|

시장보고서

상품코드

1936626

설폰계 폴리머 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Sulfone Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

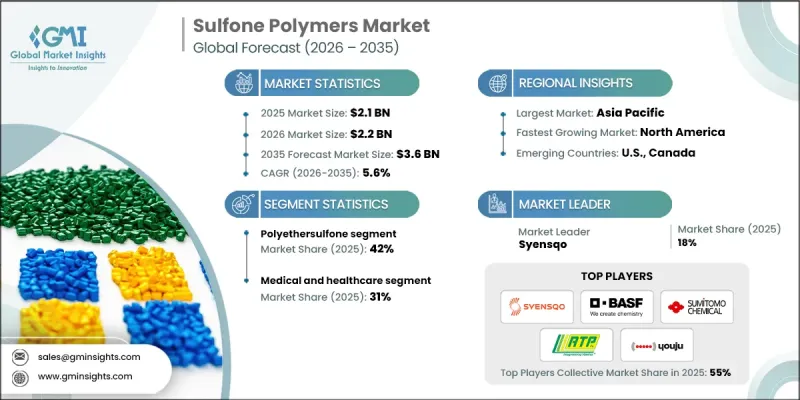

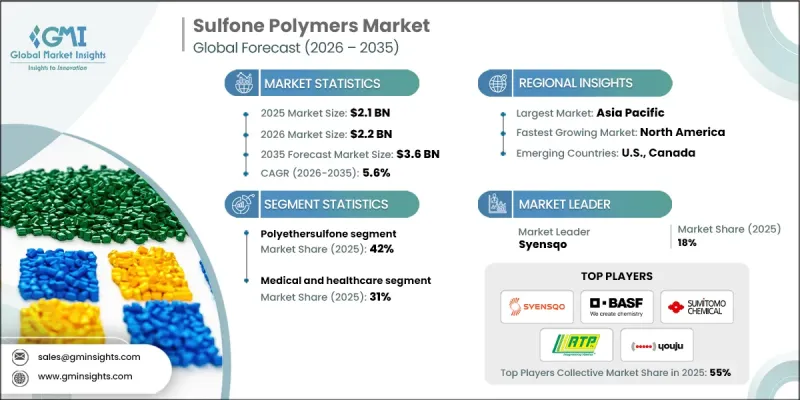

세계의 설폰계 폴리머 시장은 2025년에 21억 달러로 평가되었으며, 2035년까지 CAGR 5.6%로 성장하여 36억 달러에 달할 것으로 예측됩니다.

이 시장에는 버진 펠릿, 멤브레인 등급 분말, 화합물 제제로 제공되는 폴리설폰(PSU), 폴리에테르설폰(PESU), 폴리페닐설폰(PPSU), 폴리에테르이미드(PEI)의 수익이 포함됩니다. 가격 체계는 분자량 분포, 재료 순도, 멸균 인증, 난연 등급, 식품 및 물 접촉 승인 등의 요인에 따라 영향을 받으며, 특수 등급의 경우 20-40%의 프리미엄 가격이 책정될 수 있습니다. 의료용 및 멤브레인 응용 분야에 대한 수요가 약간만 이동해도 이들 등급의 고부가가치 특성으로 인해 수익에 불균형적인 영향을 미칠 수 있습니다. 의료 분야에서는 생체적합성, 멸균 내구성, 장수명 성능이 구매자의 우선 순위이며, PPSU 의료 부품은 여러 번의 증기 멸균 사이클을 견딜 수 있습니다. 수처리 분야에서는 플럭스 효율과 파울링 회수율을 포함한 막 성능이 매우 중요한데, PES계 막은 세정 후 빠른 회복과 함께 높은 처리량을 자랑합니다. 전자기기 및 항공우주 분야에서는 높은 유리 전이 온도, 치수 안정성, 내열 변형 온도가 가혹한 환경에서의 중요 용도를 지원하여 안정적인 수요와 높은 단가를 견인하고 있습니다. 고성능 재료 특성과 엄격한 규제 기준을 충족할 수 있는 능력이 결합되어 여러 산업 분야에 걸쳐 세계 시장 확대를 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 21억 달러 |

| 예측 금액 | 36억 달러 |

| CAGR | 5.6% |

폴리에테르 설폰(PESU) 부문은 2025년 42%의 점유율을 차지했습니다. PESU는 친수성, 우수한 내화학성, 220℃까지의 열 안정성을 겸비한 균형 잡힌 특성과 비용 비율로 인해 PESU는 물 여과, 혈액투석, 산업용 분리막에 매우 적합합니다. 분자량 45,000-68,000 범위의 PESU 상용 분말은 용해성과 막 제조의 용이성을 고려하여 설계되었습니다.

전자 및 전기 응용 분야는 2025년 22%의 점유율을 차지할 것으로 예상되며, 설폰계 폴리머의 열 안정성, 내화학성, 정밀한 치수 제어를 활용하고 있습니다. 이러한 소재는 고온 환경에서의 전자부품, 절연 모듈, 높은 화학제품 노출 환경에서도 공차 유지가 요구되는 어셈블리 용도로 점점 더 많이 채택되고 있습니다. 투명성과 자외선 안정성을 갖춘 등급은 장기적인 신뢰성과 열 열화 저항성이 필수적인 조명 응용 분야에서도 선호되고 있습니다. 설폰 폴리머의 범용성과 가혹한 작동 환경에서의 성능은 다양한 산업 분야에서 지속적으로 채택을 강화하고 있습니다.

북미 설폰계 폴리머 시장은 2025년 27%의 점유율을 차지했습니다. 이러한 강력한 지역 수요는 첨단 의료기기 제조, 엄격한 의료 품질 기준, 견조한 항공우주 부문에 의해 주도되고 있습니다. 의료용 FDA 승인 및 ASTM 표준을 포함한 규제 프레임워크는 중요한 기기에 설폰계 폴리머의 사용을 촉진하고 있습니다. 폐기물을 줄이고 시술 당 비용을 절감하기 위한 재사용 가능한 의료기기에 대한 관심은 PSU와 PPSU와 같은 내멸균성 소재의 매력을 더욱 높이고 있습니다. 또한, 광범위한 공급망과 대규모 산업 기반에 힘입어 미국과 캐나다에 집중된 항공우주 제조도 항공우주 등급 설폰계 폴리머에 대한 수요를 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 제품별, 2022-2035

제6장 시장 규모 및 예측 : 성능 등급별, 2022-2035

제7장 시장 규모 및 예측 : 최종 이용 산업별, 2022-2035

제8장 시장 규모 및 예측 : 지역별, 2022-2035

제9장 기업 개요

KSM 26.03.05The Global Sulfone Polymers Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 3.6 billion by 2035.

The market includes revenue generated from polysulfone (PSU), polyethersulfone (PESU), polyphenylsulfone (PPSU), and polyetherimide (PEI), offered as virgin pellets, membrane-grade powders, and compounded formulations. Pricing structures are influenced by factors such as molecular weight distribution, material purity, sterilization certifications, flame-retardant ratings, and approvals for food and water contact, which can command 20-40% premiums for specialized grades. Even small shifts in volume toward healthcare or membrane applications can have a disproportionate impact on revenue due to the high-value nature of these grades. In the healthcare sector, buyers prioritize biocompatibility, sterilization durability, and long lifecycle performance, which allow PPSU medical components to withstand multiple steam cycles. In water treatment, membrane performance, including flux efficiency and fouling recovery, is critical, and PES-based membranes have demonstrated high throughput with rapid recovery after cleaning. In electronics and aerospace, high glass transition temperatures, dimensional stability, and heat deflection capabilities support critical applications under extreme conditions, driving consistent demand and higher per-unit revenue. The combination of high-performance material properties and the ability to meet stringent regulatory standards is fueling global market expansion across multiple industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 5.6% |

The polyethersulfone segment held 42% share in 2025. Its balanced property-to-cost ratio, combined with hydrophilic behavior, excellent chemical resistance, and thermal stability up to 220°C, makes PESU highly suitable for water filtration, hemodialysis, and industrial separation membranes. Commercial powders of PESU, with molecular weights ranging from 45,000 to 68,000, are designed for ease of dissolution and membrane fabrication.

The electronics and electrical applications segment held 22% share in 2025, leveraging sulfone polymers' thermal stability, chemical resistance, and precise dimensional control. These materials are increasingly used in high-temperature electronic components, insulating modules, and assemblies where chemical exposure is high, but tolerances must be maintained. Transparent and UV-stable grades are also favored in lighting applications where long-term reliability and resistance to heat degradation are essential. The versatility of sulfone polymers, coupled with their performance in demanding operating environments, continues to reinforce their adoption across diverse industrial applications.

North America Sulfone Polymers Market represented 27% share in 2025. The strong regional demand is driven by advanced medical device manufacturing, strict healthcare quality standards, and a robust aerospace sector. Regulatory frameworks, including FDA recognition and ASTM standards for medical applications, support the use of sulfone polymers for critical devices. Emphasis on reusable medical devices to reduce waste and per-procedure costs further enhances the appeal of sterilization-resistant materials such as PSU and PPSU. The concentration of aerospace manufacturing in the U.S. and Canada, supported by extensive supply chains and large-scale industrial operations, also fuels demand for aerospace-grade sulfone polymers.

Key players operating in the Global Sulfone Polymers Market include Shandong Haoran Special Plastic, Mitsubishi Gas Chemical Company, RTP Company, Sumitomo Chemical, BASF SE, SABIC, Youju New Materials, Syensqo, Atul Ltd, and Solvay. To strengthen their presence, companies in the sulfone polymers industry are adopting multiple strategic initiatives. They are investing heavily in research and development to produce polymers with superior thermal, chemical, and sterilization performance, tailored for healthcare, aerospace, and membrane applications. Strategic collaborations, joint ventures, and mergers allow firms to expand their geographical footprint, access new customer segments, and improve supply chain efficiency. Many companies are optimizing production processes to reduce costs while enhancing material purity and performance. Firms are also focusing on regulatory compliance, obtaining medical and industrial certifications to improve credibility and customer trust. Advanced digital platforms for material testing, real-time quality monitoring, and customer support further enhance operational efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product

- 2.2.2 Performance grade

- 2.2.3 End use industry

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Product, 2022-2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Polysulfone (PSU)

- 5.3 Polyethersulfone (PESU)

- 5.4 Polyphenylsulfone (PPSU)

- 5.5 Polyetherimide (PEI)

- 5.6 Others

Chapter 6 Market Size and Forecast, By Performance Grade, 2022-2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Standard/commercial grade

- 6.3 Medical/healthcare grade

- 6.4 Food contact grade

- 6.5 Aerospace grade

- 6.6 Flame retardant grade

- 6.7 Others

Chapter 7 Market Size and Forecast, By End Use Industry , 2022-2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Medical & healthcare

- 7.2.1 Hospitals & dialysis centers

- 7.2.2 Medical device manufacturers

- 7.2.3 Pharmaceutical processing equipment

- 7.3 Aerospace

- 7.3.1 Commercial aviation

- 7.3.2 Military & defense aircraft

- 7.3.3 Space applications

- 7.4 Automotive

- 7.4.1 Internal combustion engine (ICE) vehicles

- 7.4.2 Electric vehicles (EVs)

- 7.4.3 Hybrid vehicles

- 7.5 Electrical & electronics

- 7.5.1 Consumer electronics

- 7.5.2 Semiconductor manufacturing

- 7.5.3 Data centers & servers

- 7.5.4 5g infrastructure

- 7.6 Water & wastewater treatment

- 7.6.1 Municipal utilities

- 7.6.2 Industrial water treatment

- 7.6.3 Desalination plants

- 7.7 Food & beverage processing

- 7.7.1 Food processing equipment manufacturers

- 7.7.2 Commercial kitchens & restaurants

- 7.7.3 Household appliances

- 7.8 Industrial & manufacturing

- 7.8.1 Plumbing & HVAC

- 7.8.2 Chemical processing equipment

- 7.8.3 Oil & gas applications

- 7.9 Energy & hydrogen economy

- 7.9.1 Fuel cell manufacturers

- 7.9.2 Electrolyzer manufacturers

- 7.9.3 Hydrogen infrastructure development

- 7.10 Others

Chapter 8 Market Size and Forecast, By Region, 2022-2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 RTP Company

- 9.2 Youju New Materials

- 9.3 BASF SE

- 9.4 SABIC

- 9.5 Solvay

- 9.6 Sumitomo Chemical

- 9.7 Shandong Haoran Special Plastic

- 9.8 Syensqo

- 9.9 Mitsubishi Gas Chemical Company

- 9.10 Atul Ltd

- 9.11 Avient Corporation

- 9.12 Ovation Polymers

- 9.13 ASEP Industries Sdn Bhd

- 9.14 Aurorium

- 9.15 3DXTech

- 9.16 Foshan Plolima Material