphorescent Pigments Market was valued at USD 795 million in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 1.5 billion by 2035.

Market growth is supported by rising adoption of photoluminescent materials in safety-focused applications across commercial buildings, public infrastructure, transportation facilities, and industrial environments. Increasing emphasis on emergency preparedness and visibility continues to drive demand, as phosphorescent materials provide reliable illumination during power interruptions. Regulatory frameworks related to building safety and fire protection have reinforced consistent consumption by mandating visible guidance systems that function without electricity. Ongoing advancements in pigment technology are further accelerating market expansion by improving brightness intensity, glow duration, and resistance to environmental stress. Enhanced material performance has broadened usage across coatings, engineered plastics, and specialty materials, enabling manufacturers to target higher-value applications. Continuous innovation has improved durability under exposure to heat, moisture, and ultraviolet conditions, supporting long-term performance. As safety standards evolve and infrastructure investment increases globally, phosphorescent pigments remain essential components in visibility-driven applications, sustaining steady market momentum.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $795 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 6.8% |

The strontium aluminate-based pigments segment reached USD 508.8 million in 2025. These pigments dominate global demand due to their superior luminosity, extended afterglow duration, and enhanced energy absorption efficiency. Their performance advantages have positioned them as preferred solutions for applications requiring long-lasting visibility. The non-hazardous composition of these pigments further supports widespread acceptance across regulated industries, particularly in construction and transportation environments that require compliance with strict safety standards.

The safety and signage segment accounted for USD 262.4 million in 2025, representing one of the most substantial usage segments within the market. These applications rely on phosphorescent pigments to maintain visibility in emergency situations without external power sources. Growing focus on workplace safety, emergency preparedness, and building compliance continues to drive steady demand across commercial, industrial, and public settings. Increased infrastructure development further strengthens this segment's contribution to overall market growth.

North America Phosphorescent Pigments Market generated USD 174.9 million in 2025 and is expected to witness attractive growth throughout the forecast period. Strong regulatory enforcement related to safety compliance and infrastructure resilience supports sustained regional demand. Ongoing investments in commercial construction and transportation facilities reinforce the adoption of photoluminescent materials across multiple applications.

Key companies operating in the Global Phosphorescent Pigments Market include Nemoto & Co., Ltd., Zegen Advanced Materials, United Mineral and Chemical Corp., RTP Company, Lumentics, Stanford Advanced Materials, iSuoChem, OliKrom, Techno Glow Inc, Badger Color Concentrates, Inc, Zhejiang Minhui Luminous Technology Co., Ltd, Vishnu Priya Chemicals Pvt Ltd, Chemical Bull, AB Enterprises, Lab Alley, SINO SUNMAN INTERNATIONAL, and Solstice Advanced Materials Inc. Companies in the phosphorescent pigments market strengthen their competitive position through continuous material innovation, capacity expansion, and application-focused product development. Manufacturers invest heavily in research to enhance glow efficiency, durability, and environmental stability. Strategic partnerships with coatings, plastics, and construction material suppliers support wider adoption. Portfolio diversification across industrial, commercial, and infrastructure applications improves revenue resilience.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 End use industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand in safety & emergency signage

- 3.2.1.2 Technological advancements in pigment performance

- 3.2.1.3 Expansion in consumer goods & decorative applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Performance degradation under certain conditions

- 3.2.2.2 Regulatory & environmental challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in smart infrastructure & urban development

- 3.2.3.2 Eco-friendly & energy-saving solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Strontium aluminate

- 5.3 Zinc sulfide

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Coatings & paints

- 6.3 Plastics & polymers

- 6.4 Printing inks

- 6.4.1 Security printing

- 6.4.2 Decorative

- 6.5 Safety & signage

- 6.5.1 Emergency exit signs

- 6.5.2 Road marking

- 6.6 Consumer electronics

- 6.6.1 Display backlighting

- 6.6.2 Wearables

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive & transportation

- 7.3 Aerospace & defense

- 7.4 Packaging

- 7.5 Textiles

- 7.6 Construction

- 7.7 Marine

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Nemoto & Co., Ltd.

- 9.2 United Mineral and Chemical Corp.

- 9.3 Zegen Advanced Materials

- 9.4 Lumentics

- 9.5 iSuoChem

- 9.6 OliKrom

- 9.7 Lab Alley

- 9.8 RTP Company

- 9.9 Badger Color Concentrates, Inc

- 9.10 Techno Glow Inc

- 9.11 Vishnu Priya Chemicals Pvt Ltd

- 9.12 Chemical Bull

- 9.13 Zhejiang Minhui Luminous Technology Co., Ltd

- 9.14 AB Enterprises

- 9.15 Stanford Advanced Materials

- 9.16 SINO SUNMAN INTERNATIONAL

- 9.17 Solstice Advanced Materials Inc.