|

시장보고서

상품코드

1936632

패혈증 진단 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Sepsis Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

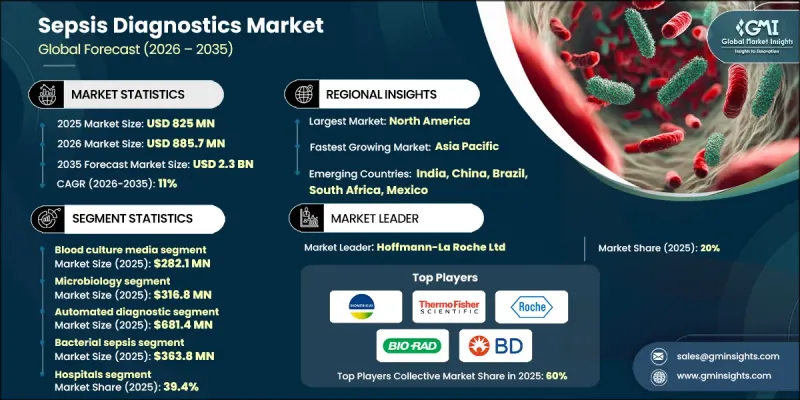

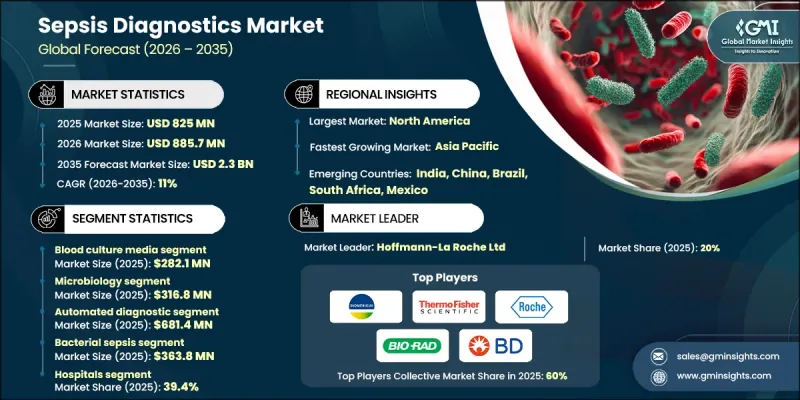

세계의 패혈증 진단 시장은 2025년에 8억 2,500만 달러로 평가되었으며, 2035년까지 CAGR 11%로 성장하여 23억 달러에 달할 것으로 예측됩니다.

이러한 성장은 감염병 발생률 증가, 공공 부문의 감염 관리에 대한 관심 증가, 진단 기술의 지속적인 발전으로 뒷받침되고 있습니다. 임상의와 환자의 적시 진단의 중요성에 대한 인식이 높아지면서 시장 수요가 더욱 강화되고 있습니다. 항균제 내성, 병원내 감염, 만성질환의 유병률 증가 등의 요인으로 인해 패혈증 위험이 지속적으로 증가하고 있으며, 특히 노인과 면역저하 환자에서 패혈증 위험이 증가하고 있습니다. 의료 서비스 제공자들은 생존율을 높이고 치료 비용을 효율적으로 관리하기 위해 신속하고 정확한 진단 솔루션을 점점 더 우선순위에 두고 있습니다. 조기 발견이 임상 결과 개선의 핵심인 만큼, 현장 진단 및 신속 진단 도구에 대한 수요 증가는 혁신과 세계 시장 확대에 유리한 조건을 조성하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 8억 2,500만 달러 |

| 예측 금액 | 23억 달러 |

| CAGR | 11% |

공공 보건 인프라에 대한 정부 주도의 투자가 시장 성장을 가속화하고 있습니다. 패혈증은 감염의 진행과 밀접한 관련이 있기 때문에 조기 발견이 공중보건의 최우선 과제입니다. 각국의 의료 프로그램에서는 진단 체계의 정비, 검사 능력의 강화, 임상적 판단의 신속성을 점점 더 중요시하고 있습니다. 이러한 노력은 첨단 진단 플랫폼의 보급을 촉진하고 병원 및 검사 시설의 수요를 강화하는 데 기여하고 있습니다.

혈액 배양 배지 부문은 2025년 2억 8,210만 달러의 시장 규모를 기록했습니다. 이 제품들은 혈액 샘플에서 미생물 증식을 촉진하도록 설계되어 혈류 감염을 감지할 수 있습니다. 자동 진단 시스템과의 호환성 및 임상 검사실에서의 일관된 사용은 안정적인 수요를 보장합니다. 감염 확인에 중요한 역할을 하는 혈액 배양 배지는 패혈증 진단의 핵심 요소로 남아 있습니다.

미생물학 기반 진단 부문은 2025년 3억 1,680만 달러를 차지했습니다. 이 방법은 환자 검체에서 병원균의 배양 및 동정에 초점을 맞추고 있으며, 임상 현장에서 널리 받아들여지고 있습니다. 상세한 미생물 동정 및 항균제 감수성 검사를 지원하여 효과적인 치료 방침을 결정하고 환자 관리를 개선하는 데 필수적입니다.

미국 패혈증 진단 시장은 2025년 2억 8,370만 달러로 평가됐습니다. 감염률의 증가와 고령화 및 면역력 저하 계층의 취약성 증가는 신속 진단 솔루션에 대한 수요를 지속적으로 견인하고 있습니다. 탄탄한 의료 인프라와 첨단 진단 기술의 고도의 보급이 국내 전역의 지속적인 시장 성장을 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 테스트 유형별, 2022-2035

제6장 시장 추정 및 예측 : 기술별, 2022-2035

제7장 시장 추정 및 예측 : 방법 유형별, 2022-2035

제8장 시장 추정 및 예측 : 병원체 유형별, 2022-2035

제9장 시장 추정 및 예측 : 최종 용도별, 2022-2035

제10장 시장 추정 및 예측 : 지역별, 2022-2035

제11장 기업 개요

KSM 26.03.05The Global Sepsis Diagnostics Market was valued at USD 825 million in 2025 and is estimated to grow at a CAGR of 11% to reach USD 2.3 billion by 2035.

Growth is supported by the rising incidence of infectious diseases, increasing public-sector focus on infection control, and continuous progress in diagnostic technologies. Greater awareness among clinicians and patients regarding the importance of timely diagnosis is further strengthening market demand. Factors such as antimicrobial resistance, hospital-acquired infections, and the expanding prevalence of chronic health conditions continue to elevate sepsis risk, especially among elderly and immunocompromised individuals. Healthcare providers are increasingly prioritizing rapid and accurate diagnostic solutions to improve survival rates and manage treatment costs more effectively. The growing need for point-of-care and faster diagnostic tools is creating favorable conditions for innovation and global market expansion, as early detection remains critical for improving clinical outcomes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $825 Million |

| Forecast Value | $2.3 Billion |

| CAGR | 11% |

Government-driven investments in public health infrastructure continue to accelerate market growth. Sepsis is closely linked to infectious disease progression, making early identification a public health priority. National healthcare programs increasingly emphasize improved diagnostic readiness, enhanced laboratory capacity, and faster clinical decision-making. These initiatives support wider adoption of advanced diagnostic platforms and strengthen demand across hospital and laboratory settings.

The blood culture media segment generated USD 282.1 million in 2025. These products are formulated to promote the growth of microorganisms from blood samples, enabling the detection of bloodstream infections. Their compatibility with automated diagnostic systems and consistent usage across clinical laboratories ensures stable demand. Blood culture media remain a core component of sepsis diagnostics due to their essential role in confirming infections.

The microbiology-based diagnostics segment accounted for USD 316.8 million in 2025. This approach focuses on cultivating and identifying pathogens from patient samples and remains widely accepted in clinical practice. It supports detailed organism identification and antimicrobial sensitivity analysis, which are essential for guiding effective treatment decisions and improving patient management.

U.S. Sepsis Diagnostics Market was valued at USD 283.7 million in 2025. Rising infection rates and increased vulnerability among aging and immunocompromised populations continue to drive demand for rapid diagnostic solutions. Strong healthcare infrastructure and high adoption of advanced diagnostic technologies support sustained market growth across the country.

Key companies active in the Global Sepsis Diagnostics Market include Abbott Laboratories, Thermo Fisher Scientific, Inc., bioMerieux SA, F. Hoffmann-La Roche Ltd, Siemens Healthineers, Becton, Dickinson and Company, Beckman Coulter Inc (Danaher Corporation), Bio-Rad Laboratories, Bruker Corporation, and T2 Biosystems, Inc. Companies operating in the sepsis diagnostics market focus on multiple strategies to strengthen market position and expand global reach. Continuous investment in research and development enables faster, more sensitive, and more accurate diagnostic solutions. Strategic collaborations with hospitals and research institutions support clinical validation and adoption. Many players expand product portfolios to include rapid and point-of-care testing platforms. Geographic expansion into emerging healthcare markets enhances revenue opportunities. Automation, digital integration, and workflow optimization are prioritized to improve laboratory efficiency.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Test type trends

- 2.2.3 Product trends

- 2.2.4 Method trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in prevalence of infectious diseases

- 3.2.1.2 Increasing government initiatives towards infectious diseases

- 3.2.1.3 Technological advancements in infectious diseases diagnosis

- 3.2.1.4 Rising awareness regarding infectious diseases and its diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of sepsis diagnostics devices

- 3.2.2.2 Stringent regulatory framework

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with AI & digital health

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2024

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Test type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Blood culture media

- 5.3 Instruments

- 5.4 Assay kits & reagents

- 5.5 Software

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Microbiology

- 6.3 Molecular diagnostics

- 6.4 Immunoassays

- 6.5 Flow cytometry

Chapter 7 Market Estimates and Forecast, By Method type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Conventional diagnostics

- 7.3 Automated diagnostics

Chapter 8 Market Estimates and Forecast, By Pathogen type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Bacterial sepsis

- 8.3 Fungal sepsis

- 8.4 Other pathogen types

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Diagnostic centers

- 9.4 Clinics

- 9.5 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 F. Hoffmann-La Roche Ltd

- 11.2 Thermo Fisher Scientific

- 11.3 Abbott Laboratories

- 11.4 Beckman Coulter Inc

- 11.5 Siemens Healthineers

- 11.6 Becton, Dickinson and Company

- 11.7 bioMerieux SA

- 11.8 Bio-Rad Laboratories

- 11.9 Bruker Corporation

- 11.10 T2 Biosystems, Inc