|

시장보고서

상품코드

1936623

젖산 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Lactic Acid Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

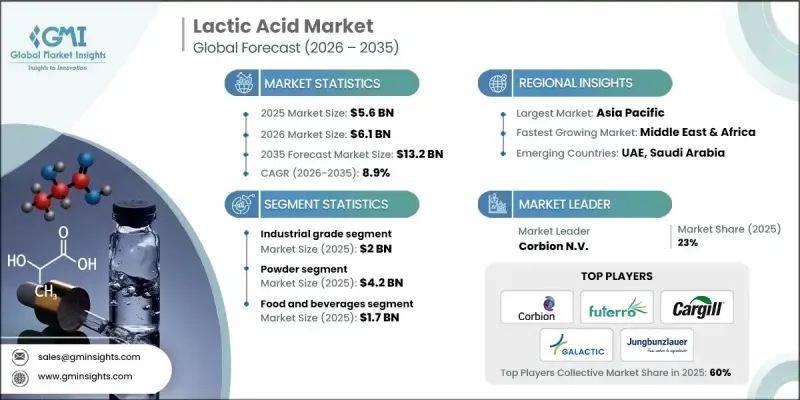

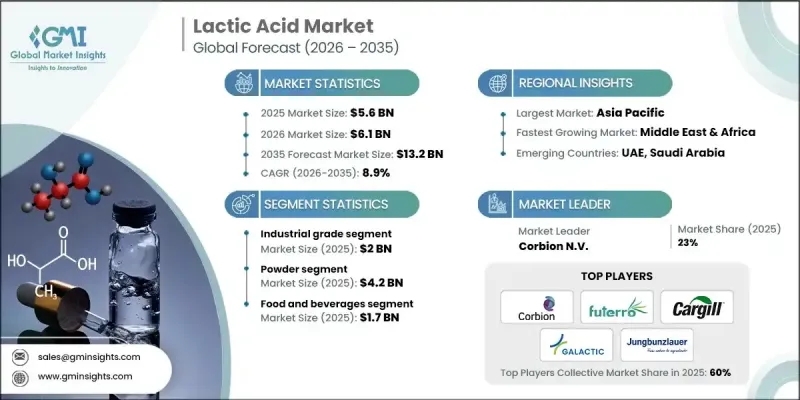

세계의 젖산 시장은 2025년에 56억 달러로 평가되었으며, 2035년까지 CAGR 8.9%로 성장하여 132억 달러에 달할 것으로 예측됩니다.

시장 확대의 배경에는 바이오 기반 폴리머, 특히 폴리락트산(PLA)의 핵심 원료로서 젖산의 중요성이 커지고 있다는 점을 들 수 있습니다. 환경 규제 강화와 기업의 지속가능성에 대한 노력은 포장, 소비재, 산업 분야에서 기존 플라스틱에서 생분해성 대체품으로의 전환을 가속화하고 있습니다. 전통적인 식품 용도 외에도 젖산은 대량 생산되는 산업 응용 분야에서도 점점 더 많이 채택되어 시장의 꾸준한 성장을 뒷받침하고 있습니다. 또한, 자동차, 항공우주 등의 분야에서도 수요가 촉진되고 있습니다. 각 제조사들이 연비 향상과 배기가스 배출량 감소를 위해 가볍고 지속가능한 소재를 찾고 있기 때문입니다. 젖산 유도체는 경량화 및 환경 적합성이 중요한 내장재, 복합재료 블렌드, 비구조용 재료에서 더욱 널리 사용되고 있습니다. 이러한 고급 용도의 점진적인 도입은 전체 산업에서 젖산의 장기적인 전망을 강화하고 있습니다. 발효기술과 고분자 가공기술의 발전, 그리고 전 세계적인 바이오 기반 소재에 대한 관심은 그 시장 가능성을 더욱 높여주고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 56억 달러 |

| 예측 금액 | 132억 달러 |

| CAGR | 8.9% |

산업용 젖산 부문은 2025년 20억 달러를 차지했습니다. 바이오플라스틱, 화학 중간체, 용제, 산업 공정에서 폭넓게 사용되고 있으며, 높은 생산량과 비용 효율성이 그 장점으로 꼽힙니다. 산업용 젖산은 대규모 발효 및 폴리머 생산에 적합하며, 전 세계 포장재, 특수 화학제품 및 바이오폴리머 제조업체가 선호하는 선택입니다.

물리적 형태에 따라 분말 부문은 2025년 42억 달러에 달했습니다. 분말 젖산은 높은 안정성, 장기보관성, 보관의 용이성, 운송의 편리성으로 인해 선호되고 있습니다. 정확한 복용량, 낮은 취급 위험, 건조 혼합물과의 호환성이 중요한 식품 가공, 의약품, 산업용 배합제에서 널리 사용됩니다. 벌크 관리와 광범위한 유통 네트워크에 대한 적합성은 세계 공급망에서 주요한 형태로서의 지위를 더욱 강화하고 있습니다.

북미 젖산 시장은 2025년 14억 달러 규모에 달했습니다. 미국은 선진적인 발효 인프라와 바이오플라스틱, 식음료, 의약품, 퍼스널케어 제품에 대한 높은 수요에 힘입어 세계 젖산 시장의 약 25%를 차지하고 있습니다. 풍부한 원료 공급원, 첨단 바이오 공정 기술, 확립된 산업 소비 패턴이 이 지역의 시장 리더십을 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 등급별, 2022-2035

제6장 시장 추정 및 예측 : 물리 형태별, 2022-2035

제7장 시장 추정 및 예측 : 용도별, 2022-2035

제8장 시장 추정 및 예측 : 지역별, 2022-2035

제9장 기업 개요

KSM 26.03.05The Global Lactic Acid Market was valued at USD 5.6 billion in 2025 and is estimated to grow at a CAGR of 8.9% to reach USD 13.2 billion by 2035.

Market expansion is driven by the growing importance of lactic acid as a core raw material for bio-based polymers, particularly polylactic acid (PLA). Increasing environmental regulations and corporate sustainability commitments are accelerating the shift from conventional plastics to biodegradable alternatives across packaging, consumer goods, and industrial applications. Beyond traditional food use, lactic acid is increasingly incorporated into high-volume industrial applications, maintaining steady market growth. Additionally, sectors like automotive and aerospace are stimulating demand, as manufacturers seek lightweight and sustainable materials to improve fuel efficiency and reduce emissions. Lactic acid derivatives are finding wider adoption in interior components, composite blends, and non-structural materials, where weight reduction and ecological compliance are crucial. This gradual incorporation into high-end applications strengthens the long-term outlook for lactic acid across industries. Technological advancements in fermentation and polymer processing, along with global emphasis on bio-based materials, continue to reinforce its market potential.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.6 Billion |

| Forecast Value | $13.2 Billion |

| CAGR | 8.9% |

The industrial-grade lactic acid segment accounted for USD 2 billion in 2025. Its dominance stems from broad applications in bioplastics, chemical intermediates, solvents, and industrial processing, coupled with high production volumes and cost-effectiveness. Industrial-grade lactic acid is ideal for large-scale fermentation and polymer manufacturing, making it the preferred choice for packaging, specialty chemicals, and biopolymer producers worldwide.

By physical form, the powder segment reached USD 4.2 billion in 2025. Powdered lactic acid is favored for its high stability, long shelf life, easy storage, and convenient transportation. It is widely used in food processing, pharmaceuticals, and industrial formulations where precise dosing, low handling risk, and compatibility with dry blends are critical. Its suitability for bulk management and broad distribution networks further reinforces its position as the dominant form in global supply chains.

North America Lactic Acid Market captured USD 1.4 billion in 2025. The U.S. accounted for roughly 25% of the global lactic acid market, driven by its advanced fermentation infrastructure and high demand for bioplastics, food and beverage applications, pharmaceuticals, and personal care products. The availability of abundant feedstock, sophisticated bioprocessing capabilities, and established industrial consumption patterns support the region's market leadership.

Key companies operating in the Global Lactic Acid Market include Arkema, Corbion N.V., BASF SE, DSM-Firmenich, Evonik Industries, Cargill Incorporated, Galactic, JIAAN BIOTECH, Jungbunzlauer Suisse AG, TEIJIN LIMITED, Musashino Chemical (China) Co., Ltd., Futerro, DOW, and NatureWorks LLC. Leading players in the lactic acid market are strengthening their positions through strategies such as expanding production capacity, improving fermentation technologies, and diversifying into high-value biopolymer derivatives. Companies are investing in research and development to enhance purity, yield, and bio-based product integration. Strategic partnerships and acquisitions allow firms to extend regional footprints and secure raw material supply chains. Focus on sustainable and cost-effective production processes, as well as product innovation for industrial, pharmaceutical, and food-grade applications, enables these companies to maintain competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Grade

- 2.2.3 Physical Form

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for natural & clean-label food preservatives

- 3.2.1.2 Consumer shift away from synthetic additives

- 3.2.1. 3 Growing bioplastics market & circular economy initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Slow degradation in ambient conditions

- 3.2.2.2 Limited industrial composting infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Lignocellulosic & non-food feedstock development

- 3.2.3.2 Greenhouse gas-to-lactic acid technology

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Grade, 2022 - 2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Food grade

- 5.3 Industrial grade

- 5.4 Pharmaceutical grade

- 5.5 Technical grade

- 5.6 Cosmetic grade

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Physical Form, 2022 - 2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder

- 6.3 Liquid

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Polyamides & nylons

- 7.3 Plasticizers

- 7.4 Lubricants & greases

- 7.4.1 Synthetic lubricants

- 7.4.2 Complex greases

- 7.4.3 Metalworking fluids

- 7.5 Cosmetics & personal care

- 7.6 Adhesives & sealants

- 7.7 Coatings & paints

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Corbion N.V.

- 9.2 Arkema

- 9.3 BASF SE

- 9.4 DSM-Firmenich

- 9.5 Evonik Industries

- 9.6 JIAAN BIOTECH

- 9.7 Galactic

- 9.8 Jungbunzlauer Suisse AG, Basel

- 9.9 Cargill Incorporated

- 9.10 TEIJIN LIMITED

- 9.11 Musashino Chemical (China) Co., Ltd.

- 9.12 Futerro

- 9.13 DOW

- 9.14 NatureWorks LLC